Diversification. Energy infrastructure provides diversification relative to broader market indices as well as other income-oriented investments. For portfolios increasingly allocated to passive products tracking well-known market indices, the diversification benefit of midstream may be particularly attractive. For example, there are currently only three midstream corporations included in the S&P 500 – ONEOK (OKE), The Williams Companies (WMB), and Kinder Morgan (KMI). MLPs are not included in broader market indices.

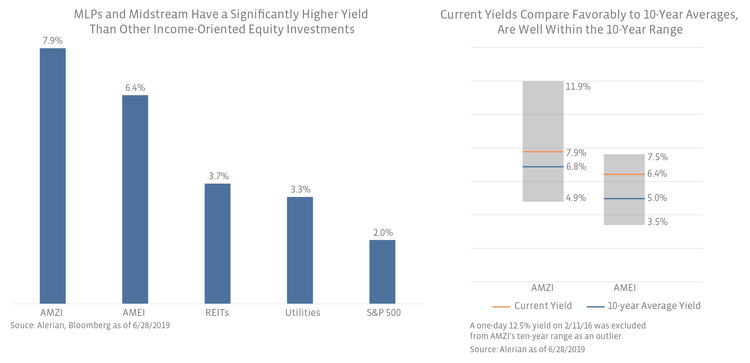

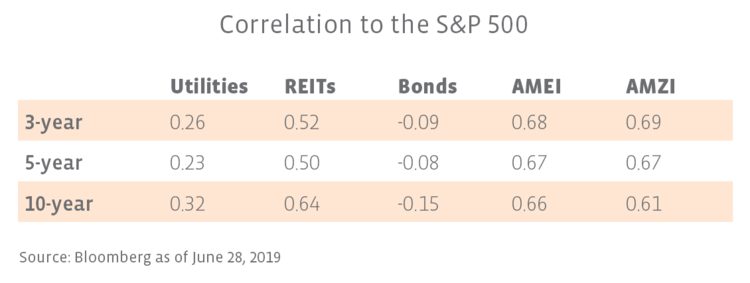

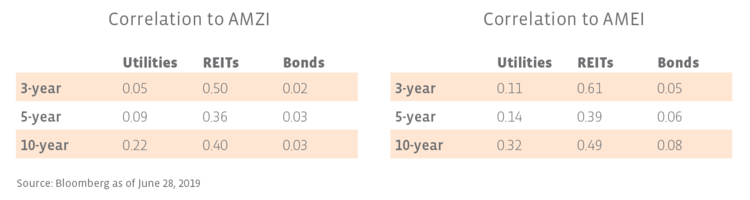

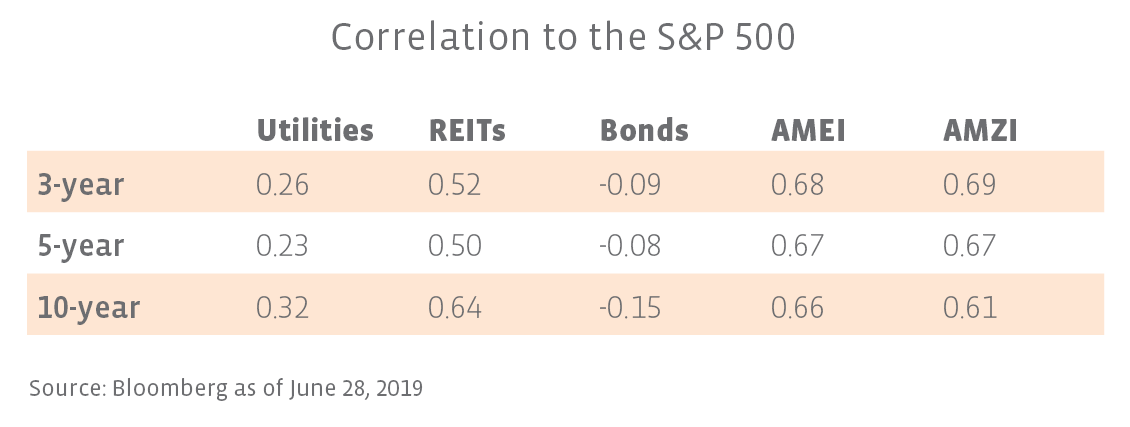

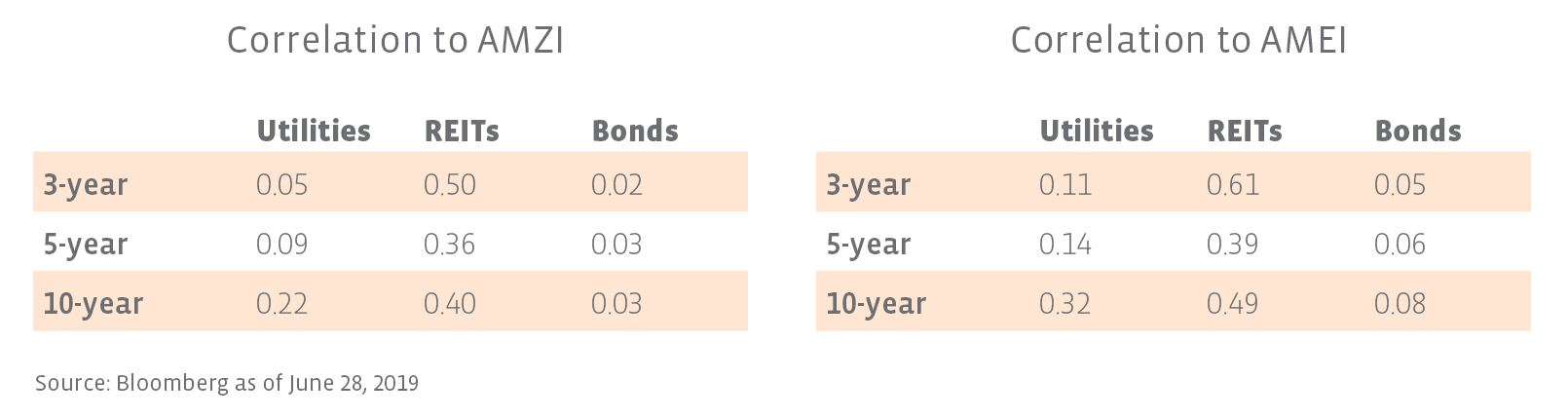

Notably, energy infrastructure has relatively low correlations with other income-oriented investments, including REITs, Utilities, and Bonds, as shown in the table below. Adding midstream to an income portfolio with these investments could provide diversification while also enhancing the income profile of the portfolio.

Real Asset Exposure. Real assets provide potential protection in an environment of rising inflation and diversification. Energy infrastructure contracts often have inflation protection built into them, and midstream assets represent “steel in the ground.”

Growth Potential. Growth companies generate cash flows (or earnings) at a faster growth rate than the broader economy and have ample opportunities to reinvest in their business. By this definition, North American energy infrastructure companies are growth companies. At the entity and index level, historical EBITDA growth numbers are often distorted by acquisitions. For a less skewed perspective, forward company guidance can be used to evaluate growth. The average implied 2019 EBITDA growth among nineteen midstream companies earlier this year was 8.4% using the midpoint of guidance and 2018 adjusted EBITDA (read more).

Over the next several years, the outlook for growth remains robust and is being driven by increasing energy production and exports from the US and Canada, which will require more energy infrastructure. Based on a 2018 study from the Interstate Natural Gas Association of America, it is estimated that the US and Canada will require $521 billion in energy infrastructure investments from 2018 to 2035 (read more). This forecast implies plentiful opportunities for midstream companies to reinvest cash flows into growth projects.

Where does energy infrastructure fit in your portfolio?

Energy infrastructure could fit in multiple portfolio sleeves depending on the objective of the investor. Typically, energy infrastructure falls into an energy, equity income, real assets, or equity growth allocation. Relative to other energy investments, midstream offers greater income, is less correlated with oil prices, and tends to perform more defensively in periods of falling crude prices (read more). Within an income sleeve, energy infrastructure can provide attractive diversification while also enhancing yield. Within an income portfolio, the weighting to energy infrastructure may be 5-10% or potentially higher depending on the portfolio’s objectives.

Bottom Line

When weighing investment options for a portfolio, the attractive qualities of energy infrastructure merit consideration. The multi-faceted benefits of an energy infrastructure allocation include income, diversification, real asset exposure, and growth potential. An allocation to energy infrastructure may fit within the energy, income, real assets, or equity growth sleeve of a portfolio. Wanting more charts, data and explanations? Please see our white paper.

{kind=link}

{kind=link}

{kind=link}