The era of ultra-cheap exchange-traded funds (ETFs) is upon us, and asset managers are upping the ante to remain competitive in a market with no shortage of selection. Several of these firms are venturing into new offerings with variable fees in an attempt to lure investors.

Over the past few years, several major fund managers have introduced new funds whose fees rise with returns and fall when the ETFs underperform the market. In the investment community, this sliding fee structure is called a fulcrum fee.

Fulcrum Fees: An Introduction

Put simply, a fulcrum fee is a performance-based fee that goes up or down based on how well a particular fund performs against its benchmark. Funds that employ fulcrum fees charge more when they outperform their benchmark (on a sliding scale) and slash their fees when they underperform the market. Although low-fund fees have been around for a long time, these new products begin with a lower base fee that rises and falls more sharply depending on performance. Fulcrum fees tell investors that the fund manager is confident it can outperform the market, and will provide a type of insurance if they don’t.

Use our ETF Screener to find the right ETFs for your portfolio.

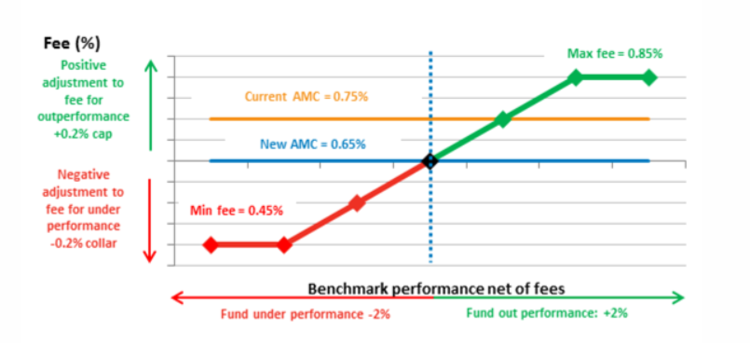

The following diagram, courtesy of Fidelity International Limited, demonstrates how the fulcrum fee works. In this particular diagram, a fund charges a ‘maximum fee’ when it outperforms the benchmark (net of fees) by 2%.

Fidelity sets the ceiling at 0.2% above the base management fee and the floor at 0.2% below it. This makes the Fidelity fulcrum fee completely symmetric, thus avoiding one of the main criticisms of variable fee funds (namely, ‘heads we win, tails you lose’). In this particular example, the ceiling kicks in when the fund performs 2% or better. The floor is triggered when the fund underperforms the market by 2% or more.

As of 2016, less than 2% of U.S. registered funds employed fulcrum fees. However, analysts expect their use to rise steadily as asset managers respond to mounting pressure over lowering their fees.

To learn more about ETF Investing Strategies, click here.

Regulatory Considerations

U.S. regulation puts stern limits on the types of performance-based fees that fund managers and financial advisers are able to charge. The Investment Advisers Act of 1940 was the first legislation to put an outright ban on performance-based fees because they give advisers too much incentive to take big risks.

Lawmakers first permitted performance-based fees (i.e., fulcrum fee) in 1970, but only by Registered Investment Advisers (RIAs) managing mutual funds. It would take another 15 years before the Securities and Exchange Commission (SEC) permitted the use of fulcrum fees with retail clients on the basis that the adviser was equally vested in the performance of the fund as the investor.

To this day, the SEC requires two conditions to be met for an adviser to charge a fulcrum fee:

- Returns must exceed the benchmark; if they don’t, the fee must be reduced.

- Only ‘qualified clients’ defined under Rule 205-3 of the Investment Advisers Act of 1940 can be charged a fulcrum fee. This includes individuals or registered investment companies with an account value greater than $1 million or a net worth higher than $2.1 million.

Compare the fees and expenses of ETFs vs. mutual funds here.

Opportunities and Costs

Depending on your investment goals, fulcrum fees provide both opportunities and risks. On the one hand, funds that employ such a model are able to attract investors with more aggressive portfolios as well as those looking for market-beating strategies without the added risks. Fulcrum fees essentially tell the investor that the fund manager is confident they can outperform their benchmark and will provide insurance if they can’t.

Fulcrum fees also cater to cost-conscious investors who don’t want to pay higher fees for funds that don’t always beat the market. This gives them the incentive to work with a particular fund without paying a premium during downturns or rough patches.

On the opposite side of the spectrum, fulcrum fees can be costly. For starters, only a tiny minority of funds employ such a strategy and there isn’t enough data to conclude whether they consistently outperform their benchmarks or not. At the same time, with so many ETFs to choose from, it’s not entirely clear that this narrow slice of the fund universe offers any tactical advantage even when outperforming the market. For many investors, low-fee ETFs may provide a better alternative.

Be sure to check our News section to keep track of the latest news on ETFs.

Investor Due Diligence

While all fulcrum funds operate on a sliding fee structure, they can vary significantly in terms of structure. Investors must, therefore, perform their due diligence when selecting which fulcrum funds to include in their portfolio.

For starters, it’s important to compare the fee structure of a particular fund relative to others. Not all funds in this category operate like the Fidelity fulcrum fund described above, so it’s important to get up to speed on how cost ceilings and floors are calculated. Investors should only select funds with a transparent fee structure that is easy to understand. This is true of all ETFs, but especially those that charge a variable fee.

Secondly, not all funds track the same index. Investors who are paying for performance should consider funds with an index that’s not very easy to beat. After all, it doesn’t make sense to select a fund that charges a higher premium for outperforming a benchmark that most passive fund managers are already beating. As an example, outperforming the S&P 500 during the so-called Trump reflation trade after the 2016 election was relatively easy given the extent of the bull market.

The Bottom Line

The concept of fulcrum fees isn’t going away any time soon. As asset managers respond to growing industry pressures, investors can expect performance-based fees to proliferate in the near term.

For more ETF news and analysis, subscribe to our free newsletter or sign up for ETFdb Pro to get access to our ETF Guides.