The rapid development of the exchange-traded fund industry has brought to market some of the most useful and intriguing products for all walks of investors. With more than 1,600 ETPs offering exposure to just about every asset class, investment strategy, and developed or emerging economy, the potential portfolio combinations are endless.

Although investors can dip into some of the more complex and intriguing funds, most choose to select a number of ETFs that will allow them to build a well-diversified portfolio. But thanks to the innovativeness of ETF issuers, there is now an entire line of products that takes this strategy to the extreme, offering access to a complete portfolio through a single equity ticker.

A Closer Look

Enter target retirement date ETFs, the ultimate in passive, buy-and-hold investment strategy. To pick which of these funds is right for you, investors must simply select the ETF that corresponds to his or her intended retirement date (e.g. 2030 fund), the rest is left to the ETF’s manager. These hands-free portfolios are essentially designed to shift asset allocations with an investors’s changing risk profile.

For example, as an investor approaches his or her retirement, a higher allocation will go to fixed income products, while a younger investor would have a heavier weighting towards equity exposure.

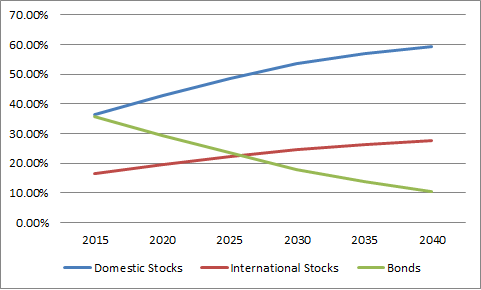

Here’s an example of how the exposure of these funds will shift depending on the target retirement date of the product:

As depicted above, the further out a retirement date is, the more a fund will invest in equities and less in bonds. Over time, these target retirement date ETFs will evolve, shifting allocations to asset classes with risk profiles that are more inline with investors’ objectives. So in the next 25 years, one would expect the 2040 fund to gradually shift away from equities towards bonds, eventually forming a portfolio that is very similar to how the 2015 fund looks today.

Here is a closer look at some of the most popular target retirement date funds (data as of 3/13/2015):

| ETF | Target Date | % in Stocks | % in Bonds | % in US Stocks | % in International Stocks |

|---|---|---|---|---|---|

| 2040 Target Date Fund (TDV ) | 2040 | 90% | 9% | 70% | 20% |

| 2030 Target Date Fund (TDN ) | 2030 | 70% | 29% | 54% | 16% |

| 2020 Target Date Fund (TDH ) | 2020 | 48% | 14% | 37% | 11% |

To achieve the different portfolio compositions, target retirement date ETFs actually invests in other exchange-traded products, essentially becoming a sort of “fund of funds.” iShares, for example, invests in its own ETFs, including the S&P 500 Index Fund (IVV ), Barclays Aggregate Bond Fund (AGG ), MSCI EAFE Index Fund (EFA ) and S&P Midcap 400 Index Fund (IJH ).

Be sure to also see our Retirement ETF Database Portfolios.

The Bottom Line: Benefits And Disadvantages

The adaptability of these funds is perhaps one of the most obvious reasons investors choose to invest in target retirement date ETFs. Once one of these ETFs are purchased, investors can sit back and let the security shift allocations to the most appropriate asset classes which best reflect the holder’s risk profile. Furthermore, investors won’t have to sift through the over 1,600 ETPs to build their long-term portfolios.

Instead, a single equity ticker provides fine-tuned exposure to a diversified basket of securities. But because these ETFs are funds that hold other ETFs, holders will have to burden a double layer of fees. While these expenses might be relatively low, they can add up over a long period of time. Potential investors should also take a close look under the hood of these ETFs since they only follow general rules to determine allocations, meaning that the resulting portfolio may not be exactly in line with your investment objective.

Follow me on Twitter @DPylypczak

For more ETF analysis, make sure to sign up for our free ETF newsletter.

Disclosure: No positions at time of writing.