Summary

- The biotechnology sector largely underperformed the broader market this year, particularly small to mid-cap biotech indexes whose constituents tend to experience more volatility.

- Contributing factors to the market decline include fears of increased regulation and oversight of M&A transactions and drug prices against the backdrop of interim leadership at the FDA.

- November, however, brought several developments which may suggest that these concerns could be alleviating, along with news of a nomination for FDA chief.

- If broader markets remain steady and the broader biotechnology sector recovers, small to mid-cap biotech indexes could see higher return potential relative to their large cap counterparts given their weakness in 2021.

On February 9, 2021, small and mid-cap biotechnology indexes hit a record high after enjoying a newsworthy 2020. But several subsequent factors in 2021 contributed to a perfect storm that set equity prices on a downward trend, with these indexes off nearly 30%, compared to 17% gains for the S&P 500.1 Regulatory concerns and uncertainty at the FDA disproportionately weighed on small and mid-cap biotechnology companies, which tend to be more focused on developing drugs and are often takeover candidates as new drugs and therapies progress. November, however, brought several significant news items that could potentially alleviate some of these investor concerns.

Below are three headwinds that contributed to biotech sector weakness in 2021 (particularly evident in the more volatile small and mid-cap indexes), followed by recent events that may relieve sector weakness in the coming months.

2021 Headwind—FDA uncertainty: One of the largest hurdles in the biotech sector has been the absence of a permanent FDA commissioner since the beginning of the Biden presidency in early 2021. A lack of clear leadership in addition to some controversial drug decisions caused investor frustration while creating volatility in the sector. In June, the FDA approved Biogen’s (BIIB) aducanumab, the first Alzheimer drug to be approved since 2003, after an advisory panel recommended the FDA reject the drug due to lack of clinical evidence.2 In another example, the FDA rejected a highly anticipated new drug application for Acadia Pharmaceuticals (ACAD) for pimavanserin, which treats hallucinations and delusions associated with dementia.3 The initial notification of deficiencies in March 2021 caused ACAD’s stock price to drop by over 45% (not an uncommon occurrence when a drug is rejected). In general, FDA leadership uncertainty has contributed to the recent underperformance of small and mid-cap biotech stocks, since these companies are more R&D focused with multiple drugs in trial phases.

Why fears may be overblown—Biden Administration announces nomination of FDA commissioner: On November 12, 2021, President Biden nominated Robert Califf, who had previously served as FDA commissioner briefly during the Obama administration, to head up the FDA. Given Califf’s past experience as FDA commissioner along with experience in both medicine and the pharmaceutical industry, he represents someone familiar to the industry—providing investors with a known variable.

2021 Headwind—regulatory scrutiny on biotech mergers and acquisitions:

As mentioned previously, many biotech stocks are prime candidates for acquisitions by larger pharmaceutical companies, which drives significant upside potential in equity prices. For example, when MorphoSys AG (MOR) announced the acquisition of biotechnology firm, Constellation Pharmaceuticals (CNST), CNST’s stock price surged over 65% in one day. But earlier this year in March 2021, the Federal Trade Commission (FTC) increased regulatory scrutiny of biotechnology/pharmaceutical deals. The FTC launched an international working group called the Multilateral Pharmaceutical Merger Task Force to aggressively revamp its review process for anticompetitive pharmaceutical mergers. The FTC claimed that the industry has experienced a high volume of mergers, “skyrocketing” drug prices, and anticompetitive conduct. 4

Why fears may be overblown—Merck/Acceleron acquisition largest deal among pickup in deal activity in late 2021: While regulatory scrutiny created uncertainty within the sector, particularly for small to mid-cap biotech companies which often benefit from takeover premiums, 2021 has still experienced a large wave of bio-pharmaceutical mergers—particularly in 2H21. Data from BioPharma Dive suggest that 2H21 experienced 16 deals compared to 21 deals in 2H20; however, 2H21 deals still outnumbered deals in 2H18 (10 deals) and 2H19 (14 deals).5 Additionally, the largest biotech deal of 2021 was completed recently on November 22, 2021, when Merck (MRK) completed an $11.5 billion acquisition of Acceleron (XLRN). Despite experiencing some delays from the FTC antitrust committee, the MRK/XLRN deal still supports a fairly healthy biotech M&A environment in 2021. 6

2021 Headwind—regulatory impact on drug prices:

As part of his Build Back Better plan, President Biden proposed an initiative in August to reduce drug prices. The plan allowed for Medicare to negotiate prescription drug prices and also imposed a penalty on drug companies which raised prices faster than inflation.7 Logically, many investors feared that lower drug prices would deteriorate drug company margins, give drug companies less risk/reward incentive to create drugs, and have negative implications for the overall industry.

Why fears may be overblown—Medicare receives only limited pricing negotiation power: On November 2, negotiations reached on drug pricing were more lenient than initially proposed. While Medicare is allowed to impose a penalty on drug companies which raise prices faster than inflation, Medicare can only negotiate prescription drug prices on older drugs that have passed the exclusivity period for generic competition (typically nine to thirteen years). Drug companies could hypothetically offset these caps by setting higher prices for new drugs that aren’t eligible for Medicare price negotiations. While the bill may set precedent for future drug price regulations, current impact to drug companies appears limited. As noted in a Wall Street Journal article, analysts have estimated only a 3% to 5% reduction in overall industry revenue.8

Investor Implications: SMID indexes may provide more upside potential when the market stabilizes.

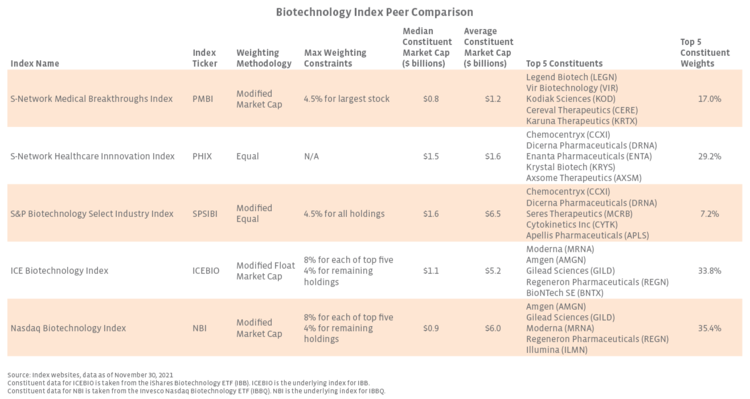

When discussing the biotechnology sector, it is important to differentiate between small to mid-cap biotechnology indexes and larger biotechnology indexes which are typically broader and own more pharmaceutical constituents. Smaller capitalization indexes like the S-Network Medical Breakthroughs Index (PMBI) and the S-Network Healthcare Innovation Index (PHIX) are heavily weighted towards biotechnology companies with multiple drugs in Phase II and Phase III FDA trials. These are generally more sensitive to FDA and regulatory news. In contrast, larger biotechnology indexes like the ICE Biotechnology Index (ICEBIO) and Nasdaq Biotechnology Index (NBI) have exposure to larger capitalization pharmaceutical companies like Moderna (MRNA), BioNTech (BNTX), and Regeneron Pharmaceuticals (REGN) which were involved with releasing the COVID-19 vaccines/antibody cocktail.

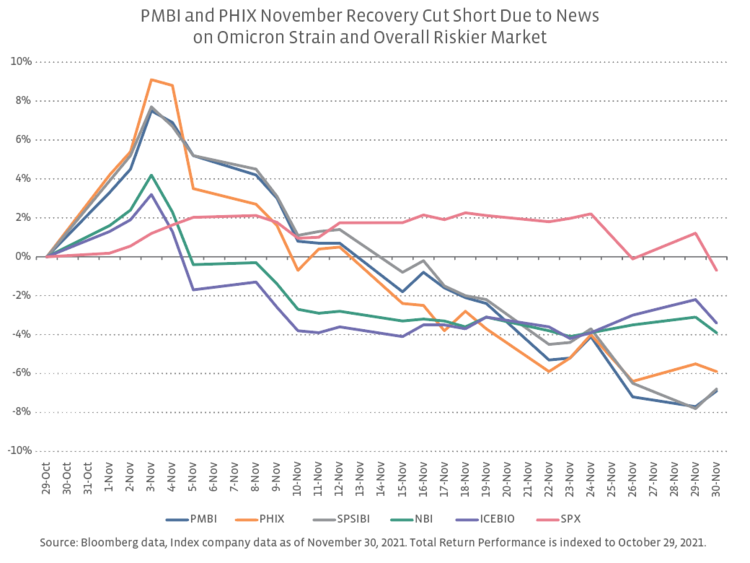

In early 2020, performance of smaller capitalization indexes like PMBI and PHIX was relatively in line with their larger cap peer indexes. But toward the end of 2020, the larger cap biotechnology indexes started outperforming due to the success of “vaccine stocks,” which contributed significantly to the index performance (especially given that both ICEBIO and NBI are market-cap weighted). Then in the early part of 2021, performance further diverged as volatility in the sector increased due to fears of increased regulation of both M&A and drug prices, in addition to uncertainty and investor frustration with the FDA—all of which weigh more heavily on small-cap biotechnology stocks whose stock prices depend on drug approval with the FDA and takeover premiums from M&A activity.

In early November, PHIX and PMBI saw a small rebound likely supported by recent positive developments, which reversed when risk once again increased on news of the COVID-19 Omicron strain. Although SMID biotech companies are more sensitive to riskier markets, risk/reward goes both ways. When the market eventually stabilizes, SMID equities could outperform large-cap peers. Additionally, SMID biotechnology indexes could show the potential for a higher rebound in the coming months given easier year-over-year comps relative to their large cap-index peers.

Bottom Line:

As the aforementioned November developments suggest some relief from this year’s largest headwinds, small and mid-capitalization biotechnology companies could benefit from a recovery considering their higher growth potential in a stabilized market, in addition to benefiting from easier comps in 2021 relative than their larger cap counterparts. For investors who can tolerate higher risk in exchange for higher return potential, the small to mid-cap biotechnology space may prove interesting in the coming months as the initial shock of regulatory fears is quelled and FDA processes are normalized under a new commissioner.

The S-Network Medical Breakthroughs Index (PMBI) is the underlying index for the ALPS Medical Breakthroughs ETF (SBIO).

The S-Network Healthcare Innovation Index (PHIX) is the starting universe for the SmartTrust Healthcare Innovations Trust, which selects 30 stocks from PHIX for inclusion in the portfolio. Series 12 of the UIT deposited on November 2, 2021. PHIX is also available on the C8 and the SMArtX platforms.

Related Research:

Investing in Biotechnology: Disrupting the Healthcare Space

Biotechnology: Capturing Innovation and Potential M&A Upside

A Differentiated Approach to Disruptive Technology

Four Megatrends Elevating the Commercial Space Industry

Crypto Mining for Digital Gold is Turning Green

1 Performance data from February 9 to November 30, 2021

2 U.S. approval of Biogen Alzheimer’s drug – Reuters

3 Press release – Acadia Pharmaceuticals

4 FTC Announces Multilateral Working Group – Federal Trade Commission

5 Biotech M&A, while far from recent heights, is picking back up – BioPharma Dive; 2H21 data through November 22, 2021.

6 Merck Completes Acquisition of Acceleron Pharma Inc. – Business Wire

7 President Biden Calls on Congress to Lower Prescription Drug Prices – The White House

8 Drugmakers Gear Up for Price Restrictions in Biden’s Legislative Agenda – WSJ