When picking an ETF investment, many advisors don’t give a whole lot of thought to currency exposure, often times deeming it as far too risky or complex for their portfolio’s needs.

In fact, many investors may not have a strong opinion on the Brazilian real, Japanese yuan, or the Australian dollar. But those same investors often have exposure to those currencies-whether they realize it or not–through investments in assets denominated in those currencies.

Indirect Currency Exposure

Exposure to exchange rates is not reserved for those trading in ultra-leveraged forex accounts. The reality is that the vast majority of investors maintain significant exposure to international currencies in their portfolios through international stocks. Going long in Brazilian equities, for example, inherently includes a long position in the Brazilian real relative to the U.S. dollar. If the Brazilian currency appreciates, the returns realized by U.S. investors will be enhanced–and vice versa (more on this below).

Decisions on whether to accept risks associated with currency exposure can be big ones, as exchange rate movements can potentially have a huge impact on bottom line risk / return profiles.

Below we highlight three noteworthy examples that demonstrate the impact of currency exposure on ETFs:

1. ELD vs. EMB

When it comes to emerging markets exposure, many investors have embraced the exchange-traded product structure as a preferred means of rounding out exposure to both the equity and debt markets of developing nations. When comparing two popular offerings from the Emerging Markets Bonds ETF Database Category, the WisdomTree Emerging Markets Local Debt Fund (ELD ) and the iShares JPMorgan Emerging Bond (EMB ) appear almost identical after a quick glance.

Both products feature a similar split between foreign government debt and corporate bonds, and similar maturity breakdowns.

However, there is a a key difference between these products, and it has a rather significant impact on bottom line returns; ELD’s debt holdings are denominated in the local currency of the issuers, while EMB provides exposure to U.S. dollar denominated emerging markets debt.

If you look at the performance history of these two funds, there are also some striking differences, which can be largely attributed to fluctuations in the U.S. dollar relative to emerging market currencies represented in EMB and ELD.

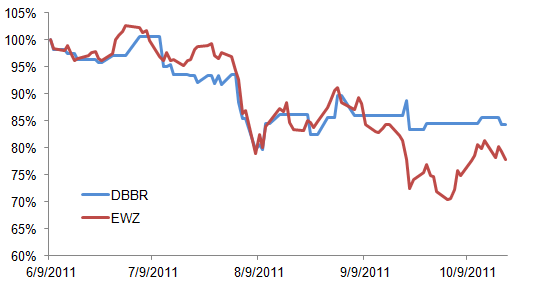

2. DBBR vs. EWZ

Fluctuations across foreign exchange rates can have a material impact on international products which have currency exposure. Consider for example the popular iShares MSCI Brazil Index Fund (EWZ ), which provides exposure to the performance of the Brazilian equity market, versus the recently launched MSCI Brazil Currency-Hedged Equity Fund (DBBR ):

In the 2011 returns chart above, notice the performance differences between the two; this variation in returns is quite significant when we consider the fact that DBBR provides exposure to the exact same basket of securities as EWZ. The distinguishing feature, however, is that DBBR is designed to provide exposure to Brazilian equity markets, while at the same time mitigating exposure to fluctuations between the value of the U.S. dollar and Brazilian real. The vast difference in performance between DBBR and EWZ across different time periods demonstrates the potentially adverse effects of currency fluctuations.

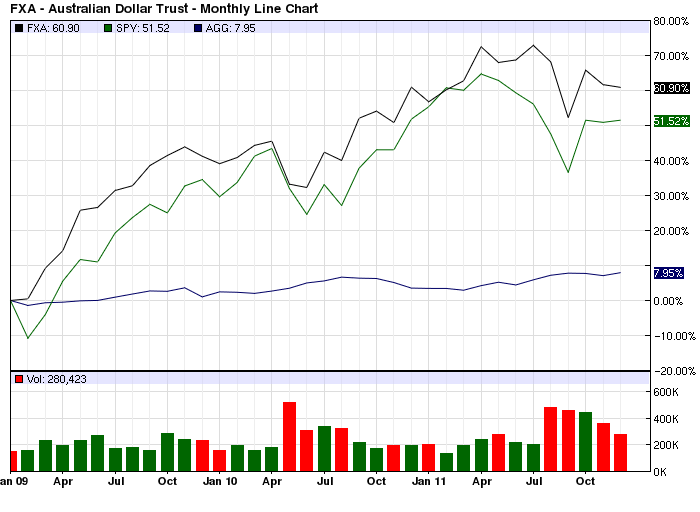

3. Pure Currency ETFs With Stellar Returns

Many investors shy away from currency investing, influenced by perceptions of extreme volatility and a zero-sum game. While ultra-leveraged forex trading does introduce potential for significant fluctuations–and likely losses after fees are considered–investors with a keen eye for spotting trends in macroeconomic developments can certainly stand to benefit from currency ETFs.

If you look for example at CurrencyShares Australian Dollar Trust (FXA ) from 2009 to 2012, the fund provided impressive and stable returns during this five year period, significantly outperforming bond markets and even the S&P 500.

The Bottom Line

It is important for investors to realize that both direct and indirect exposure to foreign currencies can impact bottom line returns. At the same time, investors should also recognize that currency investing can potentially enhance your portfolio over the long haul.

Disclosure: No positions at time of writing.