Exchange-traded funds (ETFs) provide investors with a great way to invest like the professionals in everything from the obvious to the obscure. Using stock options, investors can build upon these strategies and better control their risk/reward profile. In this article, we’ll take a look at how protective puts can be used to hedge a long ETF portfolio against short-term declines or help lock-in profits after an extended move higher [see 101 ETF Lessons Every Financial Advisor Should Learn].

What Is a Protective Put?

Protective puts are simply long put options written against an existing long equity position. For example, suppose that you own 100 shares of the SPDR S&P 500 ETF Trust (SPY ) at 160.00 and are worried that the market may move lower. While you could sell the stock and buy back in later, you’re not sure that the rally is coming to an end quite yet, and buying and selling could result in excessive capital gains taxes or other negative side-effects [see ETF Call And Put Options Explained].

Purchasing an at-the-money put option with a strike price at 160.00 gives you the right to sell your 100 shares at a set price and time in the future in exchange for a small upfront premium paid now to enter into the contract. In this case, you can purchase the right to sell in one month at 160.00 for $2.87 per contract or $287.00 for every 100 shares. Normally, puts can be purchased for a relatively small amount relative to the position size being insured [see also 10 Questions About ETFs You’ve Been Too Afraid To Ask].

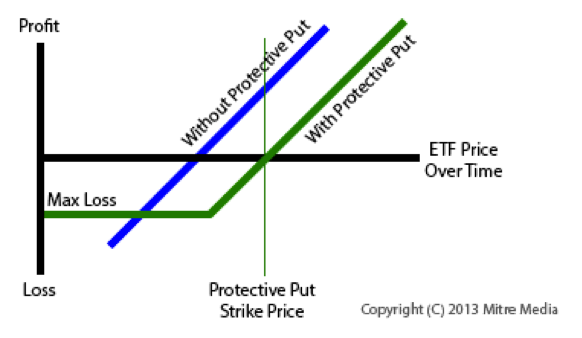

Here’s the payoff option diagram showing the dynamics of the position:

Who Is the Protective Put Strategy Right For?

Protective puts are ideal for investors concerned about a potential pullback in the market, but are not so concerned that they’re willing liquidate their position. In other words, these puts are designed for investors that are long-term bullish, but potentially short-term bearish, as opposed to those who foresee a longer-term correction in the equity or market. Those who are long-term bearish may want to instead sell the stock and consider alternative investments.

Here are some scenarios where protective puts are commonly used:

- Top-Heavy Markets – Situations where there’s a growing possibility of some profit taking, but the long-term fundamentals still look promising.

- Unrealized Gains – Situations where investors may be sitting on a large unrealized gain and they’d like to lock in some of those profits while keeping upside potential in tact.

- Upcoming Events – Situations where a single event may entail a lot of risk, such as an interest rate decision, but the long-term situation still seems promising.

What Are the Risks and Rewards?

Protective puts have a well-defined risk profile, given that they effectively set a price floor for a position, although they may involve a small amount of counterparty risk. The reward profile is also well established, as the position maintains its unlimited profit potential, since the option buyer is under no obligation to exercise the option, and would not do so at a loss [see also How To Swing Trade ETFs].

- Maximum Profit – Protective puts have unlimited profit potential, offset by the premium paid to enter into the option contract.

- Maximum Loss – The maximum potential loss with a protective put is limited to the put’s strike price plus the premium paid for the option.

Using the SPY example above, here are some possible risk/reward scenarios, assuming that the investor owns 100 shares of SPY and an at-the-money 160 put option:

| Option Price | SPY Price | Profit/Loss |

|---|---|---|

| $2.87 ($287) | 175.00 (Gain) | +$1,213 (+7.6%) vs. non-option +$1,500 (+9.4%) |

| $2.87 ($287) | 160.00 (Even) | -$287 (1.8%) vs. non-option $0 (0%) |

| $2.87 ($287) | 145.00 (loss) | -$287 (1.8%) vs. non-option -$ 1,500 (9.4%) |

How to Hedge Your Long ETF Positions

Protective puts are relatively simple options strategies to implement. Using the SPY example above, an investor purchases one at-the-money put option (160.00 in the example) for every 100 shares of SPY that he or she owns. The premium in that case is $2.87 per contract or $287 for every 100 shares that must be paid to enter into the agreement [see 13 ETFs Every Options Trader Must Know].

These protective puts give you the right to sell your stock at 160.00 per share, meaning that your ETF position has no downside risk over the next month; however, you still profit from any move higher minus the $287.00 premium paid for the protective put. The 100 shares owned makes this insurance come at a cost of 1.8% of the total position.

Of course, protective puts can also be purchased at prices above or below the current market price. Out-of-the-money puts tend to be cheaper and in-the-money puts tend to be more expensive than at-the-money puts. The pricing of puts may also depend on the volatility of the underlying stock, with greater volatility equating to a higher premium. The final decision depends on the risk tolerance and expected movement of the underlying stock.

The Bottom Line

Protective puts enable investors to hedge a long ETF position with a long put option, effectively setting a price floor for the position. The strategy is most commonly used by investors that are long-term bullish on the underlying ETF, but wish to limit their risk to either lock in profits or protect themselves from risks stemming from one-time events. To establish a position, investors can simply purchase one put option for every 100 shares of stock owned at the desired price and time, and in exchange, be protected against potential near-term downside risks.

[For more ETF analysis, make sure to sign up for our free ETF newsletter.]

Disclosure: No positions at time of writing.