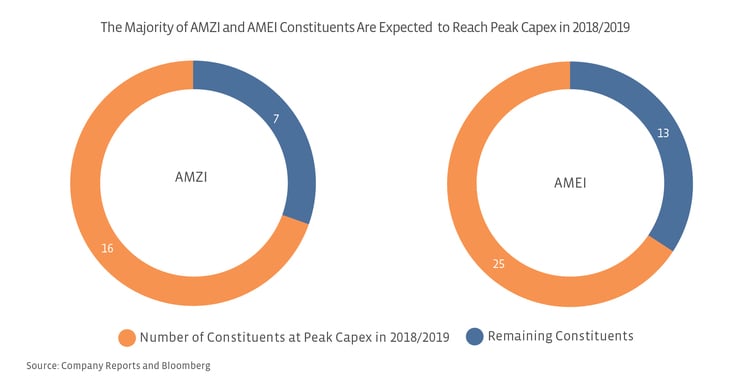

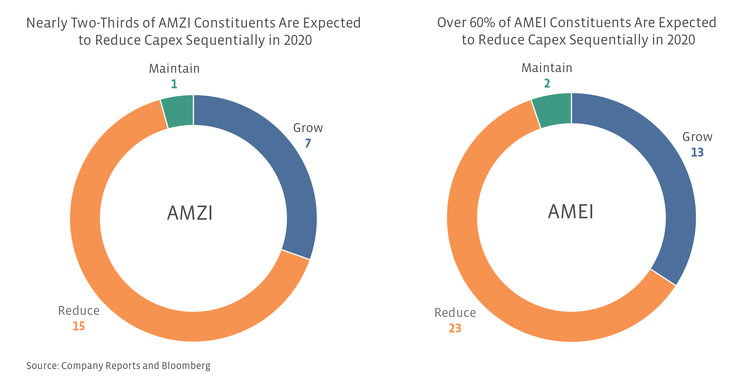

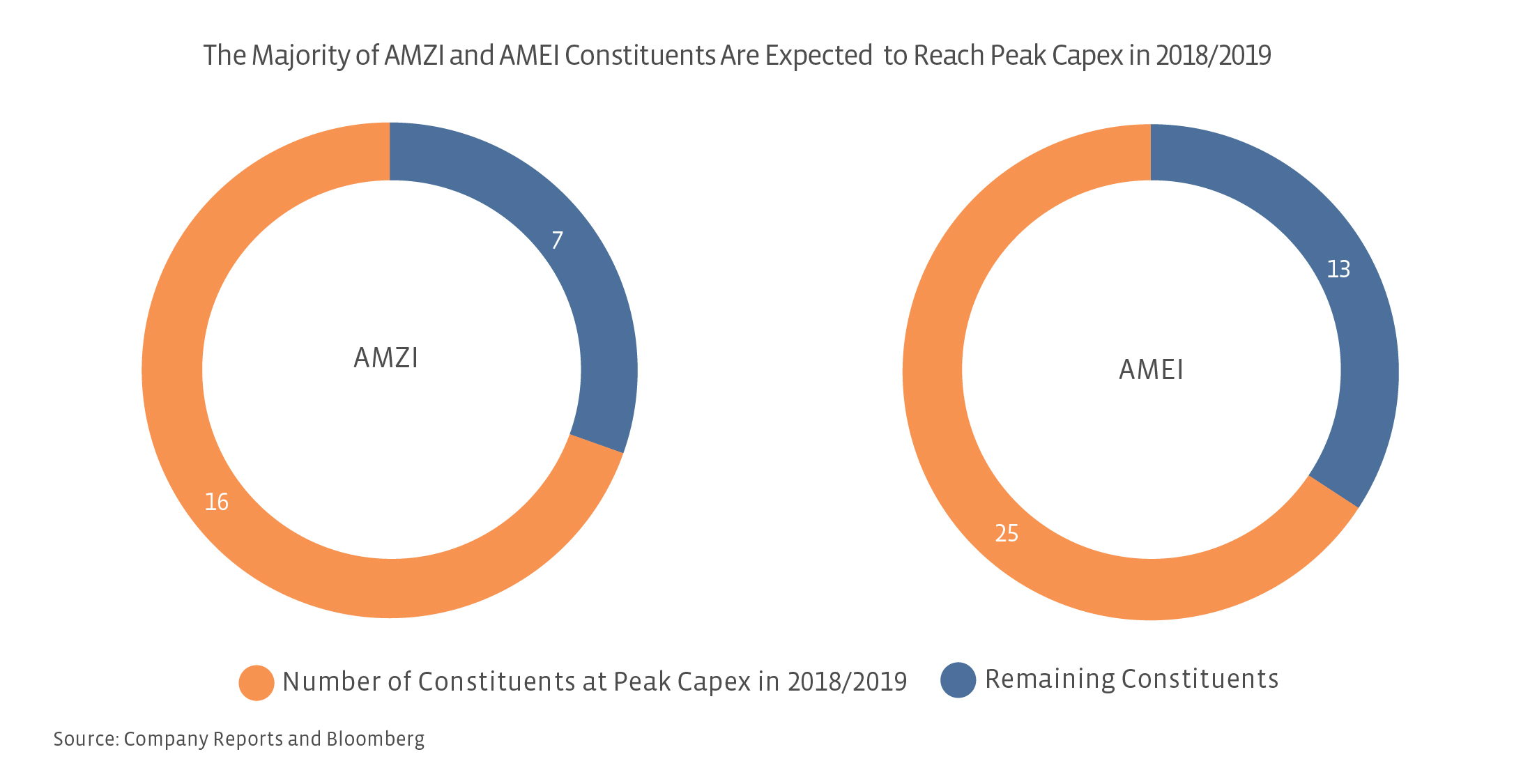

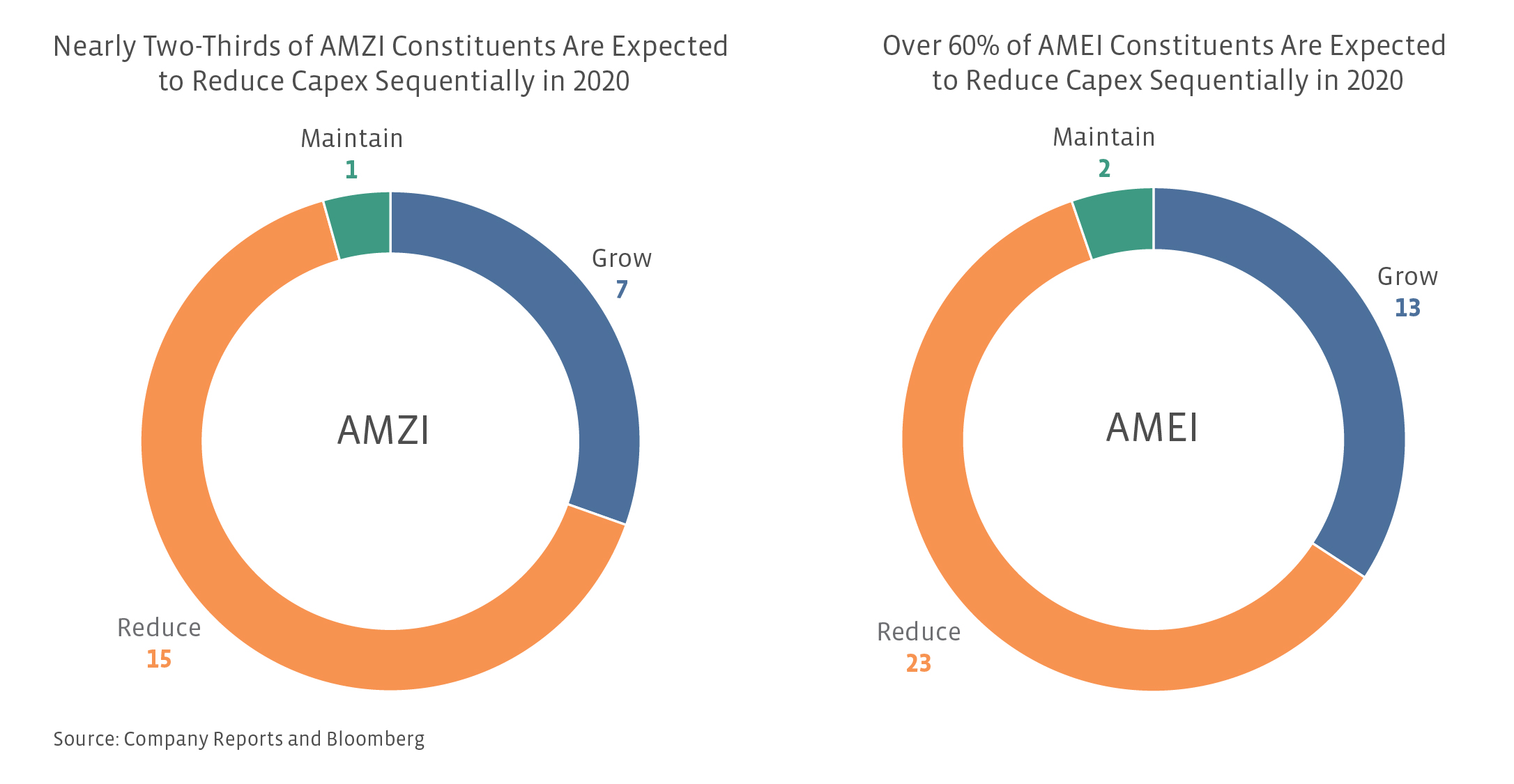

In the charts above, we primarily relied on Bloomberg estimates for 2020 growth capex because many companies have not provided 2020 guidance. The table below compares 2019 and 2020 guidance from midstream names that have given projections for both years, with many guiding to a decrease. As mentioned above, one reason for the moderation in spending is that companies are starting to complete some of the largest projects in their backlogs. For example, EQM Midstream (EQM) expects to complete the Mountain Valley Pipeline (MVP), a 2.0 Bcf/d natural gas pipeline on the East Coast, in 4Q19 at a total cost to EQM of $2.2 billion. EQM is estimating much lower capital expenditures in 2020 as a result, guiding to $800 million – a 61% decrease. With actual and estimated annual growth capex of $5 billion or more for 2016 to 2019, Energy Transfer’s (ET) median estimate for 2020 growth capex is only $3.1 billion. Magellan Midstream Partners (MMP) is currently guiding to $150 million in expansion capital spending in 2020, but management noted that number could increase if it spends some of its $500 million backlog in 2020. While 2020 numbers could certainly change, most companies are expecting a step down in spending.

| Company | Ticker | 2019 Guidance ($MM) | 2020 Guidance ($MM) |

| Andeavor Logistics – Press Release | ANDX | 600 | 600 |

| Antero Midstream –Presentation | AM | 710 | 600 |

| EQM Midstream – Press Release | EQM | 2050 | 800 |

| Magellan Midstream Partners – Press Release | MMP | 1100 | 150 |

| MPLX – Presentation | MPLX | 2200 | 2000 |

Other companies have not provided specific 2020 guidance but expect a sequential decline in growth capex. For example, ONEOK (OKE) and Targa Resources (TRGP) are expected to spend less in 2020 as major projects come online this year, with OKE management saying it expects a significant decrease in 2020 spending. Similarly, Western Midstream (WES) said in its May investor presentation that it expects 2020 capex to decline. CNX Midstream (CNXM) expressed in its 1Q19 presentation that it expects its capital budget to “decline substantially” in 2020 and beyond.

Moderating capex is generally positive for midstream.

In contrast to other sectors of energy, investors have generally been more receptive to MLPs and midstream companies raising capital spending guidance for growth projects expected to generate attractive returns (read more). As a recent example, Enterprise Products Partners (EPD) raised its 2019 growth capex guidance by 9% to $3.6 billion at the midpoint in conjunction with its 1Q19 earnings release and ended the day up 1.6%. It bears noting that results exceeded expectations, which factored into performance as well.

While investors have been sympathetic to midstream capex increases, reaching a peak in midstream spending could be positive in two ways: 1) companies generate greater cash flow as major projects built in recent years are brought online (read more), and 2) lower growth capital spending frees up cash for other uses. Simply put, greater free cash flow provides greater financial flexibility, allowing companies to reduce leverage, increase distributions, or repurchase shares/units. Growing free cash flow would also likely be welcomed by generalist investors. Separately, reduced growth capex may help alleviate investor fears of midstream potentially overbuilding infrastructure. Regardless, we view improving and sustaining free cash flow generation through prudent spending as one of the ways midstream management teams can demonstrate to investors that they are serious about capital discipline and achieving attractive returns (read more).

Bottom Line

After several years of significant capital spending on growth projects to facilitate robust US production growth, midstream growth capex appears to be peaking. For many companies, a decline in spending in 2020 reflects the completion of major projects that will now contribute to cash flow generation. Increased cash flow accompanied by lower spending sets the stage for free cash flow growth, with the potential for excess cash to be used for reducing leverage, increasing distributions, or buying back units/shares. If 2018-2019 proves to mark the peak for midstream spending, the prospect of enhanced free cash flow generation should be viewed positively by investors.

{kind=link}

{kind=link}