With Treasury yields on the rise, the list of choices for investors seeking to increase their portfolio income is growing. In addition to traditional sources of income such as interest and dividends, investors can use call options in order to generate synthetic income to enhance overall portfolio returns.

A call option gives the holder the ability to purchase a security at a specified price for a predetermined period of time. The most commonly used plan for producing income using call options is the covered call strategy. This involves owning a long position in an ETF while simultaneously selling a call option and collecting the premium. It’s a strategy that takes some time and effort to execute, but one that can help boost monthly portfolio income while potentially reducing risk.

To find out more, check out our introduction article on earning income with ETF options.

ETFs That Offer Options

Many ETFs offer the ability to trade options on them, but it’s the largest ones that often get utilized. The SPDR S&P 500 Trust ETF (SPY ) is the most frequently used product for options trading, and accounts for nearly half of all options trading volume on an average day.

Other ETFs often active in the options market include the iShares MSCI Emerging Markets ETF (EEM ), the iShares Russell 2000 ETF (IWM ), the SPDR Gold ETF (GLD ) and the PowerShares QQQ ETF (QQQ ). ETFs such as these are regularly used for options trading due to their liquidity and tradability.

The Covered Call Strategy

The covered call strategy involves owning shares of a particular ETF while, simultaneously, writing a call option on those same shares. Each options contract is for 100 shares. Therefore, one contract would need to be written to cover each 100 shares owned. Calls could be written either at the money (ATM) or out of the money (OTM) depending on risk and income preferences. At-the-money calls would be expected to earn more income but run a greater risk of being exercised if the price of the underlying moves up. Conversely, out-of-the-money calls would yield less but also have less risk of being exercised.

In-the-money (ITM) covered calls can also be used, but their upside potential is limited to the call premium received from writing the call.

Naked vs. Covered Calls

When using written calls to generate income, investors in most cases tend to use the covered call strategy. In these cases, if the written option gets exercised by the buyer, the investor has the appropriate number of shares on hand to fulfill the contract.

A riskier method of generating income would be a naked call strategy. This involves an investor writing calls to generate income but owning no shares of the underlying security. It’s riskier because if the written option gets exercised, the seller would need to go out into the open market to purchase shares to deliver. This would ultimately lead to additional losses for the seller since they would need to purchase shares at the market price and deliver them to the call buyer at a lower price. The potential losses are, theoretically, unlimited.

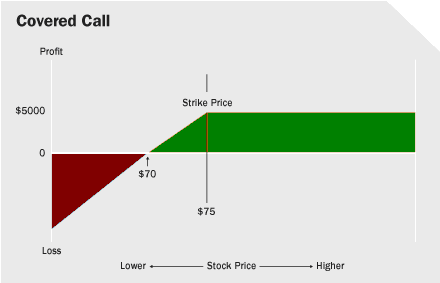

Profits and Losses Using Covered Calls

Covered calls can enhance overall portfolio income, but can also limit upside potential of the long position.

For example, an investor owns a stock with a price of $75 per share while, at the same time, writing a call with a $75 strike price for $5.

In this case, the investor’s breakeven point would be $70. They would lose $5 on the long position but would gain $5 in options premiums. Above a $75 price, the profit caps at $5 per share, since any gains in the underlying would be offset by corresponding losses in the written options. In theory, the maximum loss in this scenario would be $70 per share. The underlying could go all the way to zero resulting in a $75 per share loss on the loss position but would earn $5 in options premiums.

For additional income, check out a list of the top dividend ETFs using our ETF Screener.

In the Money and Out of the Money

Calls are considered in the money (ITM), at the money (ATM) or out of the money (OTM) depending on where the current price is relative to the option’s strike price.

Calls where the strike price is below the current price are in the money. Buyers of in-the-money call options would need to exercise them prior to their expiration date in order to profit. If not, they expire worthless, as the contract period will have ended.

At-the-money (ATM) calls have an equal current and strike price. These options would likely go unexercised since there is no profit to be gained and would result in transaction fees.

Calls where the strike price is above the current price are out of the money (OTM). Out-of-the-money call options can either be left to expire worthless or the holder could attempt to sell them prior to expiration in order to return some value.

The Benefits of Technical Analysis in Call Writing

Some traders will use technical analysis to attempt to forecast price moves in a stock. They do this by examining historical chart movements and trading volumes in order to predict patterns.

There are several indicators that can be used. Bollinger Bands is one popular indicator. Another is the relative strength index (RSI). The RSI compares gains and losses over a given time period to measure a security price’s relative strength in movement. Using a 0-100 scale, the RSI attempts to gauge whether a security should be considered overbought (a value of 70 and above) or oversold (a value of 30 and under).

Securities would, in theory, be sold in an overbought environment and vice versa. If the RSI indicates the security is in overbought territory, traders would be more apt to write call options anticipating that the price of the underlying may be heading downward.

The Risk of Call Writing

Call writing involves multiple risks. Writing call options effectively can be complicated and can expose traders to a significant risk of loss if they’re not familiar with how to implement a covered call position or implement it incorrectly.

While call writing can be a great way of collecting options premiums, it also limits the upside potential of the overall portfolio. Investors who have covered call positions can miss out on gains if the market moves sharply upward in a short period of time. Naked call positions can be especially risky, since there is, in theory, no limit to the potential losses in such a strategy.

For more strategies, come back to our ETF trading strategies category page on a regular basis.

Covered Call ETFs

If setting up a covered call strategy sounds too complicated or too labor-intensive, there are also a handful of ETFs that utilize the covered call strategies as part of their investment objective. The Recon Capital NASDAQ 100 Covered Call ETF (QYLD ), for example, takes positions in each of the index’s 100 components while simultaneously writing one-month at-the-money call options. It’s a relatively straightforward way of having a professional handle the work of call writing for you.

The Bottom Line

Call writing strategies can generate synthetic yields much above what the average Treasury security pays. It does, however, require the knowledge to properly execute the position as well as continuous portfolio monitoring in order for the strategy to pay off.

Further Reading

To learn more about specific options trading strategies, check out the rest of our ETF Options Income Series: