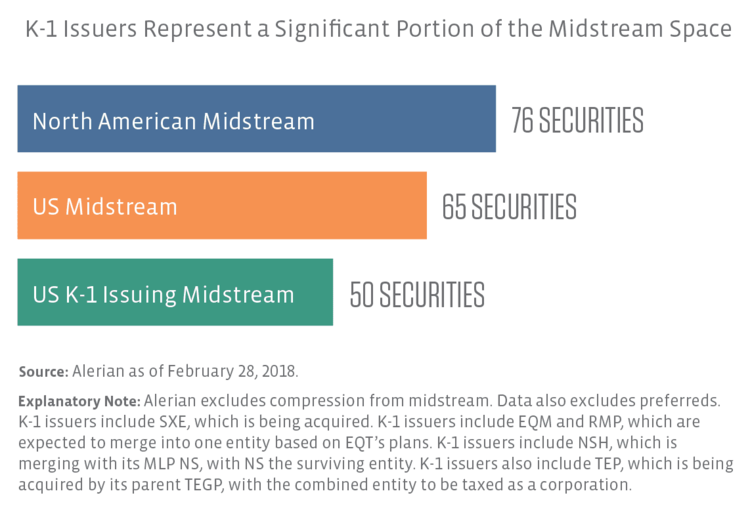

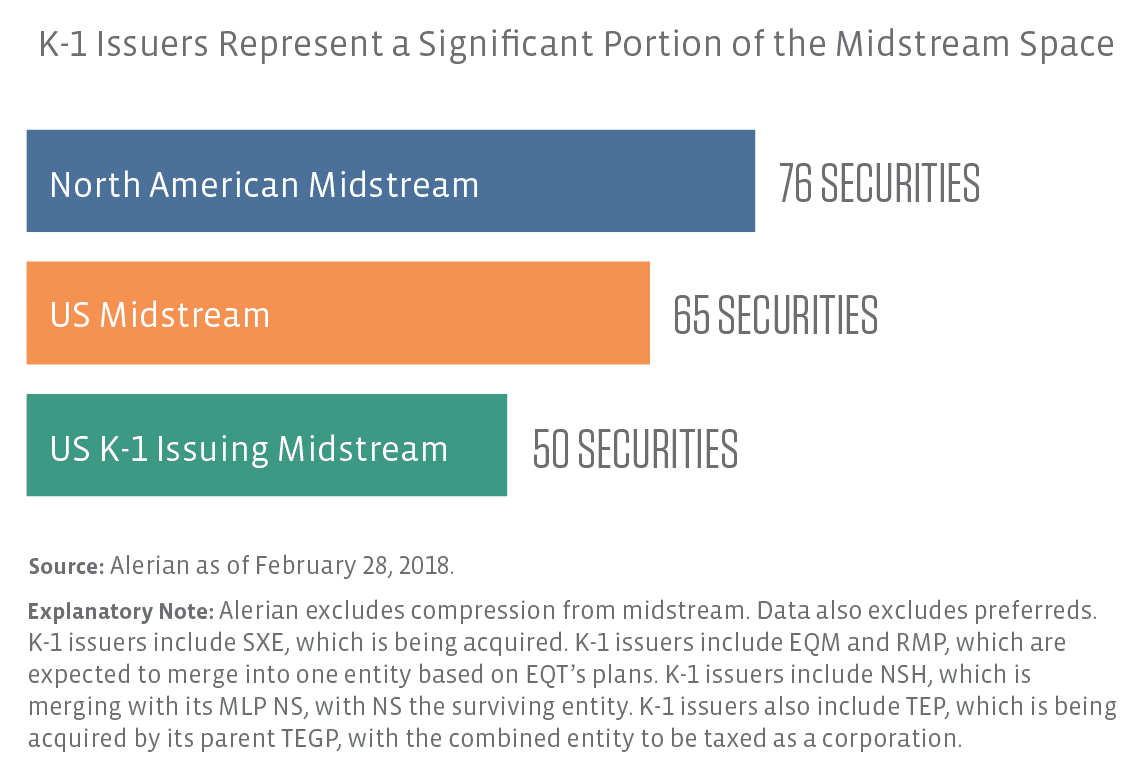

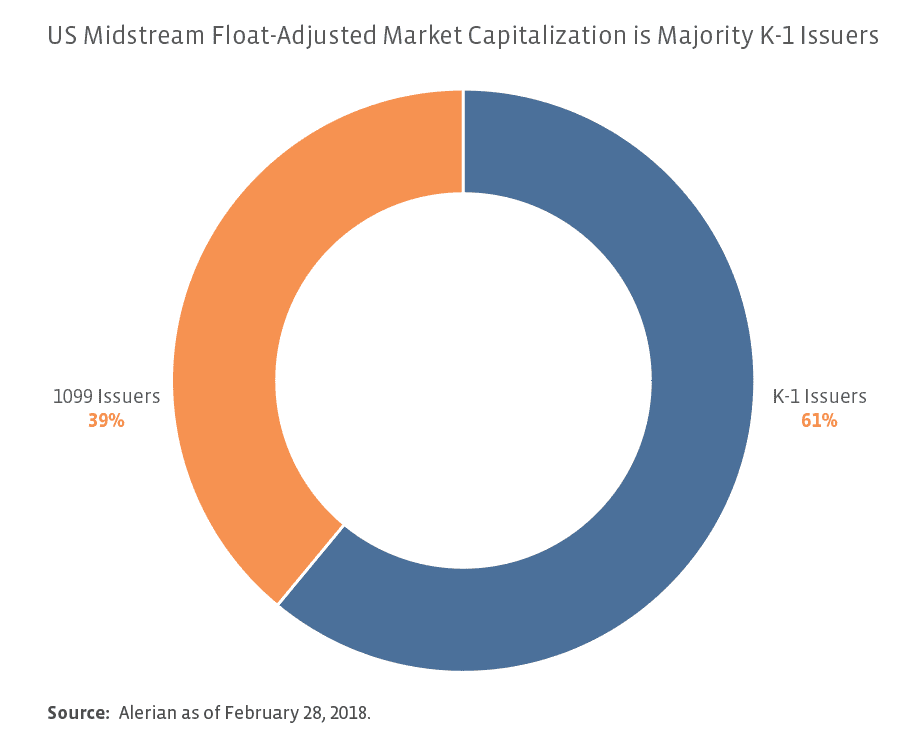

If you look at float-adjusted market capitalization as of the end of February, K-1 issuers represent 61% of the total US midstream float-adjusted market cap, with 1099 issuers representing the remaining 39%. Notably, just three corporations — Kinder Morgan (KMI), ONEOK (OKE) and Williams Companies (WMB) — constitute 26% of the total US midstream float-adjusted market capitalization.

What about those midstream companies that issue 1099s? Is the grass greener as a corporation?

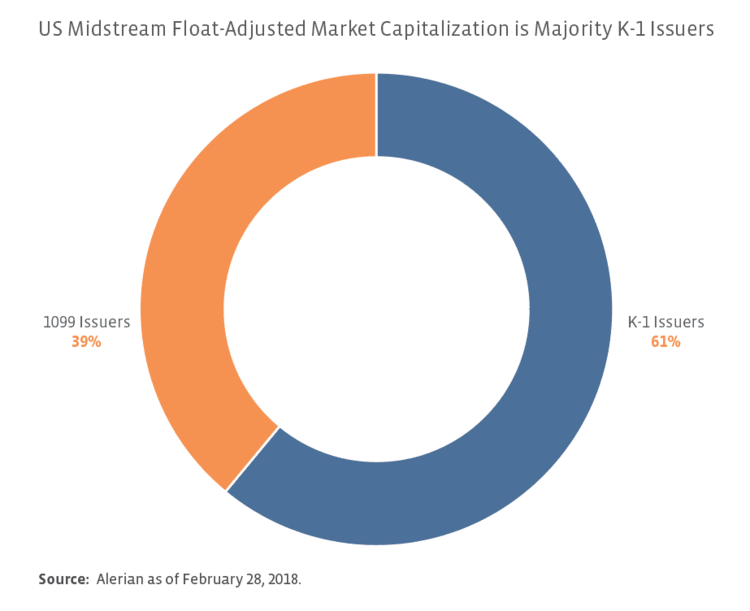

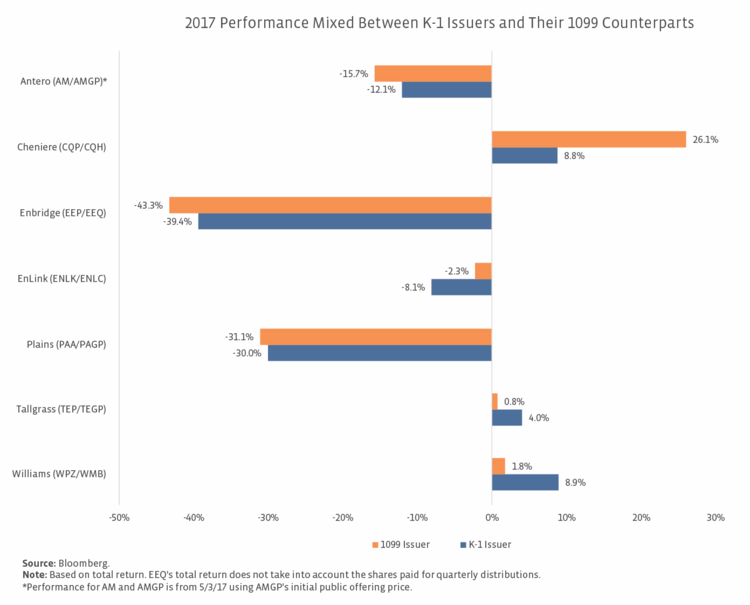

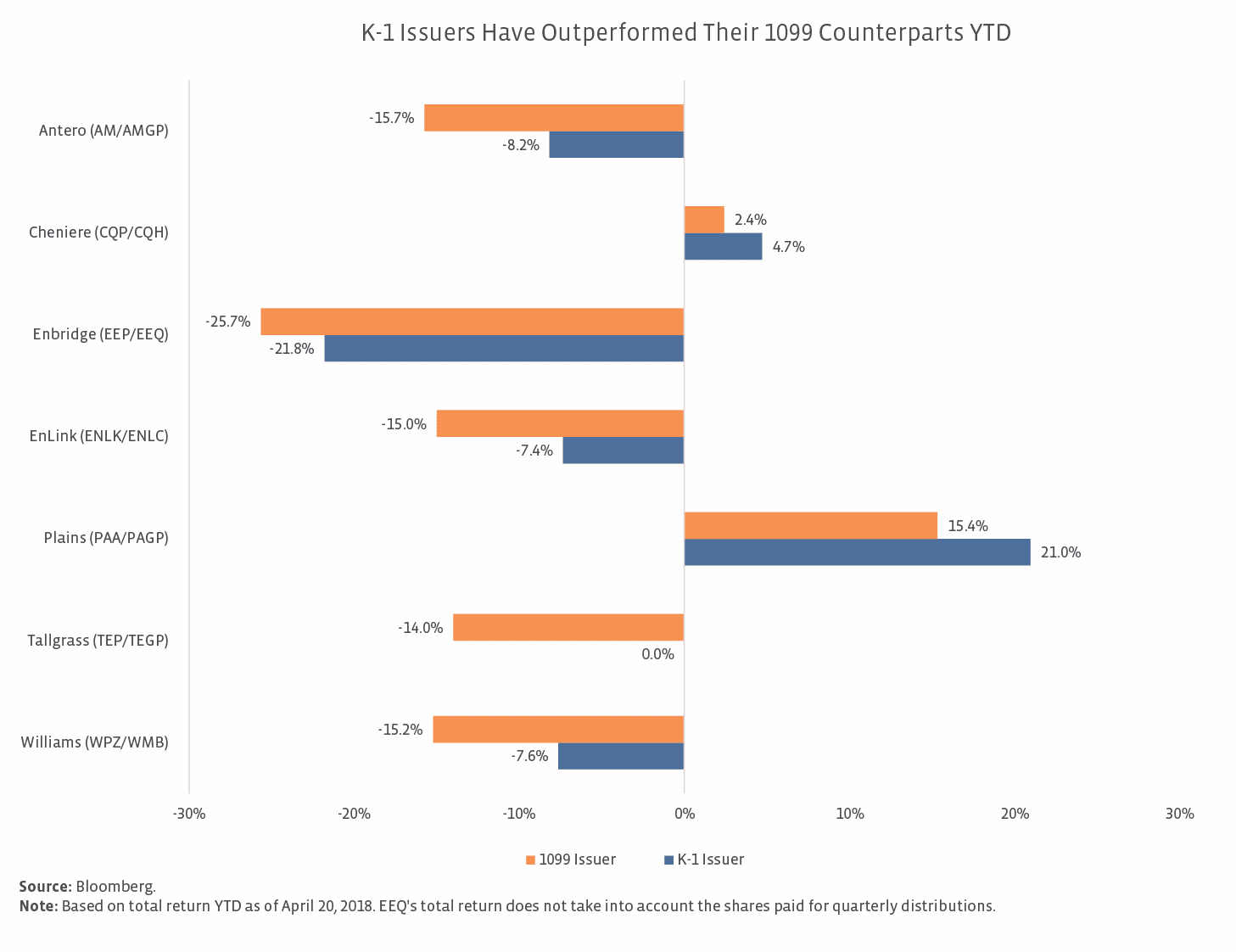

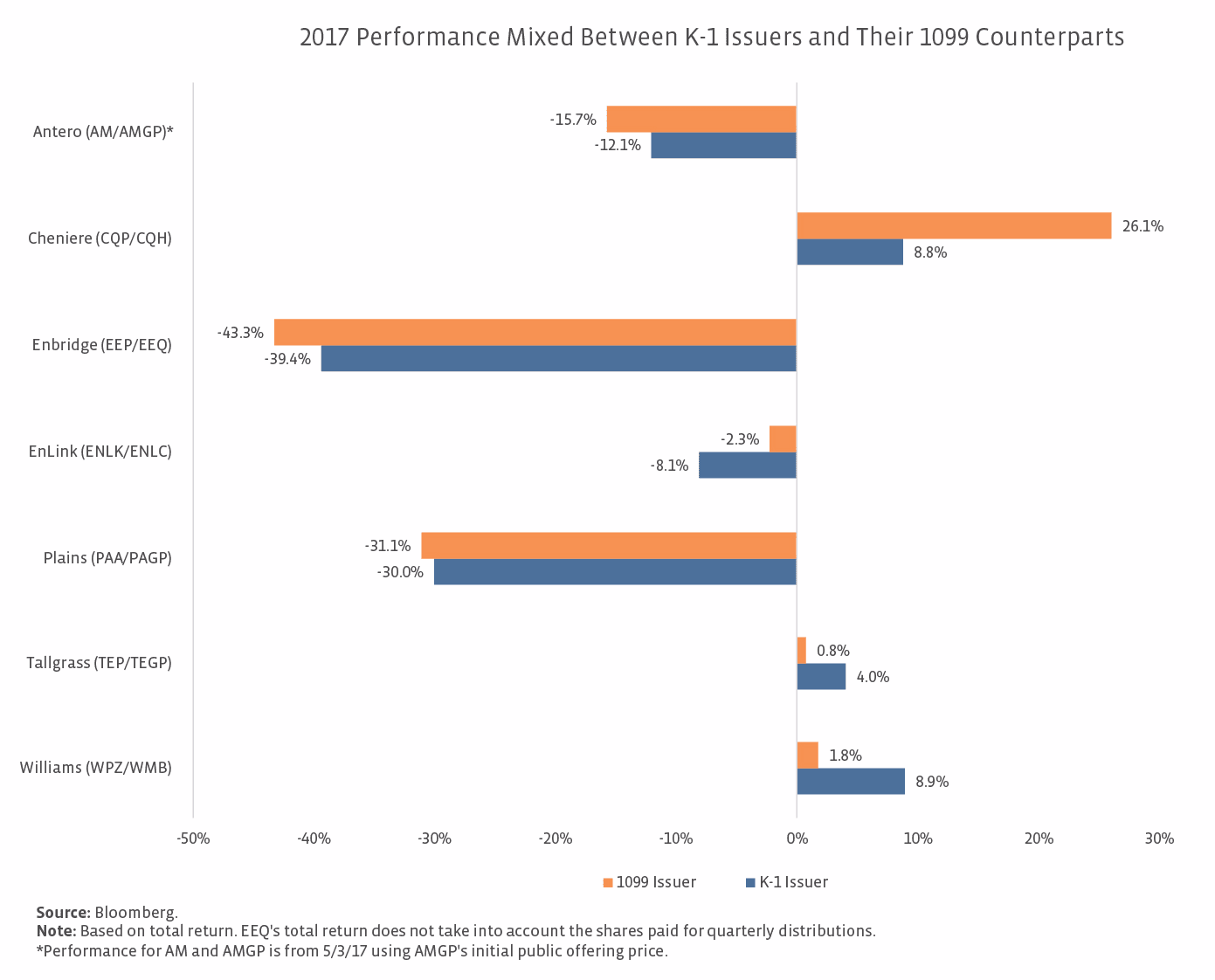

Let’s take a closer look at those 15 securities that are US midstream companies but are not K-1 issuers. Of those 15 securities, eight share an asset base with a K-1 issuer. This allows us to compare the yields and total return of the two related entities. For the Cheniere complex, we compare Cheniere Energy Partners LP Holdings (CQH) and Cheniere Energy Partners LP (CQP) below, though Cheniere Energy (LNG) is also affiliated. LNG does not pay a dividend. As you can see from the charts below, the K-1 issuers have outperformed their 1099-issuing counterparts year-to-date, which may be a surprise.

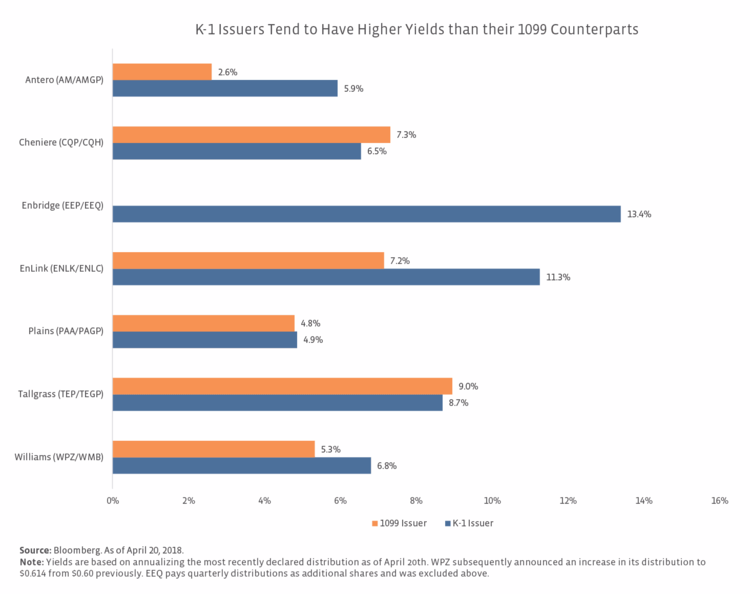

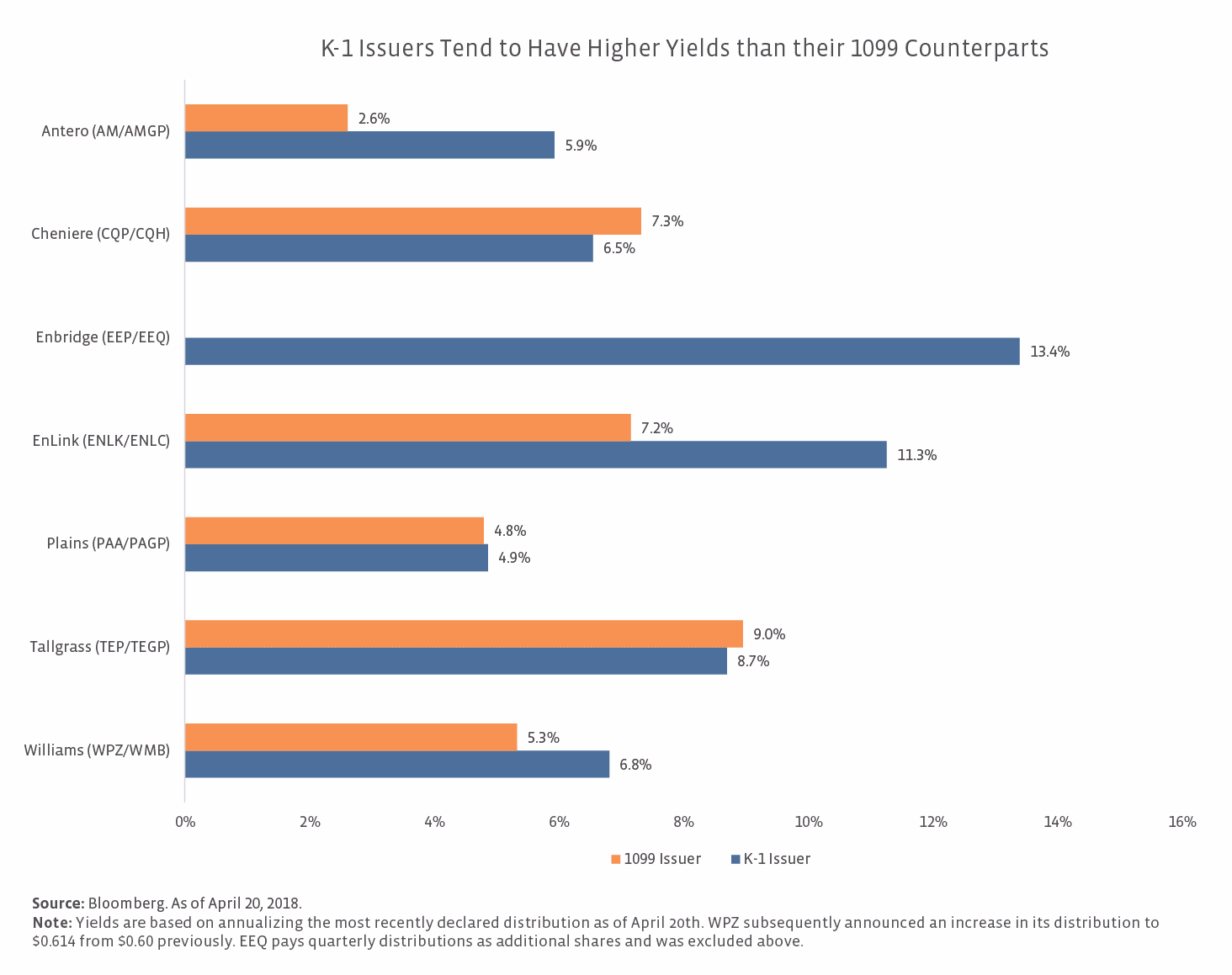

Typically, one would expect the K-1 issuer to have a higher yield given that it doesn’t pay tax at the entity level. Interestingly, in two of the seven pairings below, the 1099 issuer has a higher yield than its K-1 issuing counterpart. We chose to look at total return to even the playing field and because some of the 1099 issuers also have significant yields.

What about the seven other securities without a K-1 issuing affiliate? The seven include Tellurian (TELL) and NextDecade (NEXT), which are both focused on LNG export development and do not pay dividends, as well as Macquarie Infrastructure Corp. (MIC), Targa Resources (TRGP), SemGroup (SEMG), KMI and OKE. Setting aside TELL and NEXT, the average yield of the five remaining C-Corps was 7.2% (6.4% excluding MIC) as of April 20th. For context, the yield of the Alerian MLP Infrastructure Index (AMZI), which is a composite of energy infrastructure MLPs, was 8.2%. On a total-return basis, OKE and TRGP have outperformed the AMZI year-to-date through April 20th, while KMI, SEMG and MIC have underperformed. There seems to be an impression that the grass is greener for energy infrastructure corporations, but the data doesn’t fully support that sentiment.

“What’ll Ya Have?”

This is the greeting that meets you when you visit The Varsity — a fast food institution in downtown Atlanta. While Alerian can’t offer you delicious onion rings, we do want to help you get what you want as an energy infrastructure investor. We’re an indexing firm. We’re not in the business of giving investment advice. Our goal is to help investors make informed decisions when investing in MLPs or energy infrastructure. As such, we aren’t trying to say C Corporations are bad or that MLPs are good or vice versa. Instead, we want to point out the trade-offs that you should consider before investing in an individual midstream MLP, an energy infrastructure corporation, or an access product.

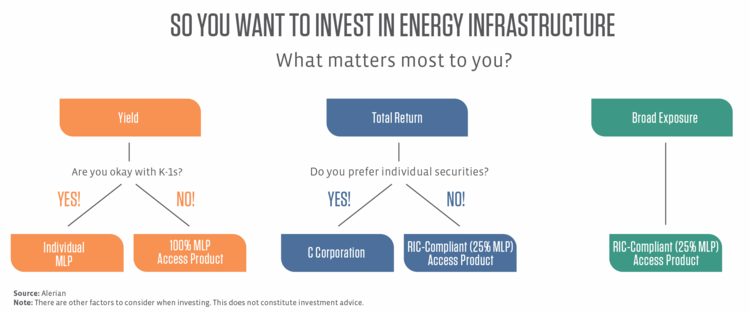

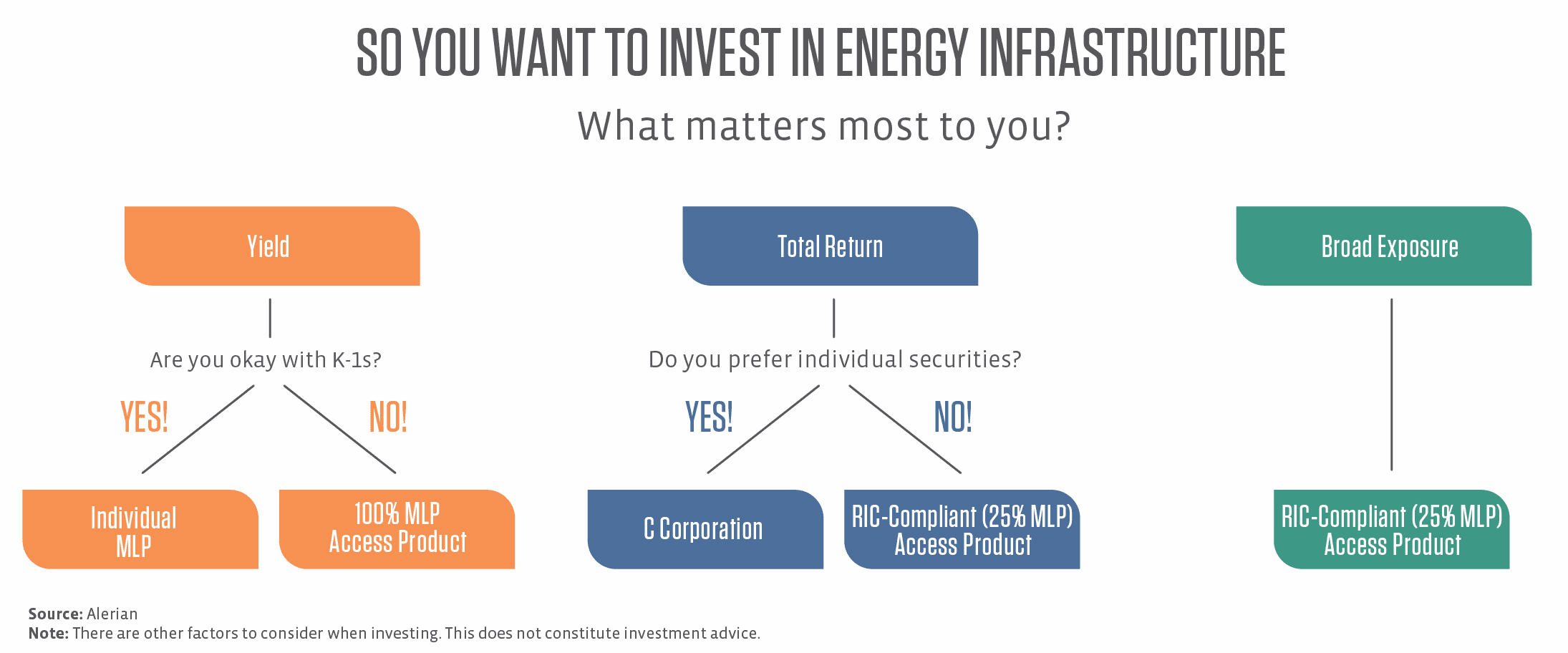

While there are lots of pros and cons to consider, we have a very simplified decision tree for investment in energy infrastructure in the infographic below. If you are mainly concerned with yield (income), then you may have more of a preference for MLPs, whether that’s investing in an individual MLP or accessing the space through an access product like an exchange traded fund (ETF), closed-end fund (CEF) or exchange traded note (ETN). If you invest in a product that is 100% MLPs, the benefits are yield and tax-deferred return of capital, but in general, you are not getting full exposure to the midstream universe, given the significance of C Corporations, such as KMI, OKE and WMB.

If you are more focused on total return and want to own a single security, and don’t want a K-1, a C Corporation may be more appealing to you. Otherwise, you may prefer to own a RIC-compliant access product that owns both MLPs and C Corporations (for an explanation of RIC-compliant funds, see the Applied MLPs section of MLP University). With MLPs capped at 25% for RIC compliance, you’ll be giving up yield and a smaller portion of the income will be considered a tax-deferred return of capital. However, you’ll be gaining broader exposure to the energy infrastructure universe. You’ll also want to be aware of what makes up the other 75% of the fund, whether it’s energy infrastructure corporations, Canadian energy infrastructure companies, utilities, oil and gas producers or even energy consumers.

Bottom Line:

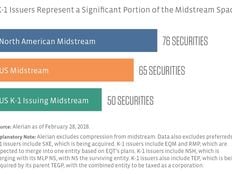

It may not feel like it, but K-1 issuers continue to represent a significant portion of the US midstream space. Yes, we will probably continue to see restructurings and some conversions to C Corporations, particularly for MLPs with incentive distribution rights in the higher split levels. That said, it’s a little premature to make the call that the MLP structure is going to be abandoned in favor of the C-Corp structure. As the midstream space evolves, investors may need to be more discerning in terms of how they gain exposure to energy infrastructure. Fortunately, with a variety of access products complementing options to invest in C Corporations or MLPs directly, investors can tailor their exposure to meet their needs.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}