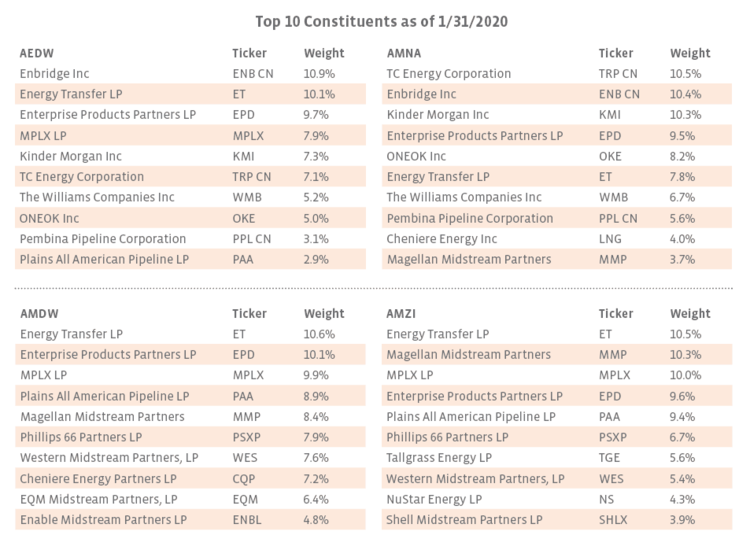

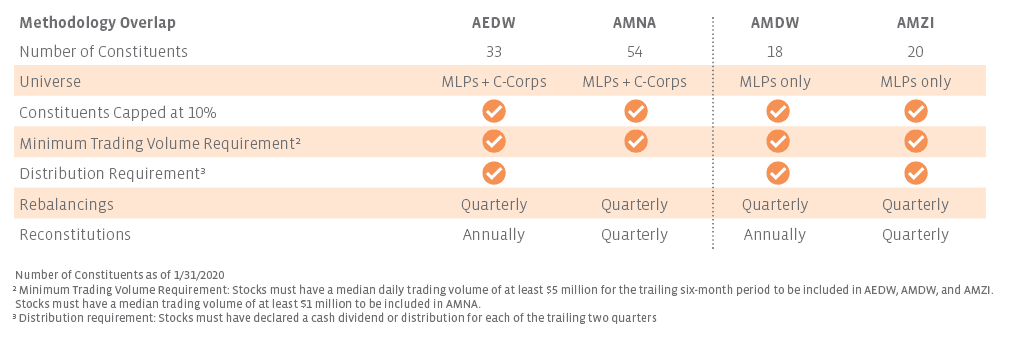

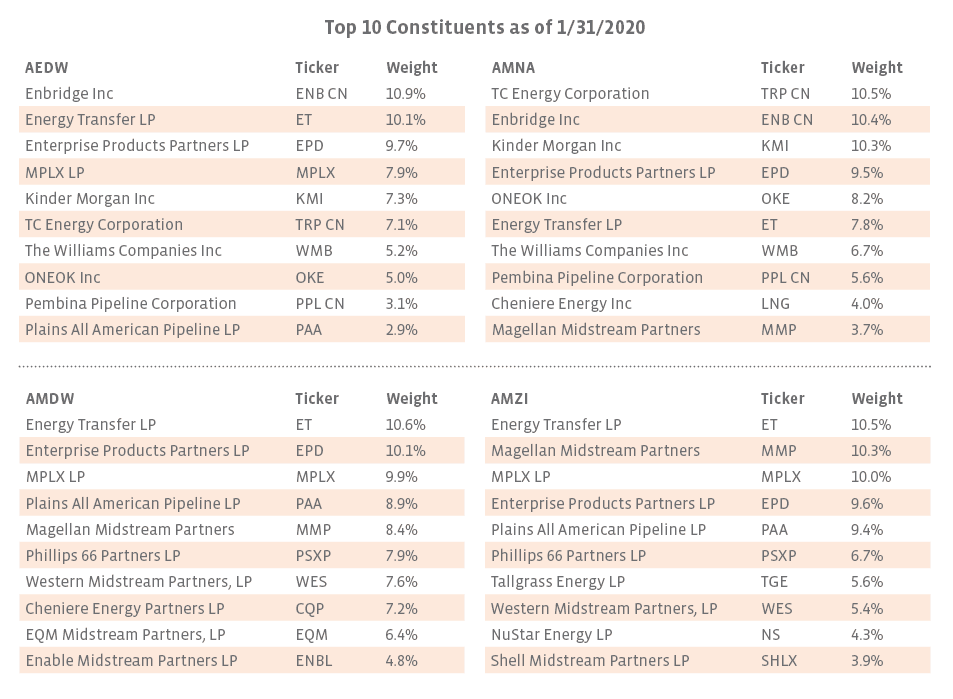

The dividend-weighted indexes outperform in the long-term despite overlap As reflected in the Methodology Overlap table above, AEDW/AMNA and AMDW/AMZI clearly have similar characteristics. As of January 31, 2020, AEDW and AMNA had an overlap of 77.4% by weighting. AMDW and AMZI had an overlap of 81.1%. This overlap is further evident in the comparison of top ten holdings below. Cheniere Energy (LNG), which currently does not pay a dividend, is the only top ten AMNA constituent not included in AEDW’s top ten, while AMDW and AMZI share seven top ten holdings.

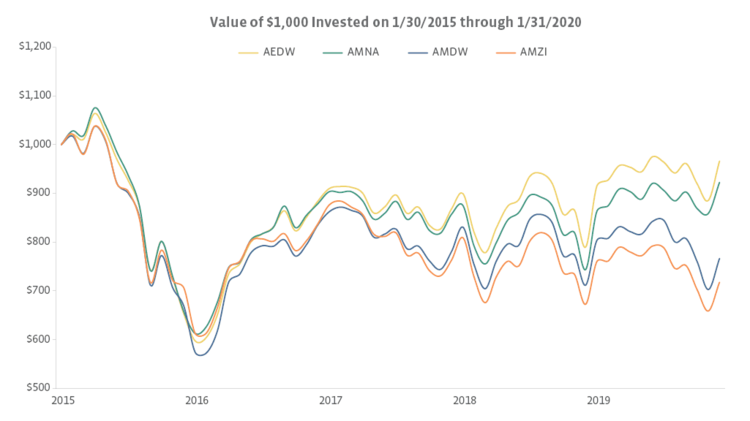

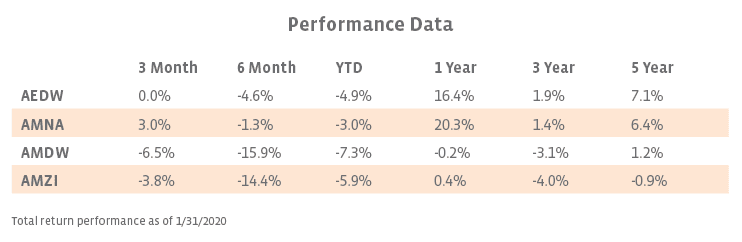

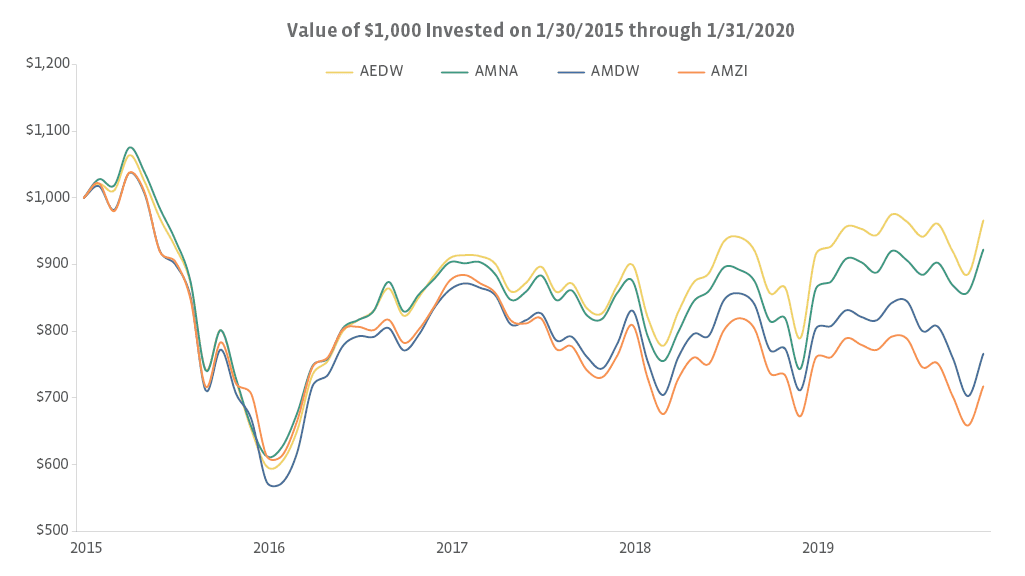

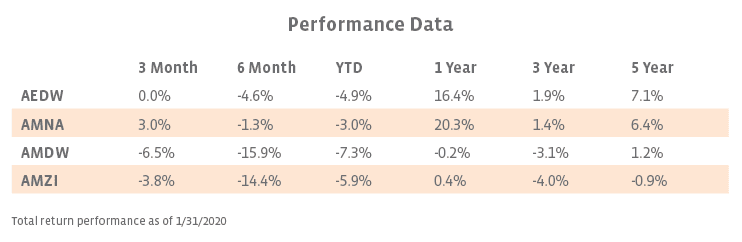

Given the significant overlap, one may expect similar performance between the fundamentally-weighted and market capitalization-weighted indexes. However, depending on the period, performance differences have been somewhat significant (see chart and table below). AEDW and AMDW have outperformed AMNA and AMZI, respectively, in the long-term. However, in the recent periods, AMZI and AMNA have performed better than their dividend-weighted counterparts. This performance difference alludes to the statistics that will be covered in the following section – among them, AEDW and AMDW have higher standard deviations, reflecting more volatility.

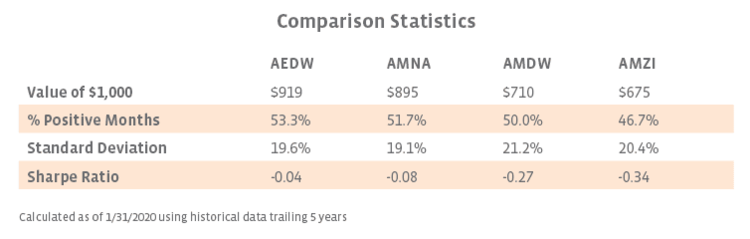

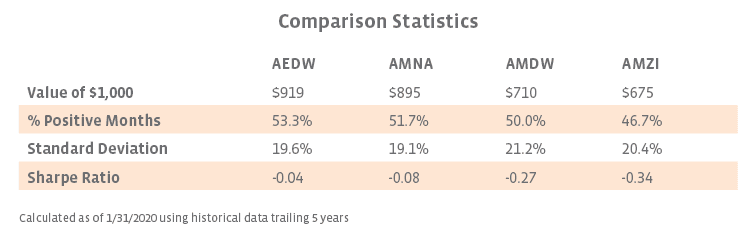

Dividend-weighted indexes have generated higher risk-adjusted returns To better evaluate the risk-return profile of AEDW and AMDW relative to AMNA and AMZI, it is informative to look at the metrics in the table below. Based on standard deviations alone, the dividend-weighted indexes suggest more risk than their capitalization-weighted peers. However, despite having a higher standard deviation, AEDW and AMDW generated higher risk-adjusted returns over the five-year analysis period as evidenced by their Sharpe ratios displayed in the table below. Even though AEDW’s standard deviation is 0.5% greater than AMNA’s, its Sharpe ratio is higher by 0.04. AMDW’s standard deviation is 0.8% higher than AMZI’s and its Sharpe ratio is 0.07 higher.

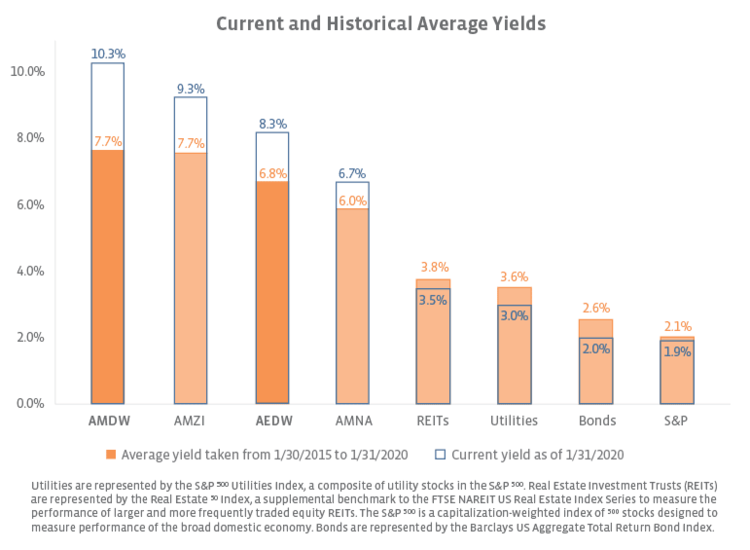

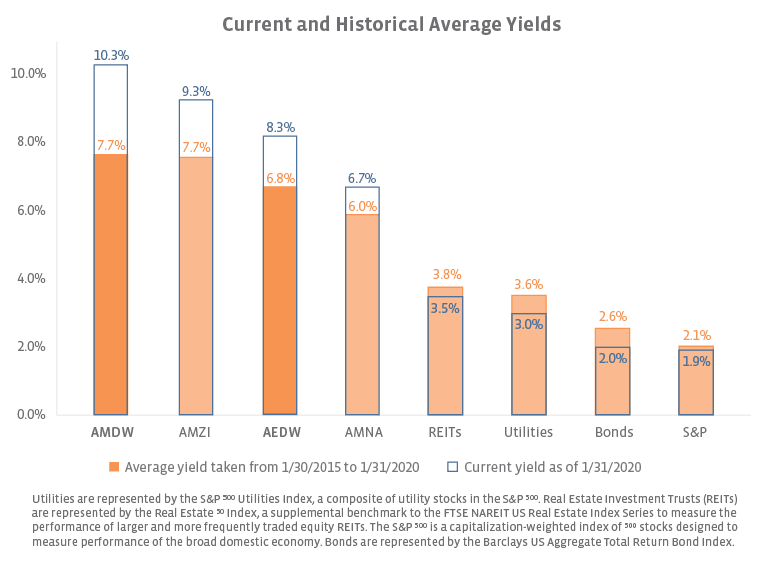

Dividend-weighted indexes screen attractively for yield Compared to their capitalization-weighted counterparts, the dividend-weighted strategies also screen more attractively in terms of yield as shown below. The midstream MLP space is known for its steady cash flows and tax-advantaged distributions, which may lend itself to an indexing strategy that emphasizes the total dividend payout of its constituents.

While these strategies emphasize dividends, it is important to not view yield in a vacuum. Large swings in equity prices can quickly inflate yields. Capitalization-weighted indexes rely on the theory that market capitalization is the best measure of a company’s value. As the price rises, so does the company’s weighting in a capitalization-weighted index. Weighting by total distribution (dividend multiplied by shares outstanding) does not take into account price; instead it deems a company’s ability to pay out distributions as more deterministic of its long-term value.

Bottom line The addition of AEDW and AMDW to the Alerian index suite provides stakeholders with new benchmarking tools and an index strategy based on dividends. Although they have historically carried slightly higher risk than their market capitalization-weighted counterparts, AEDW and AMDW have delivered higher long-term returns, higher long-term Sharpe ratios, and higher average yields.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}