This section is designed for people that are brand new to the MLP space or those that simply want a refresher. Master Limited Partnerships, or MLPs, are companies engaged in the transportation, storage, processing, and production of natural resources. When most investors think about MLPs, they focus on midstream —those companies involved in transportation, storage, and processing. These fee-based business models benefit from the abundance of natural resources in the US and generate consistent cash flows. An investment in energy infrastructure MLPs is an investment in North America’s continued production and consumption of transportable energy over the next several decades.

The Very Basics

MLP stands for Master Limited Partnership. Most people think of MLPs as energy pipeline companies with an advantageous tax structure, which is an extreme simplification, but not untrue. All partnerships in the US, including MLPs, pay no income tax at the partnership (or company) level. Unlike most partnerships, MLPs are public companies, trading on the major stock exchanges and filing reports with the Securities and Exchange Commission (SEC). Midstream MLPs are involved in the transportation, processing, and storage of oil, natural gas, and natural gas liquids (NGLs).

The Basic Midstream MLP Business Models

- Transportation Just like it sounds, transportation MLPs move energy commodities like oil and natural gas from one place to another. In North America, most energy travels through a pipeline, but it can also move via truck, railcar, or ship. Pipelines are the cornerstone of energy infrastructure MLPs.

- Processing Processing encompasses any business that transforms a raw commodity into a usable form. It involves removing impurities like water and dirt from wellhead natural gas and separating the natural gas stream into pipeline-quality natural gas and NGLs, which are used as heating fuels and petrochemical feedstocks.

- Storage Storage includes tanks, wells, and other facilities both above and below ground. These assets provide flexibility to the energy economy, so there is propane available for winter heating, gasoline for summer driving, and jet fuel for the holidays.

How is an MLP Different Than a Traditional Corporation?

Most notably, by limiting themselves to handling natural resources and minerals, MLPs do not pay federal income tax at the entity level. This means that they can pay out more of their cash flow to investors. Corporations, on the other hand, do pay federal income tax.

MLPs are also governed differently than regular corporations. Companies such as Exxon, Apple, and Ford are primarily owned by shareholders. Decisions are made by management teams as well as by shareholders at an annual meeting where major issues are decided by voting. A shareholder has one vote per share owned, and either a majority or a plurality of votes may be required for particular decisions. Most MLPs, on the other hand, are governed by their general partner.

MLPs generally have two classes of owners: the general partner (GP) and the limited partner (LP). The general partner interest of an MLP is typically owned by a major energy company, an investment fund, or the direct management of the MLP. The GP controls the operations and management of the MLP and typically owns some portion of the LP. Limited partners (aka people who own units) own the remainder of the partnership but have a limited role in its operations and management. Legally, the general partner has no fiduciary duty to make decisions that will benefit LP unitholders, although what benefits the GP typically benefits the LP.

How Midstream MLPs Make Money

MLPs typically operate fee-based business models. They earn a set fee for each barrel of oil or million British Thermal Unit (MMBtu) of natural gas transported, stored, or processed (in the case of natural gas) regardless of the price of the hydrocarbon. This is because these companies typically do not own the oil or gas.

MLPs generally sign long-term contracts (five to 20 years in length) with their customers, which makes for stable cash flows. Accordingly, the revenue equation for most business activities is fairly simple: price multiplied by volume. As such, more volumes mean more cash flows. On the price side, a federal agency sets the fee charged by interstate liquids pipelines, and the fee increases with inflation. Pipeline fees can also be negotiated with a customer based on the cost of operating the pipeline and market rates for liquids or natural gas pipelines. On the volume side, growing production of U.S. oil and natural gas over the last several years has necessitated more energy infrastructure such as pipelines, storage tanks, and processing plants.

How Investors Make Money With MLPs

If you own a stock, there are two ways to make money. The price of the stock increases and you can sell it for more than you bought it. Formally, this is known as price appreciation. The stock also likely pays you dividends. MLP dividends are called distributions because of the partnership structure. The amount of distributions relative to the unit (or share) price is known as yield.

It is worth noting that MLP distributions are not guaranteed and vary depending on the MLP. Unlike real estate investment trusts (REITs), which must distribute a certain percentage of their cash flow each quarter, the partnership agreements of individual MLPs determine the level of distributions.

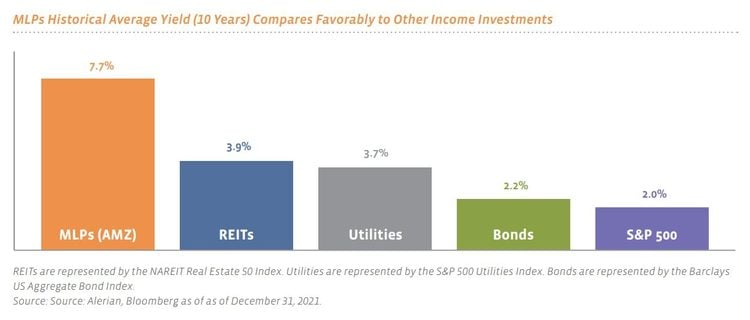

The historical average yield of MLPs over the past 10 years has been around 8%, which means that if you invested $100, on average, you would be paid $8 each year. The chart below shows yields for MLPs, represented by the Alerian MLP Index (AMZ), compared to other asset classes. MLPs boast a higher yield than utilities and REITs, which are asset classes known for their income potential.

History of MLPs

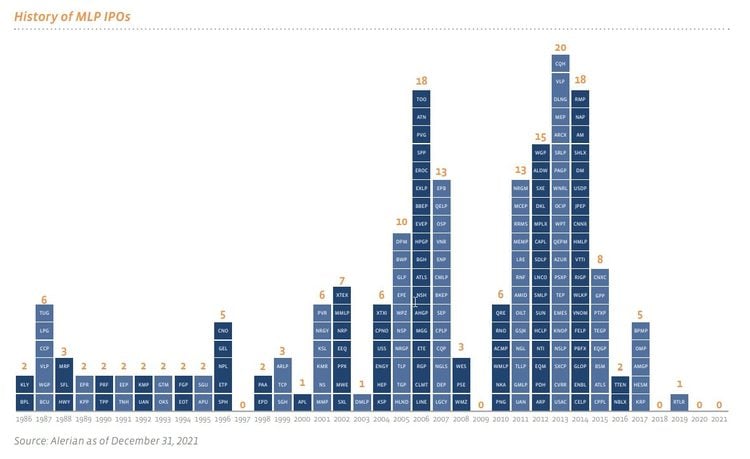

The History of MLPs In 1981, Apache Corporation created the first MLP, Apache Petroleum Company (APC). By combining the interests of 33 disparate oil and gas programs into one, APC was able to operate them more efficiently. As APC was traded on both the New York Stock Exchange and the Midwest Exchange, investors were easily able to buy and sell these interests just like shares of stock rather than having to wait for the sale of the whole business to realize their profits. Other oil and gas MLPs soon followed, as did real estate MLPs. And throughout the 1980s, more and more businesses became involved until there were cable TV MLPs, hotel MLPs, amusement park MLPs, and even the Boston Celtics became an MLP. Soon, the government noticed (after all, it was losing out on taxes!), and Congress worried that every corporation, especially Exxon, would become an MLP. Congress passed the Tax Reform Act of 1986, and President Ronald Reagan signed it on the South Lawn of the White House. In addition to eliminating several other tax shelters, the act defined the structure of the modern MLP. Section 7704 of the Revenue Act of 1987 limited which businesses could be MLPs, delineating that an MLP must earn at least 90% of its gross income from qualifying sources, which were strictly defined as: transportation, processing, storage, and production of natural resources and minerals. Any MLPs that had other kinds of income could remain MLPs, but in the past 30 years, most have gone private or converted to other structures. By the turn of the new millennium, MLPs began to own ships for the seaborne transportation of energy resources as well as the storage tanks and bobtail trucks necessary for propane distribution. Several coal companies also became MLPs, and in 2006, after a long hiatus, the upstream MLP returned (only to decline during the 2014-2015 oil price downturn). In 2012 and 2013, more non traditional MLPs came to market. While there are many types of energy MLPs, Alerian focuses on midstream or energy infrastructure MLPs. For a complete list of energy infrastructure companies, both MLPs and corporations, please see Alerian’s Screener.

The Pipeline Business, Explained

The modern pipeline network in the U.S. has its roots in the outbreak of World War II. Before the war, the East Coast was the largest consumer of energy in the country. Refined products (such as gasoline, diesel, and jet fuel) were delivered from Gulf Coast refineries via tankers. Tankers also carried raw crude oil from the Middle East. However, once the U.S. became involved in the war, German submarines began sinking these tankers. Together, the government and the petroleum industry built pipelines that could cover long distances and transport large amounts of oil. This network subsequently fueled the economic boom that followed the war, and many of those original pipelines are still in service today.

There are both large diameter trunklines that function like interstates (instead of being four lanes wide, they are often 42” in diameter, or large enough for a child to stand inside), as well as smaller delivery lines that connect the large pipelines to each town. Product traveling through trunklines is fungible —the customer will receive product on the other end that is the same quality as that which was sent, but they won’t be the exact same molecules. It is as if someone sent $100 to a college student through a bank. That student will not get the exact same $100 bill as his or her benefactor sent, but the student doesn’t care because $100 is $100. Money is fungible. However, smaller delivery lines operate on a batch system, where the exact same molecules are delivered as were shipped. In this case, our lucky college student gets a couple dozen cookies, and the ones delivered are the exact same cookies his or her parents baked, not cookies that some other people made.

Energy Renaissance

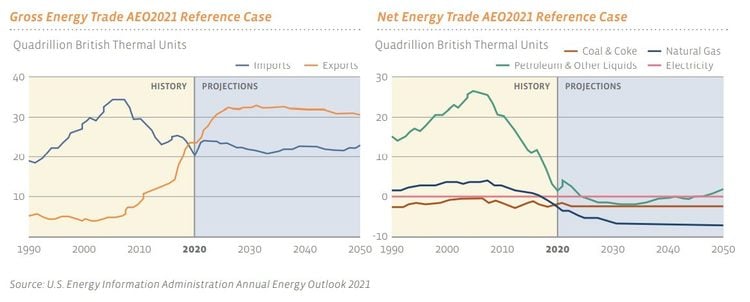

The term “energy renaissance” refers to the transformative growth in U.S. energy production that has occurred over the last several years, culminating in the U.S. becoming a net energy exporter in 2019.

Prior to the 2000s, much of the energy industry was focused on peak oil and the ways companies and our society would have to shift in response. While producers knew that oil reserves existed, accessing the oil in a cost-effective way was difficult. Experts forecasted that expensive and complex recovery methods would be needed to continue to produce even a modest number of barrels.

In the early 2000s, the natural gas industry in the U.S. began widespread application of horizontal drilling and hydraulic fracturing. The technologies were not new, but the combination of both technologies made it possible to profitably produce the large reserves of crude oil, natural gas, and NGLs trapped between layers of North American shale rock. Horizontal drilling was developed in the first half of the 20th century, and the first commercial applications of hydraulic fracturing took place in 1949. After seeing the success of natural gas companies in applying these technologies, oil producers began implementing the same drilling technology, seeing strong production growth from oil wells.

In 2009, the U.S. became the world’s largest producer of natural gas. By 2012, the U.S. had an abundance of natural gas, leading to lower prices, but gas production continued to grow. In 2014, rapid growth in U.S. oil production had led to a global crude oversupply and weakness in oil prices. A multi-decade ban on U.S. crude exports was lifted by Congress in December 2015. In 2018, the U.S. became the world’s largest oil producer. For the first time since the early 1950s, the U.S. in 2019 was a net energy exporter and remained so in 2020.

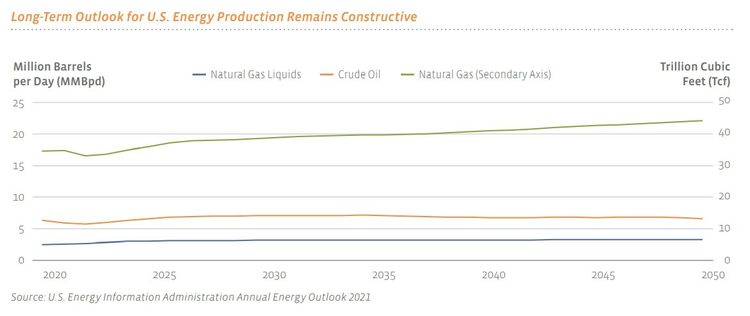

The U.S. exports liquefied natural gas (LNG) and millions of barrels per day of crude and refined products like gasoline and diesel. As shown in the chart below, U.S. energy production is expected to rebound and remain fairly steady over the long-term, with natural gas production expected to grow noticeably.

The outlook for production growth contributes to expectations that the U.S. will remain a net energy exporter in the coming decades.

What the North American Energy Landscape Means for MLPs

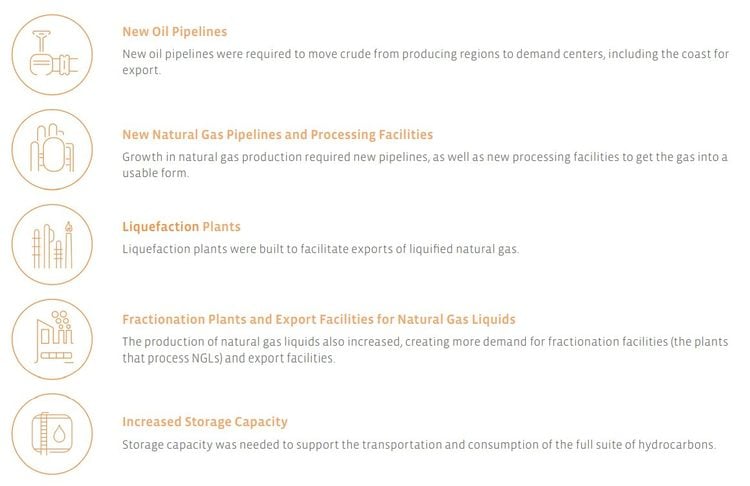

The tremendous growth in U.S. oil and natural gas production necessitated a significant investment in the buildout of new energy infrastructure. While not as dramatic, energy production from Canada has also increased, necessitating new infrastructure. The production growth seen over the last decade or so in the U.S. and Canada would not have been possible without these infrastructure assets.

Clearly, this massive infrastructure buildout had a hefty price tag, with midstream companies spending significant capital for years. However, annual capital investment peaked in 2018 or 2019 as production growth rates were expected to moderate. The weakness in oil prices in 2020 led to a decline in U.S. energy production, and companies recalibrated spending plans in response, with some planned projects tabled. While U.S. energy production is expected to recover into 2022, MLP capital spending plans are generally more modest than in the past. As such, MLPs are expected to enjoy the fee-based cash flows of previously completed projects, while reduced growth spending should allow for significant free cash flow generation.

Risks

If you have listened to a company’s earnings call, viewed an investor presentation, or perused a company’s annual report, you will have noticed disclaimers and/or a discussion of risk factors. While some of these risks may be unlikely to occur, they could impact your expected total return. While several key risks are discussed below, this list is not intended to be exhaustive.

Commodity Price Sensitivity – Since MLPs do not own the oil and gas they transport, their business performance is not directly connected with the price of oil or gas. However, commodity prices can have implications as there are indirect connections between energy prices and the performance of midstream MLPs, even though profitability may not be directly impacted by commodity price fluctuations. If commodity prices are very low, upstream companies will drill less and demand will fall for gathering pipelines and other infrastructure. Additionally, in an environment with falling commodity prices, investor psychology may connect energy infrastructure with the broader energy sector and commodity prices beyond what the underlying business models would otherwise indicate. In other words, commodity prices can impact sentiment for MLPs.

Interest Rate Risk – Because many investors have historically owned MLPs for yield, they have been perceived to trade similarly to yield instruments such as bonds or yield asset classes like utilities and REITs. For MLPs, rising interest rates can be a headwind in two ways: 1) fixed-income investments become more attractive, increasing competition for investor dollars among yield vehicles, and 2) borrowing costs rise. The higher yield of MLPs in comparison to other yield-oriented investments like REITs and utilities may help insulate them from the impact of rising rates. Another contributing factor that helps MLPs offset the impact of rising rates is continued distribution growth. For further explanation, please see Alerian’s piece from January 2022, Midstream/MLPs Resilient in Periods of Rising Rates.

Legislative Risk – Legislative risk mostly stems from the potential that Congress could change or abolish the beneficial MLP tax structure. Most MLP industry analysts, together with Alerian, view a change in the MLP tax status as unlikely. In recent years, bipartisan legislation has been introduced to extend the MLP structure to renewable energy

Environmental Risk – Some pipelines in major transportation corridors were constructed in the 1950s and 1960s. An aging pipeline system as well as high-profile oil spills and gas leaks have increased investor concerns regarding transportation safety and environmental risks. Pipelines are by far the safest form of transportation for oil and natural gas. Increased maintenance and new technologies enabling more frequent and accurate monitoring of pipelines has helped improve pipeline safety.

Alternative Energy and Demand Destruction – The potential for alternative energy (solar, wind, hydro, electric vehicles, etc.) to replace hydrocarbon-based energy is a long-term risk for energy infrastructure MLPs as demand for the products handled by midstream companies could change. Energy transitions tend to take many years, but energy infrastructure MLPs are actively evaluating opportunities in alternative energy today. Perhaps, pipelines could be repurposed in the future to transport captured carbon dioxide or hydrogen. Existing infrastructure assets should be largely compatible with drop-in fuels like renewable natural gas or renewable diesel that have a similar chemical makeup as their hydrocarbon-based counterparts. The adoption of alternative energy sources represents a risk for energy infrastructure but may also provide opportunities.

Recontracting Risk – Recontracting refers to midstream companies having to renew or establish new contracts with customers when existing long-term agreements expire. Market dynamics may have changed since previous agreements were put into place, potentially making it difficult to sign contracts with a similar fee structure. Companies often stagger their agreements across their asset base and even for a single pipeline to help mitigate recontracting risk.

Regulatory Risk – Government policies impacting the production of oil and natural gas or the regulation of pipelines could have implications for energy infrastructure companies.

Permitting Risks – The permitting process for a new pipeline involves federal and state government approvals and permits, as well as environmental impact studies and potentially eminent domain complications. Each state has its own regulations, and pipelines often pass through many states. Should an approval not be granted (or conditionally granted), a pipeline may need to be rerouted, which is an expensive and time-consuming necessity. Any delays or cost overruns in the permitting process may make the project less profitable, as well as potentially prevent the pipeline from being built, resulting in lost sunk costs for the company. With fewer major new-build pipelines under construction, permitting risk has become less relevant for many midstream companies.