These days, many investors are looking for more than just a positive return. They’re looking for a social return as well. An investor’s moral compass has become the guiding light just as valuation metrics, dividend yields and other traditional stock-picking fair have dominated in the past. Bridging the gap between profits and purpose has become a multi-trillion industry as investors have embraced the concept.

And it only continues to grow further. The number of socially responsible investing (SRI) indexes, ETFs and other investment vehicles has exploded as awareness and returns of SRI investments have grown.

But should you be concerned with trying to find great portfolio returns and acting as an agent for positive change? Well, if recent history is any guide, the answer is a resounding yes. With that in mind, here’s the 411 on socially responsible investing.

By signing up for ETFdb.com Pro, you will get access to real-time ratings on over 1,900 U.S.-listed ETFs.

So What Exactly Is SRI Investing?

SRI practices have their beginnings in the Quaker community. The group looked for ways to invest while adhering to their religious beliefs, which was difficult to do back in the 1960s and ’70s. To appease the group, money managers followed a simple weeding-out of various “sin” stocks from broader portfolios. This included removing firearms makers, alcohol producers and gambling-related stocks. The exclusion of sin stocks was the first modern forays into SRI investing and it set the stage for the movement of investing on principal.

Today, socially responsible investing is a bit more complicated, but the underlying principles remain the same. And that’s to balance the traditional four levels of corporate responsibility while seeking those firms with superior business models and forward-thinking attributes that are focused on the long term. This means making a profit, but doing so without violating any laws, ethics or ideals as well as making an effort to benefit society. Essentially, finding good companies that are doing good.

The how is a tad bit tricky. Today’s socially responsible investors use various environmental, social and governance (ESG) metrics when evaluating a stock or fixed-income investment.

Why is SRI gaining in popularity? Find out here.

When looking at environmental factors, a screen will examine various parameters such as a corporation’s carbon and greenhouse output, how much waste it produces, and what raw materials it uses and how those materials are sourced. The focus isn’t just on output, but also on the reduction of carbon through green energy initiatives and recyclable products/waste programs.

Social screens will take a look at a firm’s labor practices. This includes the health and safety of their workers, how they treat different genders, LGBT and minorities in the workforce as well as the labor practices of the suppliers they use. Additionally, some social screens can measure the impact of a company’s products or services on society as a whole.

Governance standards come down to how a firm conducts itself. Whether a company engages in corrupt accounting practices, excessive litigation, scandals, bribery or even high levels of executive compensation versus how much it pays its workers.

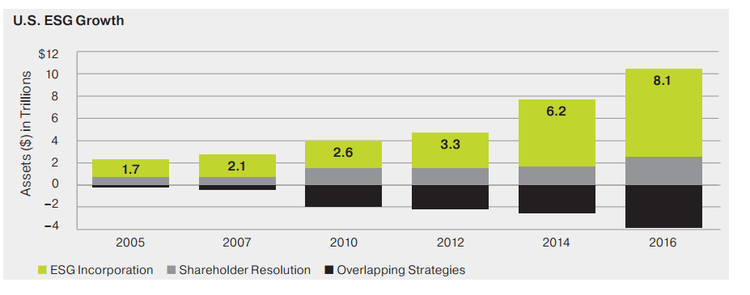

And investors certainly are taking the bait. Assets in SRI-focused investment vehicles continue to skyrocket. As illustrated by the following chart from mutual fund and investment manager Oppenheimer and SRI investing trade group, the U.S. SIF Foundation, more than $8.1 trillion now sits in SRI portfolios as of last year. To put that in context, the number of total assets under professional management in the United States was $40.3 trillion. Roughly a fourth of all of the money managed in the U.S. was in some sort of socially responsible investment vehicle.

The vast bulk of this wealth resides in 475 different mutual funds. However, ETFs and other investment vehicles continue to see swift adoption from investors. Last year, the total ESG assets of investment funds clocked in at roughly $2.6 trillion. That was more than double the amount recorded in 2014 and ten times the $202 billion record in 2007.

Utilize our ETFdb.com Screener tool to filter through the entire ETF Database universe including Socially Responsible ETFs by dozens of criteria such as asset class, sector, region, expense ratio and historical performance.

Building Out The Portfolio

The complexity of screening for ESG attributes underscores the evolution of SRI investing. If you remember the Quakers, they simply removed those types of stocks they did not like. This approach then evolved into targeting exposure to a theme and using positive screening or rules-based tilts to find the best ESG firms.

The latest evolution in ESG investing comes down to harnessing ESG information to improve the investment outcome. For example, indexing giant MSCI will use public data and filing information for one thousand different data points related to ESG. Those points are further broken down- 80 exposure metrics, 129 management issues, and 37 industry-specific parameters- to score individual stocks and make a smart-beta index.

Investment managers today, use all three methods for building out SRI portfolios.

Negative or Exclusionary Screens

Think the Quaker model. Negative or exclusionary screens will remove stocks from certain industries- like tobacco or firearms. You’re basically saying “I don’t want this in my portfolio.” More modern negative screening techniques will eliminate these sectors plus all the firms scoring below a certain threshold. The idea is that investors can remove stocks and industries that don’t jive with their overall beliefs. Someone who doesn’t believe in abortion can “not support” those pharmaceutical firms that supply products for or it, or those against war can eliminate weapons manufacturers. The problem here is that “sin” stocks have actually been some of the best-performing industries over the long haul. Investors could be leaving returns on the table.

Top ETF examples of a negatively screened fund include the $822 million iShares MSCI KLD 400 Social ETF (DSI ) – which kicks out all tobacco, gambling, firearms/weapons, nuclear power, adult entertainment and GMO seed producers in the USA Investable Market Index. Both the iShares MSCI ACWI Low Carbon Target (CRBN ) and SPDR S&P 500 Fossil Fuel Reserves Free ETF (SPYX ) are prime ETF examples of exclusionary. Both CRBN and SPYX will eliminate those firms with fossil fuel or high carbon scores from their underlying holdings.

Positive or Best-In-Class Style Screen

A positive SRI screen is saying “I do want this in my portfolio.” Here analysts will search for those firms that show positive attributes on the ESG model and included them. In broad-based funds, this includes creating a scoring threshold and any firm getting higher than this will make the cut. The FlexShares STOXX US ESG Impact Index Fund (ESG ) is great example of a positive/best-in-class screened fund. ESG will score stocks on various performance indicators and tilt the portfolio accordingly.

An offshoot of positive of best in class is so-called impact or thematic investing. Those funds that look at a certain ESG theme such as green energy or water investing are considered thematic. Those that seek to make a social change such as gender diversity and women’s rights fall under this positive subcategory. The Guggenheim Solar ETF (TAN ) and PowerShares Water Resources ETF (PHO ) are two of the most popular thematic ETFs. The $300 SPDR SSGA Gender Diversity Index ETF (SHE ) is a great example for an impact ETF as it bets on stocks considered gender-diverse and have greater gender diversity in their senior leadership positions.

The downside to positive screening is picking the wrong factor to focus on. Since you are focusing directly on a single factor, choosing the wrong factor or combination of factors could be the wrong choice and lead to losses.

Restricted Screening Process/ESG Integration

Finally, most modern ESG indexers use what’s called a modified selection process. Here, ESG criteria are just one piece of the puzzle. Parameters are weighted accordingly to sector and industry. That means that energy stocks aren’t necessarily punished for environment scores more harshly than a bank stock. ESG criteria are kept in proportion. So not all energy stocks are removed, but those that really pollute are. In a negative or positive screen, the sector may be kicked out altogether. The Oppenheimer Environmental, Social, and Governance (ESG) Revenue Weighted Strategy ETF (ESGL ) is an example of this and uses ESG and traditional metrics to weight its portfolio. That portfolio does include some non-traditional SRI holdings.

For a full list of Socially Responsible ETFs, click here.

The Bottom Line

Socially responsible investing continues to grow and expand as investors have taken a shine to building profits with a purpose. There’s no longer a trade-off between profits and the planet. That’s good news for investors. And while it may seem complex, the real crux of SRI comes down to how the various ESG factors play into your fund or chosen investment vehicle.

For more ETF news and analysis, subscribe to our free newsletter.