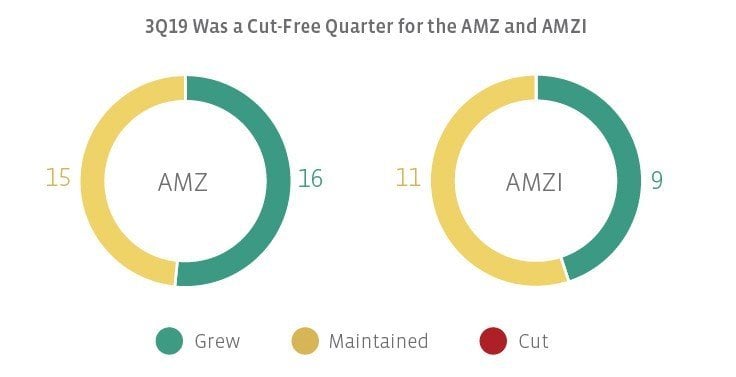

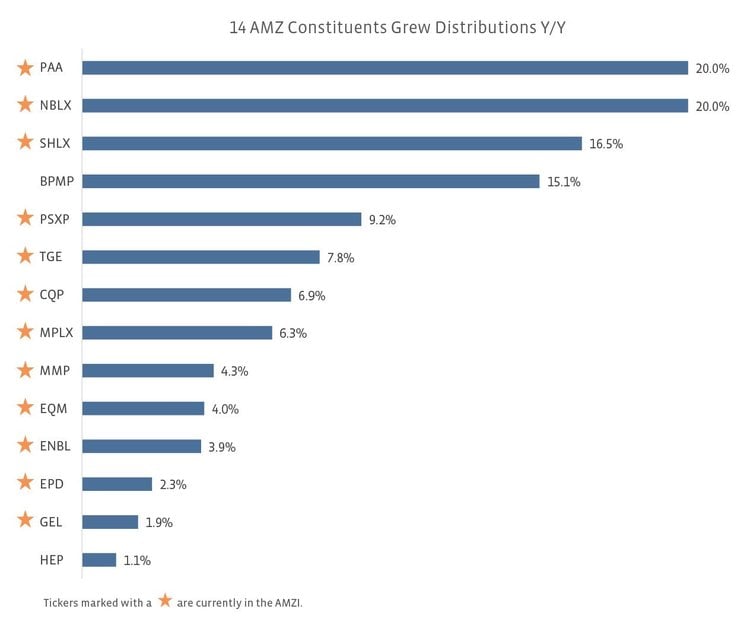

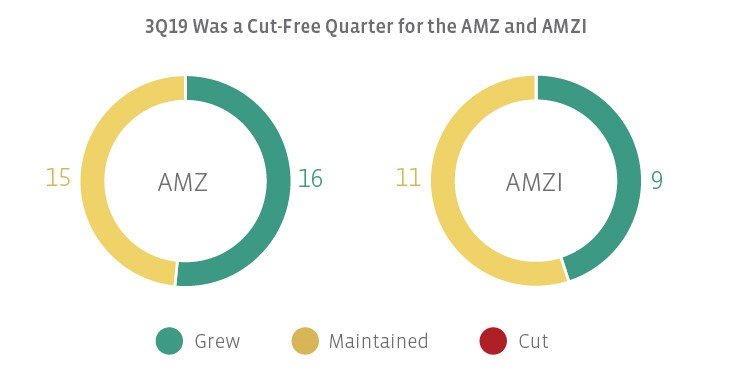

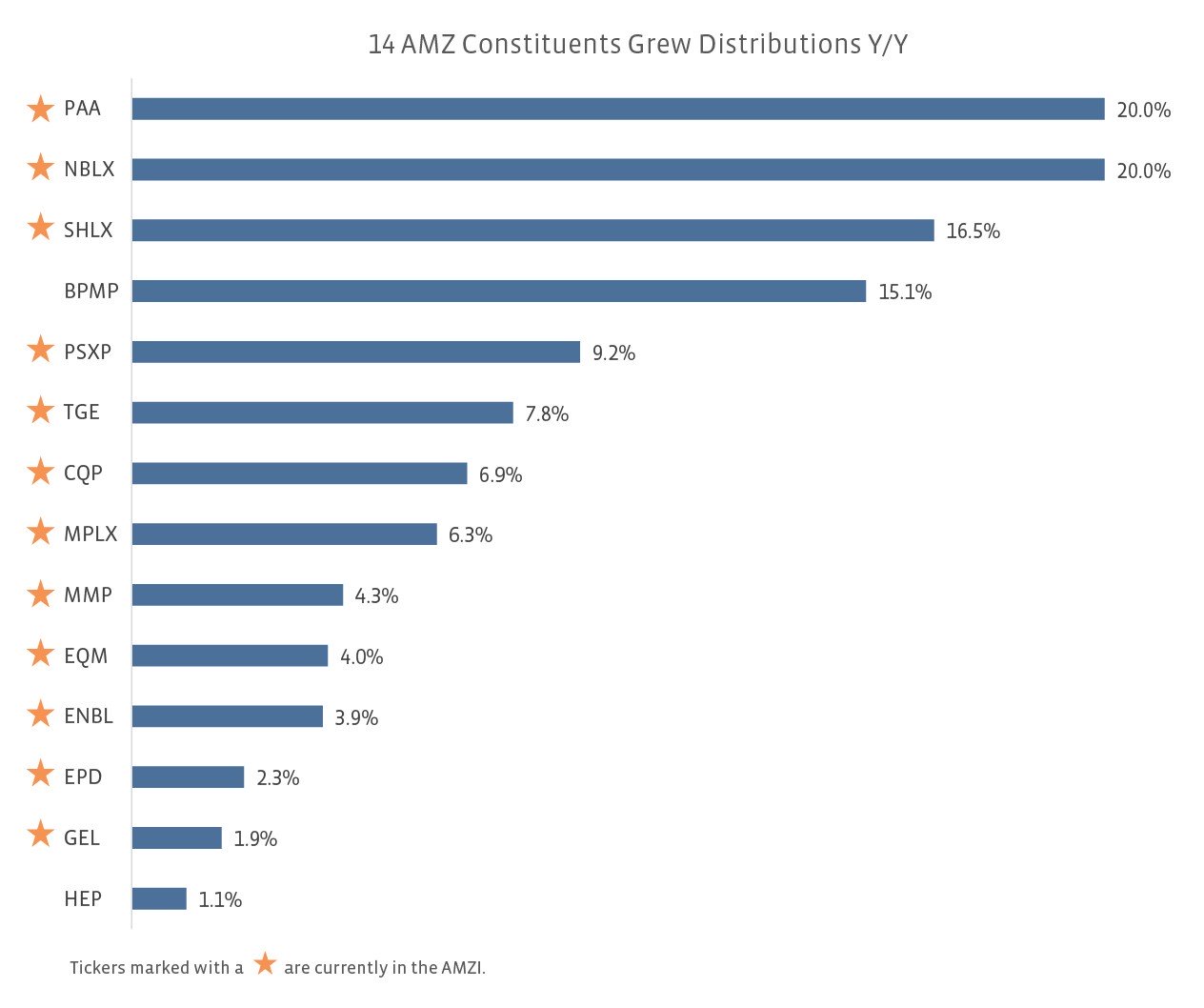

3Q19 was the first spotless quarter for AMZ and AMZI constituents in over a year. Half of AMZ constituents grew their distributions sequentially, 7 of which grew distributions by at least 3%. Oasis Midstream Partners (OMP) led the AMZ with a 5.1% distribution increase, and Noble Midstream Partners led the AMZI with a 4.6% increase. The remaining AMZ constituents, along with the majority of the AMZI, made no change to their quarterly distributions. Holly Energy Partners (HEP) kept its quarterly distribution flat for the first time in company history in order to strengthen its balance sheet and maintain a distribution coverage ratio of 1.0×. HEP expects to maintain its current distribution and coverage ratio through 2020.

Both OMP and NBLX, along with several other midstream MLPs that are growing distributions sequentially, still have their incentive distribution rights (IDRs). However, the majority of AMZ and AMZI constituents have moved to eliminate IDRs as they become a burden on the MLP’s cost of capital over time. After DCP Midstream (DCP) announced an IDR elimination alongside 3Q19 earnings, 85.9% of AMZI constituents by weighting have now eliminated their IDRs. Additionally, AMZ constituent Hess Midstream Partners (HESM) will acquire its IDRs from Hess Infrastructure Partners in a simplification transaction set to close this quarter.

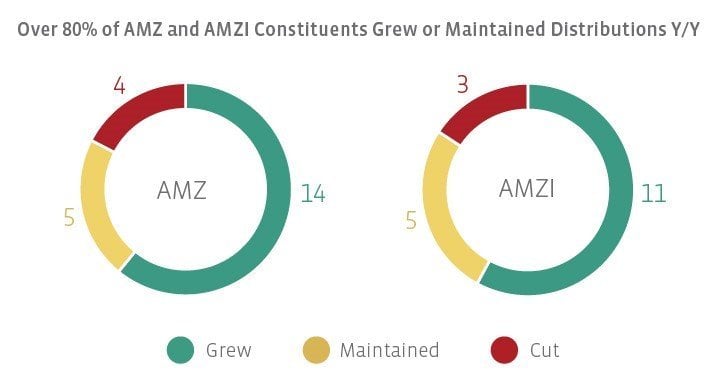

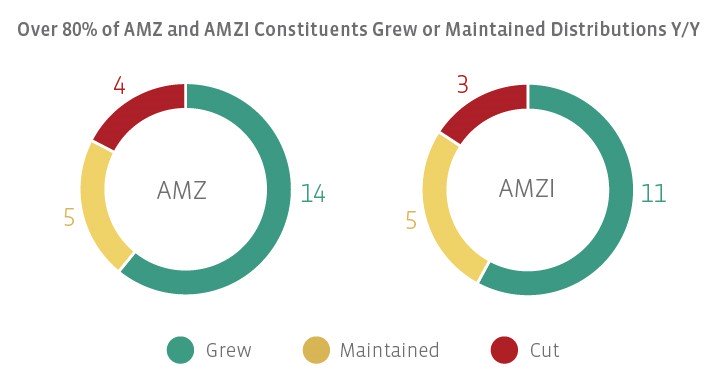

The majority of AMZI constituents have raised distributions from 3Q18

The charts below compare the 3Q19 distribution with the 3Q18 distribution for MLPs that were in the index in both periods. Note that this approach introduces survivorship bias. Nine names were excluded from the year-over-year comparison for the AMZ, primarily as a result of the December 2018 methodology change. Only one name, NBLX, was excluded from the AMZI year-over-year analysis. The 3Q19 distributions of EnLink Midstream (ENLC), Energy Transfer (ET), and Western Midstream Partners (WES) are compared to the 3Q19 distributions of the related predecessor in the index.

AMZ constituents that maintained their distribution in 3Q19 relative to 3Q18 include (all names listed are also AMZI constituents):

Crestwood Equity Partners (CEQP)

DCP Midstream (DCP)

NGL Energy Partners (NGL)

NuStar Energy (NS)

TC PipeLines (TCP)

All three of the remaining year-over-year distribution cuts in the AMZI came as a result of backdoor cuts in consolidation transactions. With consolidation transactions mostly behind the space, backdoor distribution cuts should be less frequent going forward (read more). The AMZ included an additional cut from Summit Midstream Partners (SMLP), which executed a series of strategic actions that included the elimination of IDRs and a 50% distribution cut earlier this year.

Improving AMZ and AMZI distribution profiles are reflective of positive changes in the space

Improvements in distribution trends among midstream MLPs have come alongside other positive changes the space has made, including leverage reductions, self-funding the equity portion of capital expenditures, and IDR eliminations. Distribution coverage has also improved significantly across the industry, providing investors with added comfort around yields that are above historical averages. While paying down debt, funding growth capital, and unit buybacks may take priority over distribution growth in some cases, modest distribution growth from some MLPs is a welcome sign for investors that rely on midstream MLPs for a stable stream of income.

{kind=link}

{kind=link}

{kind=link}