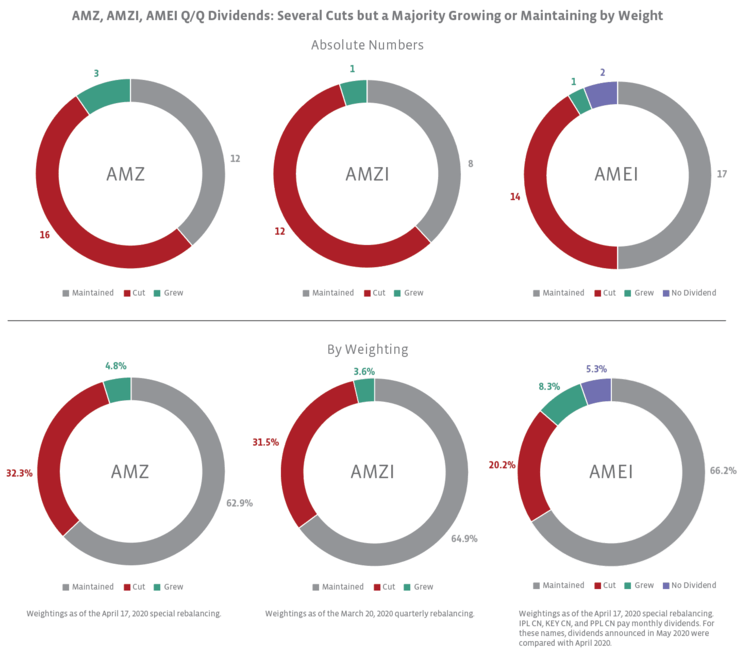

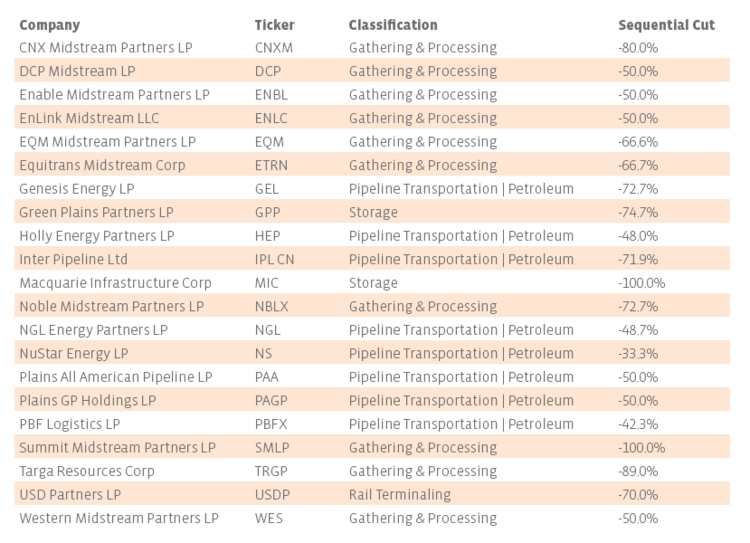

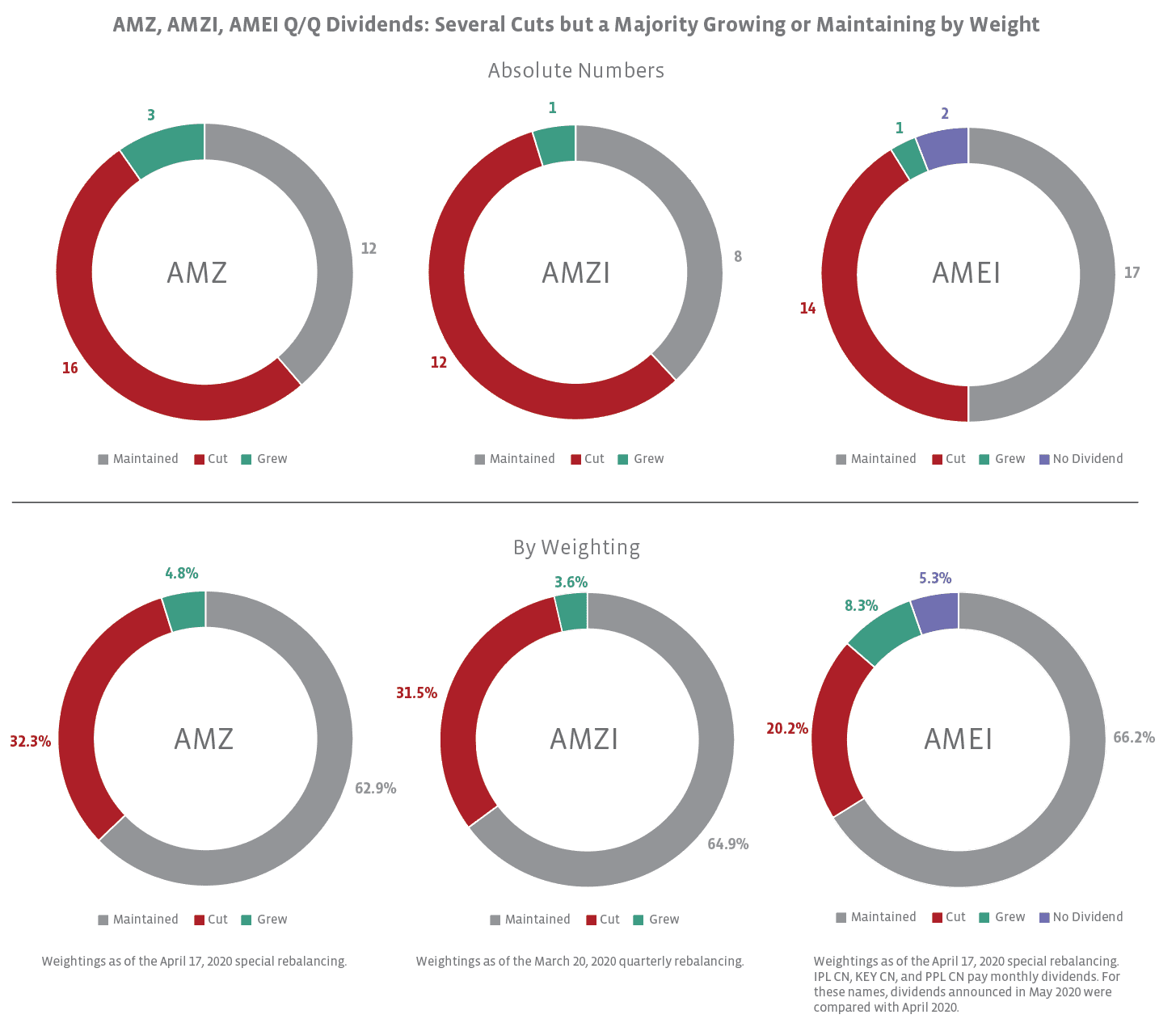

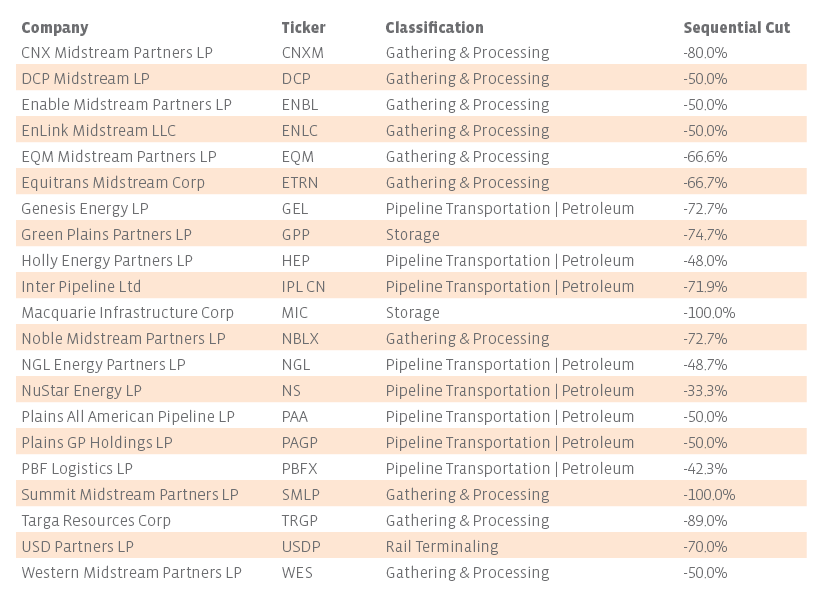

Dividend cuts were common for 1Q20 as midstream companies revised their dividend policies in response to headwinds caused by the COVID-19 pandemic and commodity price volatility, with many focused on financial flexibility and shoring up their balance sheets. For 1Q20, 16 MLPs in the AMZ, 12 MLPs in the AMZI, and 14 midstream companies in the AMEI cut their dividends quarter-over-quarter. Altogether, 21 out of 48 dividend-paying midstream companies reduced their payouts for 1Q20.The average dividend decrease was more than 50% for the constituents in each of the three indexes. Summit Midstream Partners (SMLP) and Macquarie Infrastructure (MIC) elected to suspend their dividends, while Green Plains Partners (GPP), CNX Midstream (CNXM), Genesis Energy (GEL), Noble Midstream Partners (NBLX), Inter Pipeline (IPL CN), and Targa Resources (TRGP) each cut by 70% or more sequentially (see the Appendix for a full list of cuts). The companies that decreased their dividends were more likely to be smaller companies with higher exposure to gathering and processing or petroleum pipelines. Several constituents that cut their dividend also had above average leverage and below average distribution coverage compared to the rest of the space. Many of the companies that cut their dividends said they would use the cash savings to strengthen their balance sheets and enhance financial flexibility.

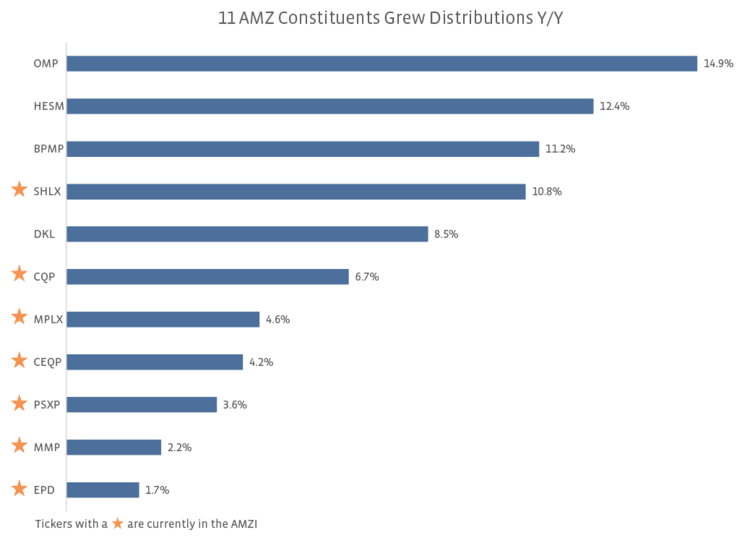

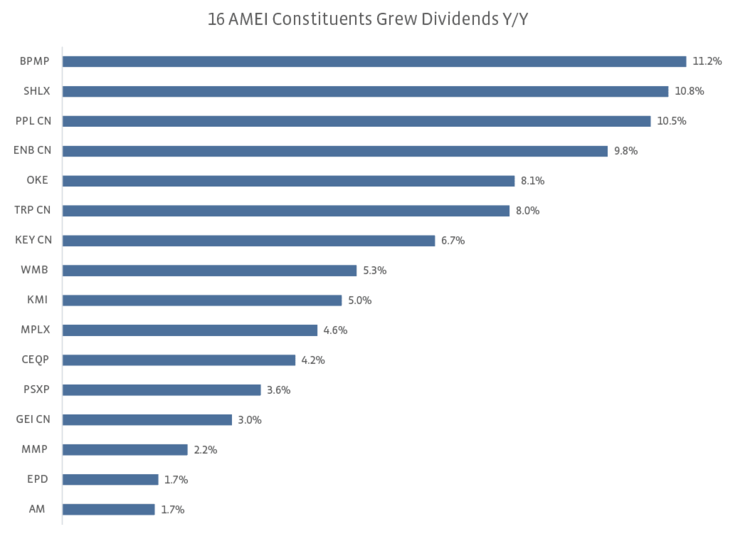

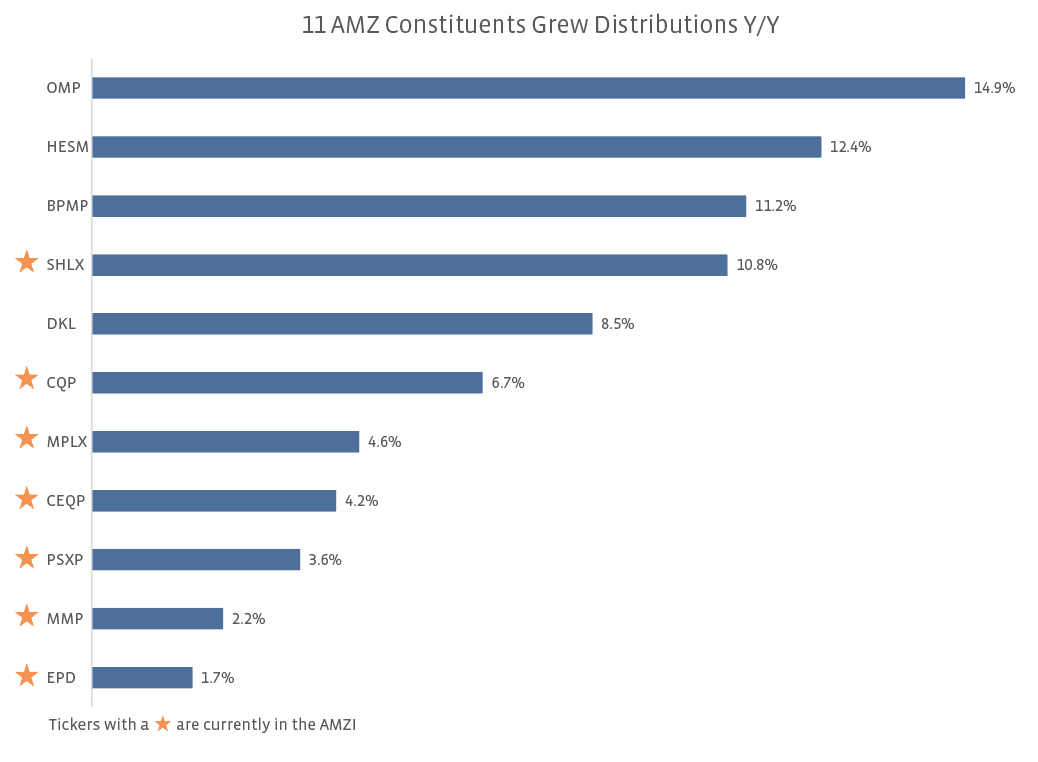

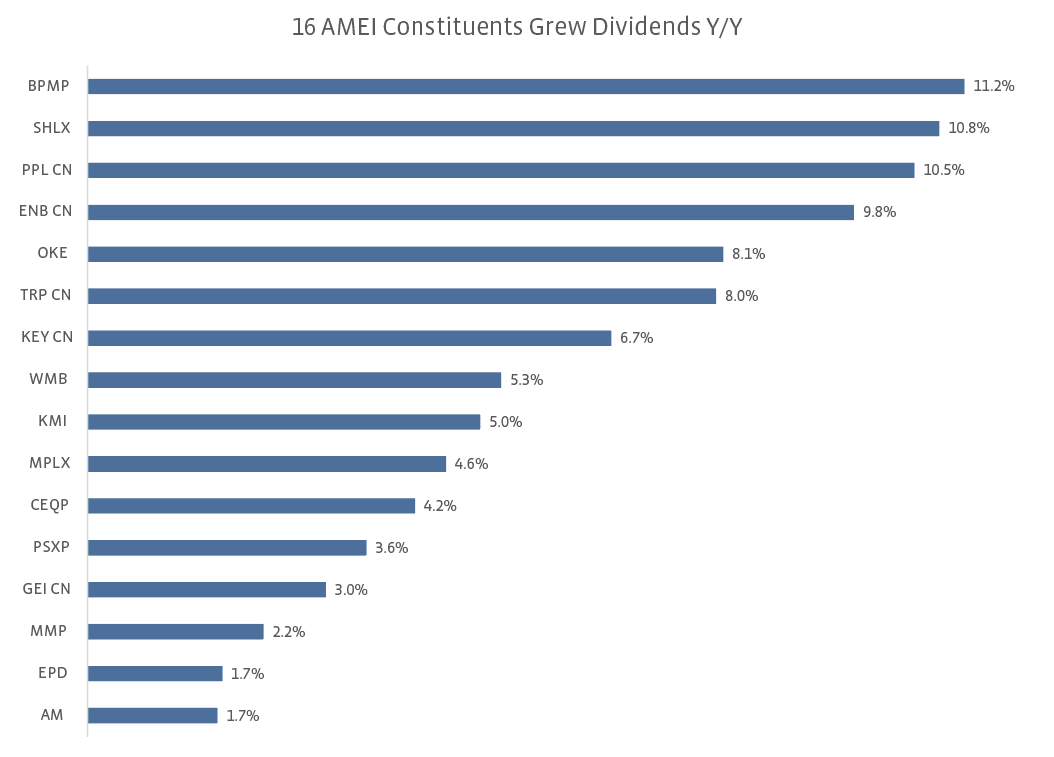

A handful of midstream companies increased their dividends for the quarter. In the AMZ, Hess Midstream (HESM) and Delek Logistics (DKL) grew their distributions modestly at 1.2% and 0.6% on a quarter-over-quarter basis, while Cheniere Energy Partners (CQP) was the sole grower in the AMZI with a 1.6% sequential increase. CQP also maintained previous full-year distribution guidance of $2.60 per unit at the midpoint, implying year-over-year growth of 5.7%. In the AMEI, Kinder Morgan (KMI) increased its dividend by 5% to $0.2625 per share, below the company’s previous 25% annual growth guidance. KMI said it would reconsider an increase to $1.25 per share on an annualized basis for 4Q20 at its January 2020 board meeting if the economy returns to normal.

Although 1Q20 was undoubtedly a difficult quarter for the midstream space in terms of the absolute number of cuts, the majority of companies in each index by weighting maintained or grew their dividends on both a quarter-over-quarter and year-over-year basis. With the announced cuts being tilted toward smaller names in the indexes, large, diversified midstream companies have been well positioned to absorb the impact of the current downturn as a result of having better financial positioning overall, higher exposure to fee-based activities with contract protections, and a diversified asset base. For these companies, dividends have proven resilient so far.

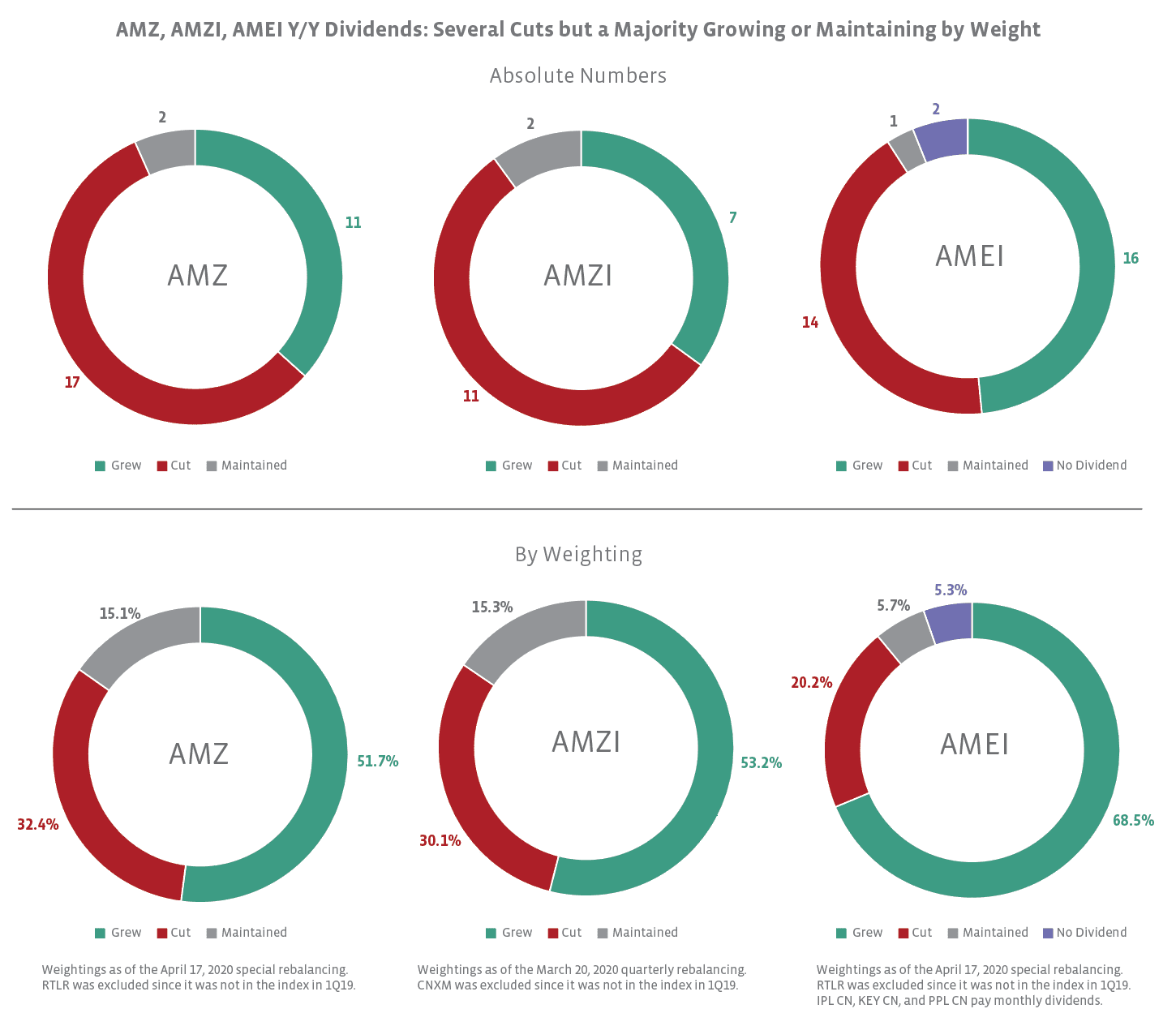

The majority of midstream constituents grew or maintained dividends over 1Q19.

The charts below compare the 1Q20 dividend with the 1Q19 dividend for the constituents that were in the indexes in both periods. Note that this approach introduces survivorship bias. For the AMZ and AMEI, Rattler Midstream (RTLR) was excluded since it was not in the index in the prior year. CNXM was excluded from the AMZI year-over-year analysis for the same reason.

Two constituents of AMZ and AMZI maintained their distribution on a year-over-year basis – Energy Transfer (ET) and TC PipeLines (TCP). ET is also in the AMEI Index. All of the year-over-year dividend cuts for the AMZI and AMEI occurred in 1Q20. The AMZ included an additional cut from Martin Midstream Partners (MMLP), which most recently reduced its distribution by 75% alongside 4Q19 earnings.

Dividend cuts not unique to midstream; larger midstream names prove resilient.

The unprecedented demand decline associated with COVID-19 and resulting commodity price volatility were playing out as midstream and other energy companies were declaring 1Q20 dividends. Among the energy complex, midstream was not unique in cutting payouts. Supermajor Royal Dutch Shell (RDS-A) cut its dividend for the first time since the 1940s, and Norwegian energy company Equinor (EQNR) also cut. Several US exploration and production companies reduced or suspended their dividends, including Occidental Petroleum (OXY), EQT Corporation (EQT), and Murphy Oil (MUR). Oilfield services bellwether Halliburton (HAL) announced a dividend cut yesterday.

While the significant number of dividend cuts across the midstream space this quarter is difficult to ignore, it is helpful to view the cuts within the context of reduced payouts across energy while recognizing that many larger midstream names maintained their payouts. In the AMZI, for instance, seven of the eight largest names by weight maintained their distributions, with a similar trend holding for the AMZ and AMEI. In short, the midstream space, especially the large names, continue to demonstrate resilience amid significant macro challenges.

Appendix

Note: A correction was made to the first graphic in this post (“AMZ, AMZI, AMEI Q/Q Dividends”) at 2:30 PM ET on March 21, 2020.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}