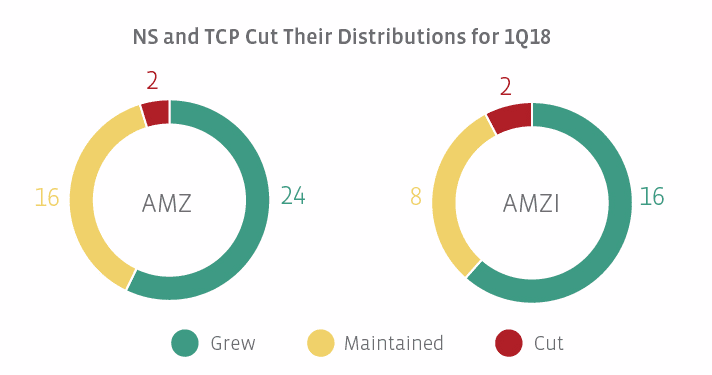

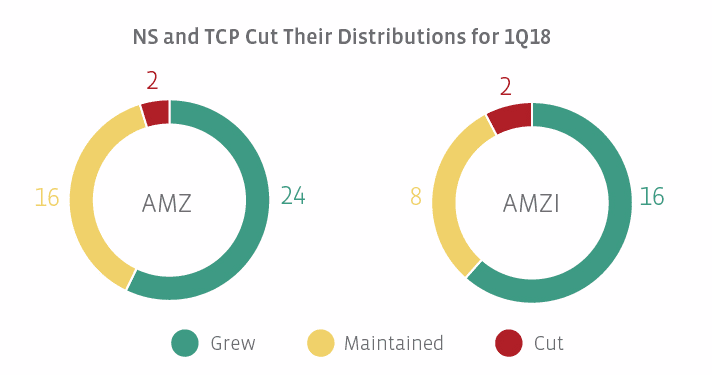

AMZ and AMZI constituents NuStar Energy (NS) and TC Pipelines (TCP) cut their distributions for 1Q18. In February, NS announced that it would cut its 1Q18 distribution to $0.60 (from $1.095) alongside the news that it would be merging with its parent, NuStar GP Holdings (NSH). The distribution cut was described as a necessary step to position the company for the future, while reducing leverage and future requirements to access the capital markets. TCP announced its 35% distribution cut earlier this month with its 1Q18 results. TCP cited the potential for a material decrease in cash flows from its pipelines due to FERC’s policy revision as a determining factor in reducing its distribution.

Notable Q/Q data points for the AMZ and AMZI

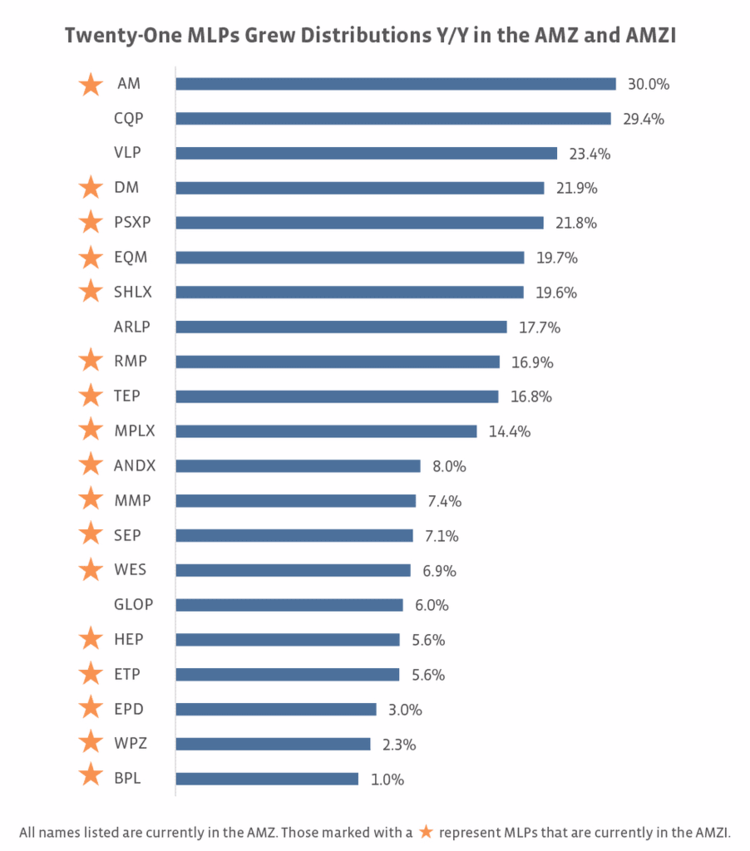

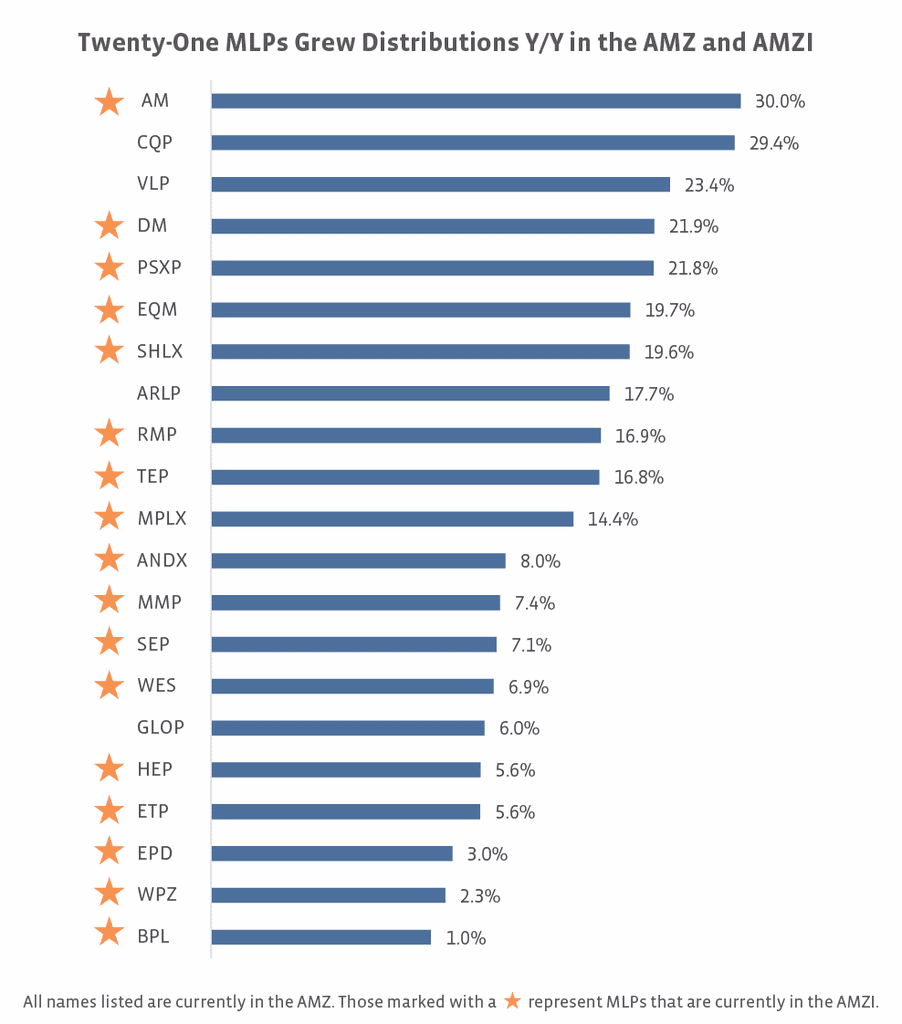

CVR Refining (CVRR) had the highest sequential increase in the AMZ. The variable distribution refining MLP raised its 1Q18 distribution to $0.51 from $0.45 in 4Q17 – a 13.3% increase. Other AMZ constituents with double-digit percentage increases were Cheniere Partners (CQP), which increased its distribution by 10.0% to $0.55, and Hi-Crush Partners (HCLP), which increased its distribution by 12.5% from $0.20 to $0.225.- Among AMZI constituents, Antero Midstream (AM) had the largest Q/Q increase, with its 1Q18 distribution of $0.39 representing a 6.9% increase from 4Q17.

- Five constituents of the AMZI grew their distributions by more than 4%: AM, Dominion Midstream (DM), Phillips 66 Partners (PSXP), Rice Midstream Partners (RMP), and Shell Midstream Partners (SHLX).

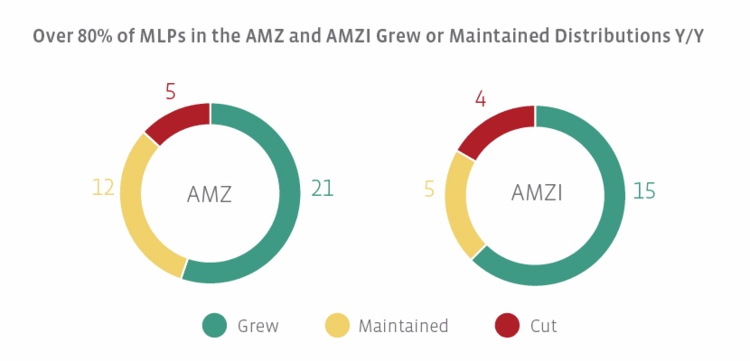

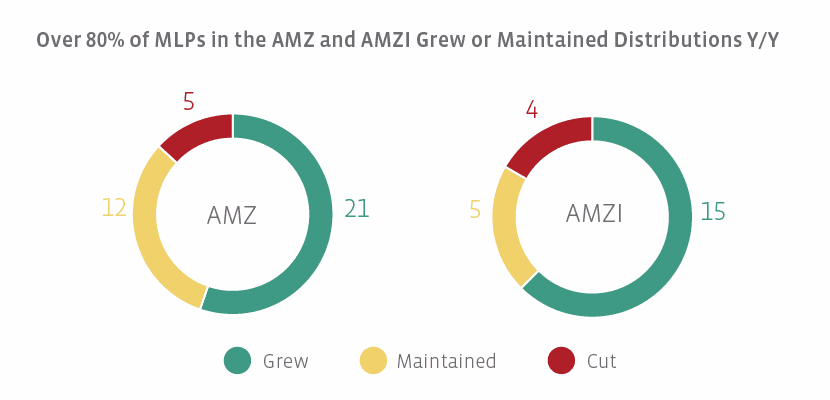

Most constituents grew their distributions on a year-over-year basis

The charts below compare the 1Q18 distribution with the 1Q17 distribution. If the name was in the index in both 1Q17 and 1Q18, its distributions were compared. Please note that there is survivorship bias in this method.

The chart below shows those AMZ and AMZI constituents that grew their distributions on a year-over-year basis.

Names that maintained their distribution in 1Q18 relative to 1Q17 include (names with a star are also in the AMZI):

AmeriGas Partners (APU)

Boardwalk Pipeline Partners (BWP)

Crestwood Equity Partners (CEQP)

DCP Midstream (DCP) *

Enbridge Energy Partners (EEP)

Enable Midstream Partners (ENBL)

EnLink Midstream Partners (ENLK)

Golar LNG Partners (GMLP)

NGL Energy Partners (NGL)

Summit Midstream Partners (SMLP)

Sunoco (SUN)

Teekay LNG Partners (TGP)

While most MLPs grew or maintained their distributions y/y, those MLPs whose 1Q18 distributions were lower than their 1Q17 distributions in addition to TCP and NS, include Plains All American (PAA), Genesis Energy (GEL), and Suburban Propane Partners (SPH). PAA and GEL are constituents of the AMZI Index, while SPH is only included in the AMZ Index.

So what?

Most MLPs in the AMZ and AMZI continue to grow their distributions, but the distribution cuts tend to detract from that fact. Distribution cuts add to the headline risk we’ve seen in the sector and distract from the positive fundamentals in the MLP space – WTI crude above $70 per barrel, US oil and gas production growing, MLPs announcing new projects, exports growing. We think a few cut-free quarters would help investors become more comfortable with the MLP space in general. If investors aren’t distracted by the bad news of distribution cuts, there may be more room in the limelight for fundamentals and MLPs’ growth projects.

{kind=link}

{kind=link}

{kind=link}