With the calendar turning to 2021 (finally), many investors are dusting off their crystal balls and pondering the best positioning for portfolios this year. In 2020, it would have been tempting to toss out the playbook in March and move to the sidelines, but equity investors were ultimately rewarded with a 20.3% price gain in the broader market for the year as represented by the S-Network US 1000 Index. Will a set it and forget it position in broad equities work again in 2021, or will investors need to be more thoughtful in their approach? Where could there be opportunities and pockets of outperformance this year? What are potential areas of risk? Today’s note discusses potential themes and investor concerns for 2021, highlighting relevant indexes from Alerian and S-Network. Recall, Alerian’s indexing capabilities expanded tremendously through the transformational acquisition of S-Network Global Indexes, and Alerian has broadened its research content to support a wider suite of indexes. The appendix to this note includes a list of indexes referenced and investable products tracking those indexes.

What could do well in a COVID-19 recovery?

From a market perspective, the potential benefits of a successful vaccine started to take shape in November as Pfizer (PFE) and BioNTech (BNTX), Moderna (MRNA), and AztraZeneca (AZN) with Oxford University announced positive vaccine developments over the course of the month. Segments of the market that had performed poorly in 2020 in the wake of the pandemic saw a strong rebound, including energy, pockets of real estate, travel-related stocks and financials. While the initial trade is in the rearview, the momentum for these sectors could continue into 2021 as vaccines are distributed. These sectors could also see benefits from a rotation into value (discussed more below). For energy, the worst-performing sector in 2020, West Texas Intermediate oil prices ended the year down 20.5% at $48.52 per barrel, implying plenty of potential upside as demand recovers with widespread deployment of a vaccine. Admittedly, it will take time for vaccine distribution to positively impact oil demand, but equities may trade in anticipation of this improvement before it materializes similar to what was seen with vaccine development. Within energy, midstream MLPs and corporations provide leverage to a recovery in the outlook for the global economy and oil demand, with the potential for total return further supported by attractive income, free cash flow generation and buybacks. Beyond energy, REITs could be another interesting way to play a recovery while also receiving income. Specifically, the S-Network REIT Dividend Dogs Index (RDOGX) could outperform in a COVID-19 recovery due to its overweight exposure to Hotel and Resort REITs relative to other indexes (read more).

Where can investors find income?

With the 10-year Treasury ending 2020 at a yield of 0.92% and the S&P 500 yielding just 1.54%, income can be difficult to find these days. With the Federal Reserve emphasizing employment and taking a looser stance on inflation in its August policy shift, interest rates are likely to remain low for some time. Furthermore, traditional income sectors such as REITs and utilities are offering yields below their five-year averages. For investors searching for yield, there are compelling income opportunities in the market as exemplified by the chart of select Alerian and S-Network indexes shown below. Midstream energy infrastructure continues to provide attractive income and the potential for total return thanks to discounted valuations relative to historical averages, growing free cash flow generation, and buyback authorizations. More broadly, the S-Network Dividend Dogs Indexes are designed to provide above average yield and diversification by selecting the five companies with the highest dividend yields across ten sectors. As discussed more below, these indexes also offer the potential to benefit from mean reversion over time. Closed-end funds (CEFs) can also help enhance a portfolio’s yield. The S-Network Closed-End Fund Indexes shown in the chart utilize a smart beta weighting approach to give a greater weighting to the CEFs trading at larger discounts, which helps lead to more attractive yields.

What may benefit under a Biden administration?

A new administration in the White House brings with it additional considerations for investors based on policy plans and expectations. Alternative Energy was a standout performer in 2020 with the Ardour Global Alternative Energy Extra-Liquid Index (AGIXL) gaining 118.3% on a price-return basis for the year. While the momentum behind the space was expected to continue regardless of the election outcome, a Biden Administration is likely to lend further support as it takes steps to combat climate change. For more information on other key themes and trends in alternative energy, please see Alerian’s recent white paper.

In addition to alternative energy, infrastructure stands out as another sector that stands to benefit from a Biden presidency. The Biden-Harris transition team has laid out several administration priorities once the president-elect takes office this month, with infrastructure playing a role in two facets of the plan. In considering ways to boost the economic recovery, Biden is seeking greater investment in modern infrastructure related to transportation, energy, water, and internet access. These areas are also a key part of his clean energy plan by emphasizing the buildout of infrastructure that is sustainable and can withstand the effects of climate change.

Value vs. Growth

In the push and pull between value and growth, it may feel like value is overdue for a rotation and positive sentiment, but there have been a fair share of false dawns for value in recent years. Value clearly shined in November, but will 2021 see a sustained rotation into value or a return to momentum in growth? For those anticipating a value recovery, one way to play it is to shift into value-oriented sectors, such as energy, financials, and materials. Another option is to invest in broader value products or funds providing more diversified exposure. For example, the S-Network Dividend Dogs Indexes have a value tilt by including the five highest-yielding names in each of ten sectors. The high yields imply discounted valuations, which would be expected to improve over time with reversion to the mean. The yield for these indexes tend to be at a relative high after the annual reconstitution, which was completed at the close of trading on December 18, 2020.

Investors expecting growth to continue to outperform have similar options from an investment standpoint, whether it’s investing in a broad growth product or overweighting growth-focused sectors. In terms of sectors, technology has been the clear standout this year as the pandemic has forged a greater dependence on the internet and the virtual world. The O’Shares Global Internet Giants Index (OGIGX), which is owned by O’Shares ETF Investments and calculated by S-Network Global Indexes, exemplifies these trends (read more). OGIGX’s unique index construction emphasizes inclusion of fast-growing global technology companies with screens that account for profitability and balance sheet quality. The combination of these screens as well as diverse geographic and technology exposure have contributed to OGIGX’s outperformance in recent years compared to indexes only focusing on old technology companies or US names alone. Also from a sector perspective, alternative energy stands to benefit from further investor preference for growth stocks even after notching impressive gains in 2020. Given the constructive long-term projections for the adoption of clean energy globally, these companies are at the forefront of one of the most prominent growth trends in investing today.

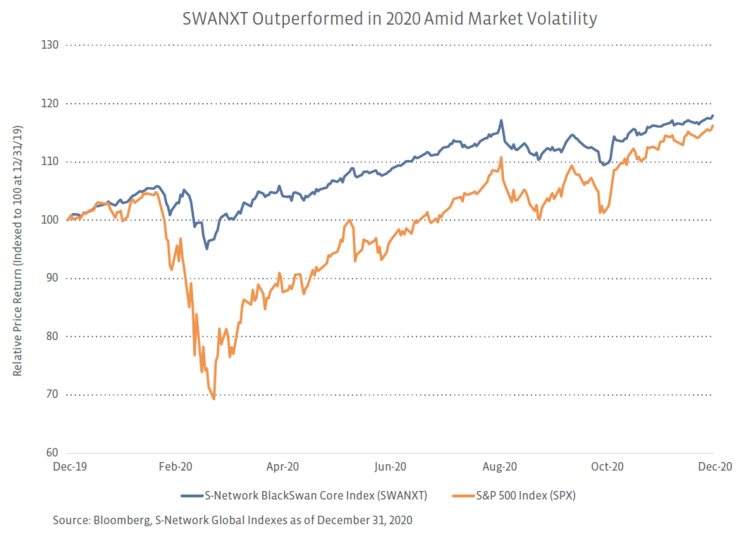

What about investors fearing another pullback or skeptical of a recovery?While it may feel like the broad market just keeps going up, some investors are likely concerned about a correction or another unforeseen event that could have a dramatic impact on markets similar to COVID-19 in March 2020. For these investors, it may be tempting to just hold cash, but today there are more sophisticated options to position for an anticipated pullback while maintaining upside potential if the market continues to rise. For example, the S-Network BlackSwan Indexes minimize volatility through a 90% allocation to US Treasuries but aim to provide capital appreciation through exposure to long-dated, in-the-money call options that round out the index. The S-Network BlackSwan Core Index (SWANXT) allocates to options on the SPDR S&P 500 ETF Trust (SPY), while the S-Network International BlackSwan Index (ISWNXT) allocates to options on the iShares MSCI EAFE ETF (EFA). The strategy for these indexes was validated in the volatility of early 2020 as exemplified by SWANXT’s performance shown in the chart below. From its relative peak on February 19 to its low on March 23, 2020, the S&P 500 fell 33.9% compared to an only 8.6% decline for SWANXT. While 2020 provided a case study for the advantages of these indexes, a headline or geopolitical event could rock markets at any time, making these strategies relevant well beyond the pandemic.

Another option for investors cautious on 2021 would be to emphasize quality in their allocations. Some of the hallmarks of quality companies are strong balance sheets, solid earnings profiles, and stable dividends. Admittedly, these characteristics can be attractive against any market backdrop. However, if the macro environment is challenging or a recovery stalls, quality stocks may prove a relative safe haven. The suite of O’Shares Quality Dividend Indexes, which are owned by O’Shares ETF Investments and calculated by S-Network Global Indexes, were designed to provide exposure to quality companies with an emphasis on the goals of income, wealth preservation, and capital appreciation.

What if inflation is a concern?

Stimulus spending and the Federal Reserve’s swelling balance sheet, along with the Fed’s August policy change, have raised inflation concerns for some. Others point to the ongoing repercussions of the pandemic, such as lower demand, increased saving and a weakened economy, as reasons for inflation to remain a non-issue. Admittedly, inflation in the US has been muted for some time. As noted in Alerian’s white paper on real asset investing, the Consumer Price Index (CPI) has not risen by more than 2.4% on an annual basis since 2011. However, for investors concerned with inflation, real assets such as commodities, precious metals, real estate, and infrastructure, including energy infrastructure and utilities, tend to provide an inflation hedge. In years of elevated inflation, real assets have tended to outperform the broader market as discussed in the white paper. For investors looking for a hedge against inflation along with high relative yields and diversification to broader equities, midstream, REITs, or infrastructure may all be attractive options. Other indexes with real asset exposure include the VanEck Natural Resources Index (RVEI) and S-Network Microsectors Gold Miners Index (MINERS).

Conclusion

While no one expected 2020 to play out as it did, expectations continue to inform investment decisions and allocations. This note has only highlighted a couple potential themes for 2021 and related ways to position in anticipation of those themes. While some ideas seem to garner greater conviction, such as an eventual COVID-19 recovery and certain sectors benefitting under the new administration in the White House, other calls, such as a sustained value rotation, are arguably more difficult to make. Investors must ultimately make decisions based on their views and convictions with today’s note simply framing some of the considerations that may be top of mind for 2021.

Appendix

| Index Mentioned |

Linked Product |

| ETRACS Alerian Midstream Energy Index ETN (AMNA) |

|

| ETRACS Alerian Midstream Energy High Dividend Index ETN (AMND), Alerian Midstream Energy Dividend UCITS ETF (MMLP) |

|

| Alerian MLP ETF (AMLP), ETRACS Alerian MLP Infrastructure Index ETN Series B (MLPB) |

|

| JP Morgan Alerian MLP Index ETN (AMJ) |

|

| ALPS Sector Dividend Dogs ETF (SDOG) |

|

| ALPS International Sector Dividend Dogs ETF (IDOG) |

|

| ALPS Emerging Sector Dividend Dogs ETF (EDOG) |

|

| ALPS REIT Dividend Dogs ETF (RDOG) |

|

| Invesco CEF Income Composite ETF (PCEF), ETRACS 1.5X Closed-End Fund ETN (CEFD) |

|

| VanEck Vectors CEF Municipal Income ETF (XMPT) |

|

| VanEck Vectors Low Carbon Energy ETF (SMOG) |

|

| O’Shares Global Internet Giants ETF (OGIG) |

|

| O’Shares U.S. Quality Dividend ETF (OUSA) |

|

| O’Shares U.S. Small-Cap Quality Dividend ETF (OUSM) |

|

| O’Shares Europe Quality Dividend ETF (OEUR) |

|

| Amplify BlackSwan Growth & Treasury Core ETF (SWAN) |

|

| VanEck Vectors Natural Resources ETF (HAP) |

|

| MicroSectors Gold Miners 3x Leveraged ETN (GDXU), MicroSectors Gold Miners -3x Inverse Leveraged ETN (GDXD) |