Since coming onto the investment scene in 1993, the market for ETFs has expanded dramtically, bringing the total number of exchange-traded products to approximately 1,700. This rapid growth has given investors more options than ever before, expanding the universe of investable assets to include nearly every geographic region, asset class, and investment strategy imaginable.

But this growth has also complicated matters for some investors. Sometimes picking the best ETF from an already shortened list can be a daunting task if you don’t know where to look. Below are five important statistics and descriptive metrics to consider before purchasing an ETF.

1. Expense Ratio

Why it’s Important: ETFs have gained so much ground on mutual funds in part because of their low-cost structure. While mutual funds on average charge approximately 1.40% in annual fees, some ETFs charge as little as 0.00% annually.

ETFs are generally cheaper, but there is a surprising amount of deviation between various funds. Within the Emerging Markets ETF Database Category, for example, expense ratios range from 0.14% to 0.98%, a gap wide enough to drive a truck through (data as of 06/04/2015). Once you’ve narrowed the universe of ETFs down to a few different options, be sure to compare the fee structures between funds. A difference of a few basis points doesn’t seem like much, but it can add up very quickly over the long term.

How to Find it: Each ETF Database Ticker Page includes the expense ratio for each fund. ETF Database Pro users can download results from the ETF screener into Excel, providing a tool for quickly evaluating the cost efficiency of various ETF options (if you’re not a Pro user, sign up for a free trial or read more here). It may also be useful to compare the expense ratio of an ETF to the average for its ETF Database Category (the low, high, and average expense ratios are included on each ETFdb Category page).

2. Index Methodology

Why it’s Important: When indexes were used primarily as benchmarks against which manager performance was measured, few investors gave much thought to the rules governing their construction and maintenance. But now that ETFs have transformed indexes into (effectively) investable assets, investors have begun taking a much closer look at index methodology.

Most of the indexes to which U.S.-listed equity ETFs are linked use a market capitalization-weighting strategy, meaning that the allocation given to a particular component stock is based on the market cap of the company. But ETFs utilizing “alternative” weighting methodologies have become increasingly popular in recent years. Some investors prefer equal-weighted funds that address some of the inherent flaws in cap-weighting, while others have found weighting systems based on revenue, earnings, dividends, and fundamental measures of size to be potentially superior (see this Guide To ETF Index Weightings).

How to Find it: A description of the underlying index is almost always available from the issuer home page. Generally, the description of the index on the issuer home page will include details on the weighting methodology used to develop the benchmark.

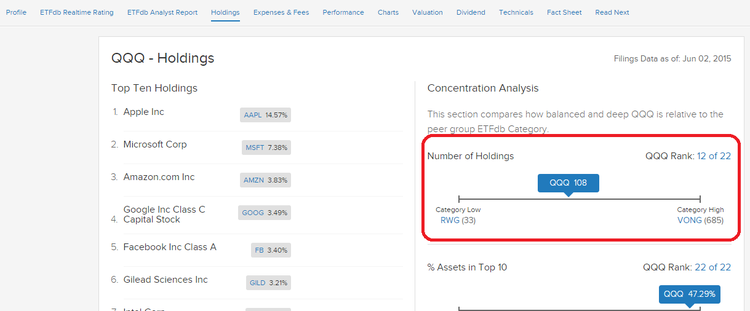

3. Depth of Holdings

Why it’s Important: Once upon a time, mutual funds burst on to the investment scene in part because they make it possible for relatively small investors to gain access to a large, well-diversified pool of assets. ETFs present a very similar value add in this area, allowing investors to gain exposure to a basket of securities with the purchase of a single share.

But the depth of exposure offered by otherwise similar ETFs can be very different. For example, the FTSE/Xinhua China 25 Index Fund (FXI ) has 54 individual holdings, while the SPDR S&P China ETF (GXC ) has about 356. More isn’t necessarily better–it’s sometimes advantageous to concentrate holdings in a small group of securities–but the depth of exposure offered can have a significant impact on an ETF’s risk/return profile.

How to Find it: Almost every ETF issuer prominently displays the number of securities underlying an ETF on the ticker home page. If you can’t find it there, this figure can be computed from the daily holdings data required of each ETF. (Or simply look under the “holdings” tab on ETFdb).

4. Tracking Error

Why it’s Important: Nearly every ETF description includes something along the lines of “ABC seeks to replicate the performance of the XYZ Index,” indicating the benchmark to which fund returns can be expected to correspond. Many investors assume that all ETFs match the underlying index exactly, but this isn’t always the case. Unlike a hypothetical index, for which the rebalancing process is the flip of a switch, ETFs must actually go out into the market to buy and sell securities at certain points. Moreover, the depth of certain indexes (some have more than 8,000 individual components) makes exact replication difficult, and forces certain funds to use a sampling process.

Tracking error is a good measure of the efficiency of the ETF manager. The smaller the difference between an ETF and its underlying index, the better.

How to Find it: Somewhere on the fund homepage, the ETF issuer will provide performance data for both the ETF and the related benchmark, generally for the most recent quarter and year, as well as three-, five-, and ten-year periods (if the data is available). It’s also worth noting that iShares offers a pretty slick tool that allows investors to view tracking error over customized time periods (see the tool in action here).

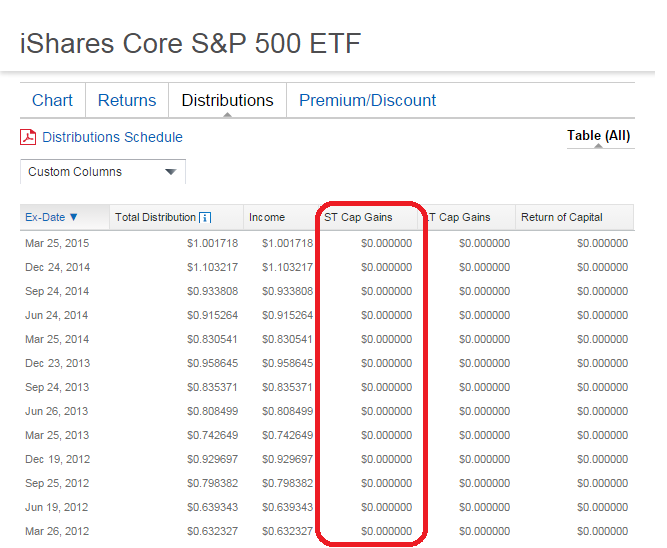

5. Tax Efficiency

Why it’s Important: Another big draw of ETFs is the potential for advantageous tax treatment relative to actively managed mutual funds. Because of the nuances of the creation/redemption process, as well as the inherently lower turnover, ETFs can be “more tax efficient” than mutual funds (and in fact, most are). A good way to measure this tax efficiency is by examining the distribution history for the fund.

Ideally, ETFs will make zero short-term capital gains distributions since the presence of these outflows indicates that short-term gains (which are taxed at higher rates) were incurred by the fund managers. Ordinary income distributions are just fine (these are generally unavoidable and taxed at a more investor-friendly rate), but a regular history of capital gains distributions can be a red flag.

How to Find it: The distribution history of most ETFs can be found on the issuer web site. In most cases, distributions will be classified as either ordinary income, short-term capital gains, long-term capital gains, or return of capital. The image below shows the recent distribution history for IVV, and indicates that this ETF is pretty efficient from a tax perspective.

For more ETF analysis make sure to sign up for our free ETF newsletter.

Disclosure: No positions at time of writing.