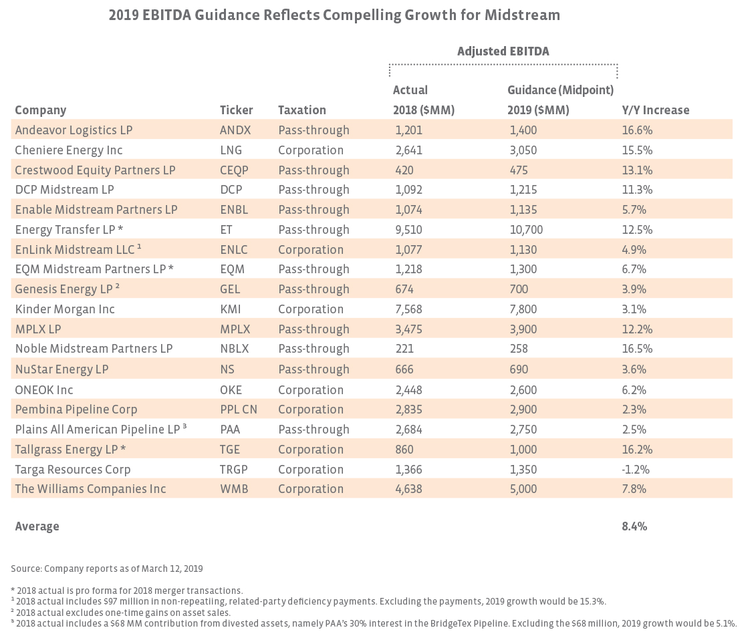

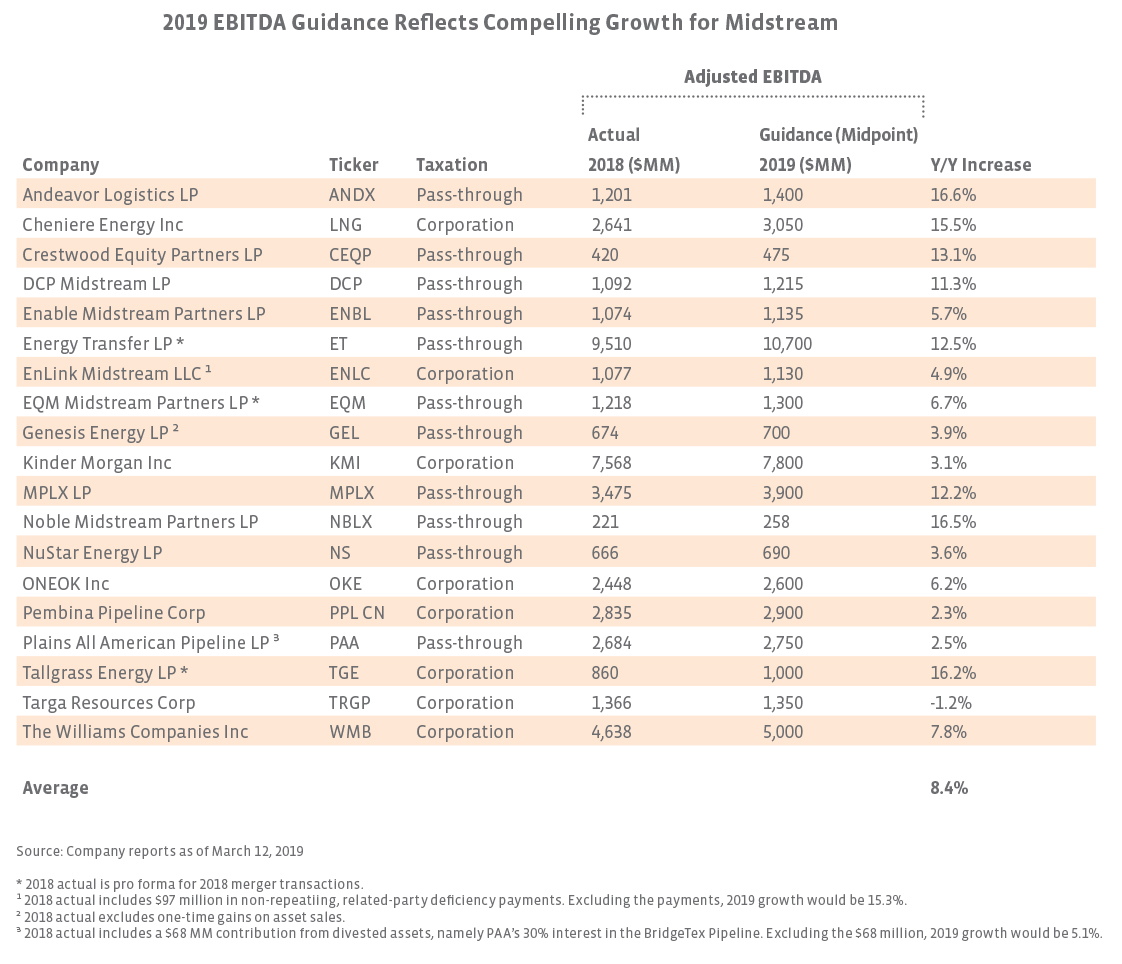

While the data table includes footnotes, additional context around adjustments may be helpful. Tallgrass Energy’s (TGE) 2018 actual EBITDA is pro forma for the merger of TEP and TEGP. Similarly, for EQM Midstream (EQM), the 2018 actual includes EBITDA from Rice Midstream Partners (former ticker RMP) prior to the merger and the pre-acquisition results of dropdown assets acquired in May 2018. Without these adjustments, guidance would have implied 2019 EBITDA growth of 53% and 30%, respectively. Please also note that EQM’s 2019 EBITDA guidance predates its acquisition announced last week.

In some cases, not adjusting numbers resulted in lower EBITDA growth. Specifically, Plains All American (PAA) and EnLink Midstream (ENLC) would have higher 2019 growth (see footnotes in table for the rate) if we had adjusted 2018 EBITDA for PAA’s BridgeTex sale and for ENLC’s non-repeating deficiency payments received in 2018. To be conservative, we did not adjust 2018 EBITDA lower for these items.

For other names, the 2019 growth numbers benefit from dropdowns or acquisitions completed in 2018, which will provide a full year’s contribution in 2019. MPLX (MPLX) closed on a major dropdown expected to generate $1 billion in annual EBITDA on February 1, 2018. If the dropdown assets had been held for the full year (i.e. one more month), 2018 EBITDA would have been modestly higher, implying a slightly lower 2019 growth rate. MPLX also acquired an export terminal in late September 2018, which will contribute to 2019 growth. In other words, MPLX’s 2019 EBITDA growth benefits from the full-year contribution of 2018 acquisitions (i.e. not just organic growth). Noble Midstream Partners (NBLX) similarly closed on a joint venture acquisition on January 31, 2018, for which we made no adjustment. Finally, Andeavor Logistics (ANDX) also completed a significant dropdown in August 2018, which will contribute to 2019 growth.

What can we learn from the data?

Of the nineteen midstream companies included above, nine are guiding to double-digit EBITDA growth next year. Some are benefitting from full-year contributions from 2018 acquisitions as noted, but others are seeing largely organic growth. For example, Cheniere’s (LNG) 2019 EBITDA benefits from the recent completion of Sabine Pass Train 5 and Corpus Christi Train 1. EBITDA growth for DCP Midstream (DCP) reflects increased volumes on its NGL pipelines, increased processing capacity, and other projects coming online in 2019. NBLX’s growth similarly reflects increasing volumes in its gathering and water services businesses. Even large companies stand out for expecting significant growth, including Energy Transfer (ET) and Williams (WMB) with growth of 12.5% and 7.8%, respectively. To be clear, WMB plans to update 2019 financial guidance with its 1Q19 results, as mentioned in yesterday’s press release announcing a joint venture in the Marcellus and Utica with Canada Pension Plan Investment Board. On the other hand, Targa Resources (TRGP) attracts attention for a slight decline in 2019, but for context, TRGP’s guidance reflects the recent sale of a 45% interest in its Badlands assets as well as lower commodity price assumptions for the year. Also, to be fair, TRGP is guiding to 50% EBITDA growth in 2020 (that’s not a typo).

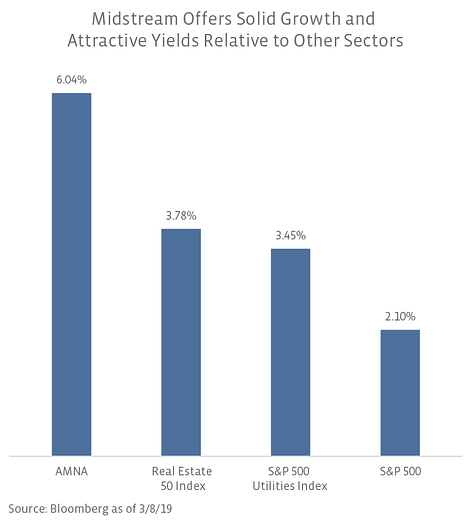

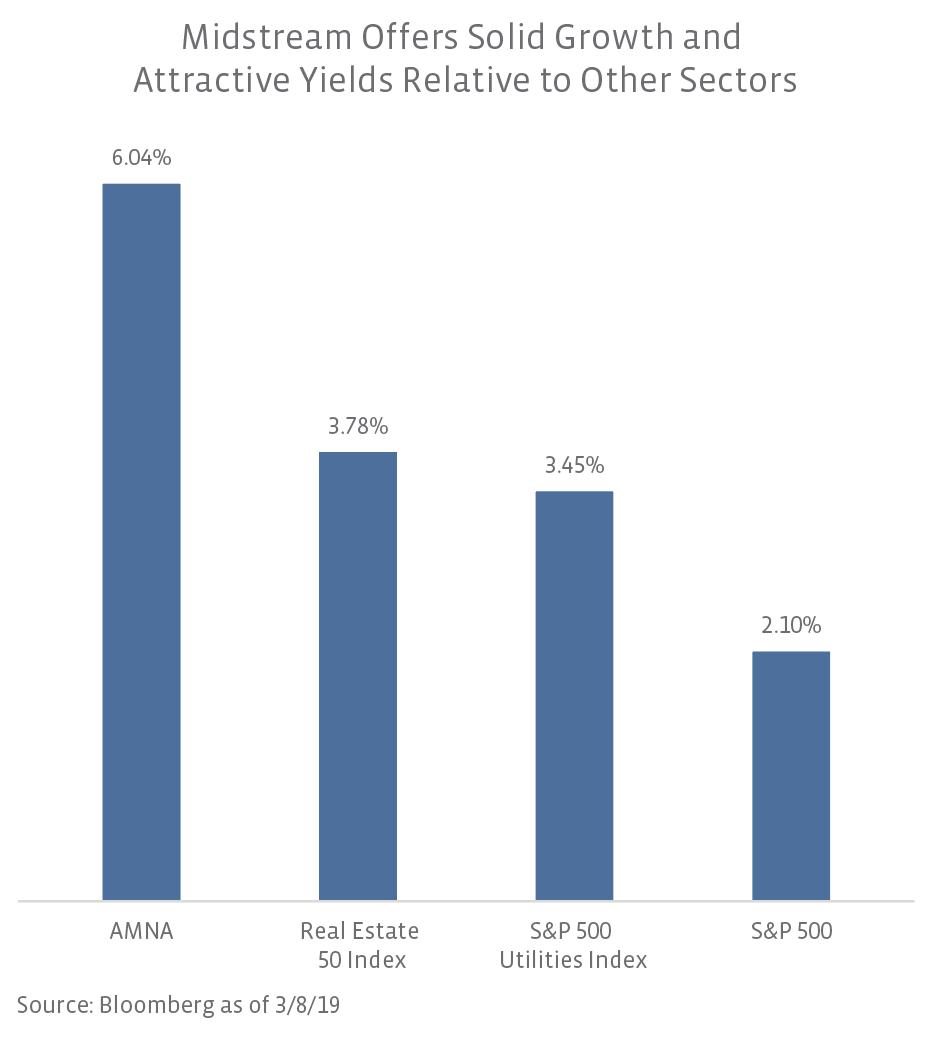

How does expected midstream growth stack up against other sectors?

Not every midstream company provides guidance, and we have intentionally excluded some names that are showing lofty 2019 growth due to acquisitions. For the nineteen companies above, the average growth of 8.4% is robust considering the strong base for 2018 EBITDA. If we had been less conservative in our treatment of PAA and ENLC, the average for the group would be 9.1%.

How does this compare to other sectors and the broader market? Per Bloomberg, EBITDA growth for the Real Estate 50 Index is expected to be 4.6% this year, following a slight decline in 2018. For the S&P 500 Utilities Index, 2019 EBITDA growth is estimated at 24.1% after a 13.6% decrease in 2018. The elevated growth for the utilities index in 2019 is likely skewed by recently completed acquisitions. EBITDA growth for the S&P 500 (just over 20% weighted to information technology) is projected at 15.2% this year, after growing by 7.8% in 2018. All in all, the midstream group’s average growth of over 8.0% for 2019 stacks up favorably. In addition to growth, midstream, as represented by the Alerian Midstream Energy Index (AMNA) in the chart below, offers more attractive yields than other sectors or the broader market.

Bottom line

The outlook for 2019 EBITDA growth for the midstream space is strong, reflecting the constructive fundamentals created by growing US energy production and rising exports. By definition, growth companies generate significant cash flows (or earnings) at a rate faster than the economy grows and have ample opportunities to reinvest in their business. Not only is midstream checking those boxes, but midstream is also paying attractive dividends/distributions – a quality that’s atypical of most growth companies. If you don’t think of midstream as a growth business, it may be time to reconsider.

{kind=link}

{kind=link}