Summary

- ESG reporting has continued to gain traction in midstream with six more companies publishing their inaugural sustainability reports in the last ten months.

- Recent sustainability reports show that energy infrastructure has made notable improvements in ESG reporting and performance.

- Going forward, midstream companies should continue to adopt comprehensive and transparent sustainability reporting and strive to improve their safety, emissions, and governance metrics.

One of the most popular trends in investing over the last few years has been the rise of environmental, social, and governance (ESG) investment considerations. Energy infrastructure may not be the first sector that comes to mind when thinking of ESG-friendly investments, but adoption of sustainability reporting is becoming more commonplace among midstream companies. Although midstream certainly still has a way to go in its efforts to cater to ESG considerations, there have been notable improvements in the last year alone. Today’s piece serves to update our October 2019 white paper, First Steps: Introducing ESG Issues in Midstream, by examining developments in sustainability reporting and performance in the space, as well as a discussion of next steps for the industry.

ESG reporting continues to gain traction in midstream.

Even against the backdrop of a challenging and noisy macro environment for energy this year, ESG has remained in focus for investors and midstream management teams alike. Since the October 2019 ESG white paper, six more energy infrastructure companies have published their inaugural sustainability reports, bringing the total across the industry to fifteen. This excludes companies such as Phillips 66 Partners (PSXP) and Hess Midstream (HESM) whose parent companies publish ESG data for their midstream subsidiary. Overall, Canadian corporations tend to be leading the way in terms of ESG reporting in midstream with the large US C-Corps also providing sustainability reports. MLPs as a group are lagging, though some individual MLPs have provided sustainability reports and integrated ESG into broader investor materials. As an example, a recent presentation from Enterprise Products Partners (EPD) included a dedicated sustainability section that highlighted the role US energy will play in improving quality of life around the world. A handful of companies have also updated their sustainability reports in the last year to include additional data or a more comprehensive discussion of their operations, demonstrating the industry’s ongoing commitment to ESG reporting.

With sustainability and ESG considerations increasingly on the minds of investors, ESG should similarly be a focus for midstream management teams trying to attract new investors to the space. The momentum around ESG-minded investing continues to grow, especially among younger investors, and midstream should be responsive to this trend. A survey conducted by Brown Brothers Harriman found that roughly 74% of global investors intend to increase their exposure to ESG exchange-traded products in 2020. For midstream, ESG reporting is likely a prerequisite for attracting generalist investors with ESG sensitivities. Additionally, ESG adoption could benefit midstream as greater public scrutiny is placed on energy infrastructure projects. Pipelines tend to receive criticism from environmental groups, but in reality, they are the safest method of oil and natural gas transportation. Transparent data around worker safety, pipeline spills, and emissions may help reassure stakeholders that companies operate in a safe and effective manner.

Midstream shows improvement in key ESG metrics and increases transparency.

In our initial analysis of ESG in midstream, we noted that the first steps for energy infrastructure companies would be to engage with investors, increase disclosures, and promote uniformity and transparency in those disclosures. Based on recently published sustainability reports, it seems that the space is in the process of taking these steps. The increase in reporting has made it easier for investors to compare the ESG performance of individual companies and gauge an operator’s standing among the industry. While there is still some variability in the metrics disclosed, most sustainability reports tend to include common key data points. The widespread adoption of a reporting framework, such as those offered by the Global Reporting Initiative (GRI) or Sustainability Accounting Standards Board (SASB), could help further improve uniformity across the industry. Many midstream companies already utilize one or both of these frameworks in sustainability reporting.

Recent sustainability reports also show improvement in key metrics in recent years, particularly in regard to safety. Given the nature of the midstream business, sustainability reports often place a strong emphasis on safe operations, which has only been amplified by the ongoing pandemic. A key example of this is Crestwood Equity Partners (CEQP), which ties 20% of company compensation to five safety metrics, such as Total Recordable Incident Rate (TRIR). TRIR, which is a measure of work-related injuries or illnesses, or a similar metric is included in each midstream sustainability report. For the 15 midstream companies with sustainability reports, TRIR fell by 14.9% on average on a year-over-year basis as of the most recent reporting period. Several companies even provide TRIR goals. Gibson Energy (GEI) and ONEOK (OKE), after seeing declines in their injury rates in 2019, have stated targets for further reducing TRIR in 2020.

Greenhouse gas emissions are another key component of sustainability reporting and will likely be a primary consideration for ESG-focused investors going forward. While emissions metrics continue to vary from company to company, each midstream sustainability report provided some data detailing the company’s environmental impact. The majority of reports even mention the threat that climate change poses to both the environment and their businesses, with Enbridge (ENB), TRP, and Williams (WMB) each including more extensive sections on climate change in their reports. One of the most helpful measures included in the majority of sustainability reports is emissions intensity, which shows a company’s greenhouse gas emissions relative to another metric, such as EBITDA, barrels of oil equivalent handled, or gross margin. Relative to total greenhouse gas emissions, emissions intensity helps to contextualize size, growth, M&A, or other factors that could make a year-over-year or company-to-company comparison difficult. It also bears mentioning that intensity targets will vary depending on a midstream company’s primary operations. A storage company will generally be less emissions-intensive than operators involved in natural gas processing or fractionating natural gas liquids. While energy infrastructure is already a lower emissions business than other sectors of traditional energy, ongoing investment in renewables by some midstream companies will further benefit their emission profiles going forward (read more).

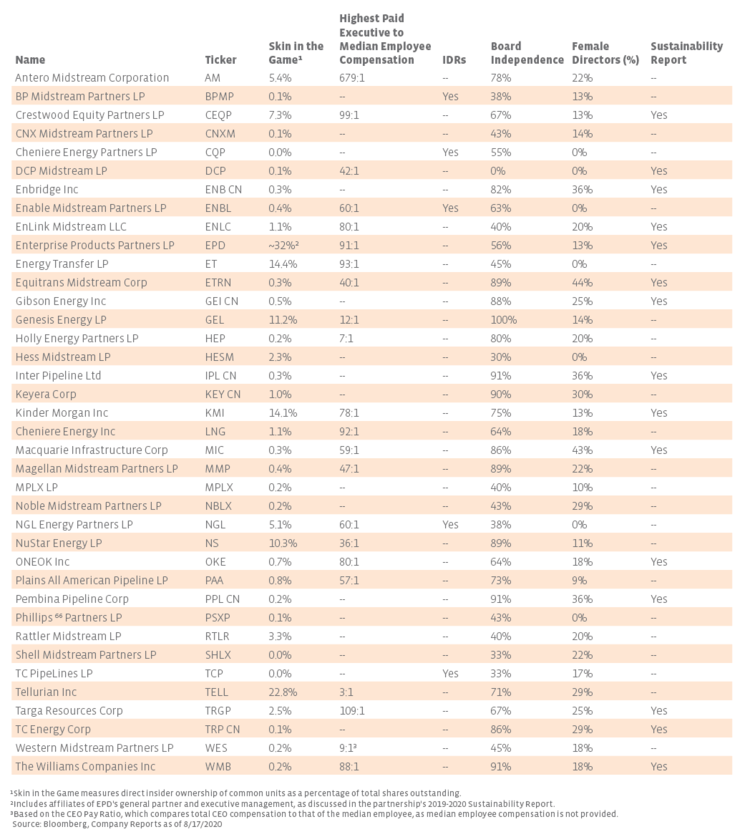

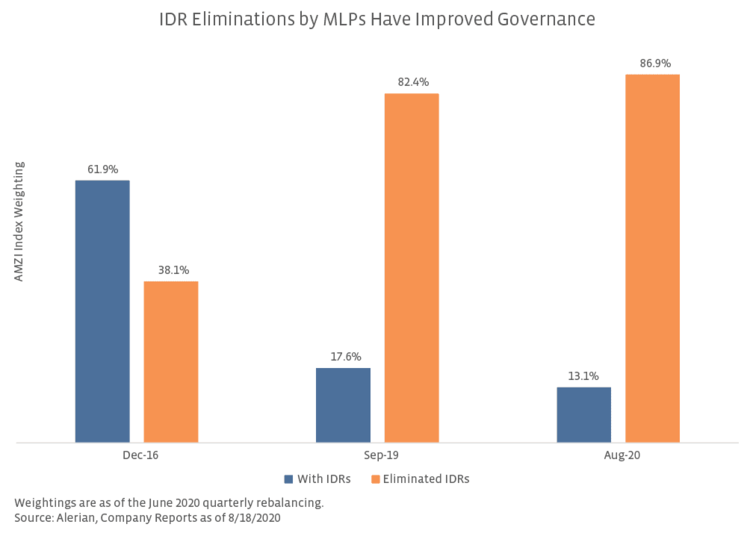

Governance factors are a major component of the ESG discussion for midstream. The table below provides an update on the governance metrics for the top 30 constituents of the Alerian Midstream Energy Index (AMNA) from the October ESG white paper, expanding the data set to include all of the current constituents of the Alerian Midstream Energy Select Index (AMEI). In terms of board independence, 24 of 38 companies analyzed have a majority independent board. No company has a board that is majority female, and seven companies do not have a female board member at all. While board dynamics have not changed much in less than a year, insider ownership can change quickly, and management teams’ skin in the game has broadly increased since our white paper was published. Many of the names listed below, namely CEQP and Genesis Energy (GEL), have seen skin in the game tick up since October as midstream insiders took advantage of the sell-off in 1Q20 to purchase significant amounts of their company’s shares on the open market, better aligning their financial interests with those of their shareholders (read more).

{kind=link}

{kind=link}