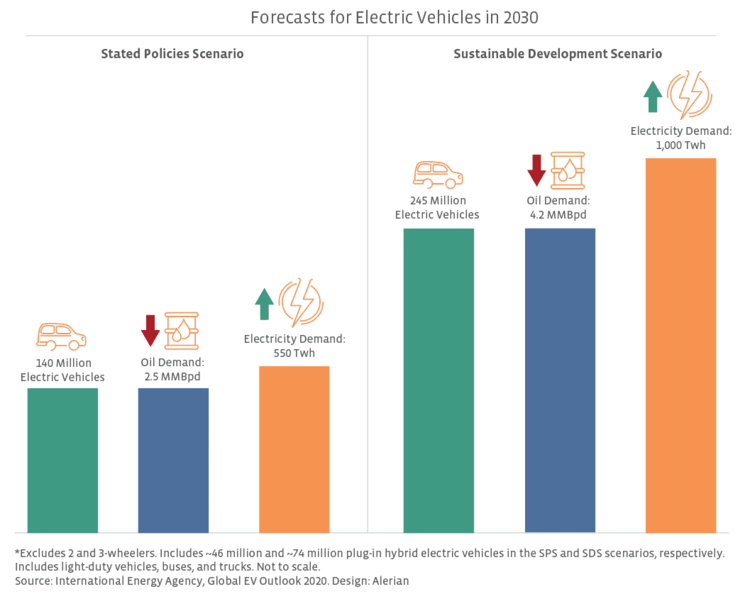

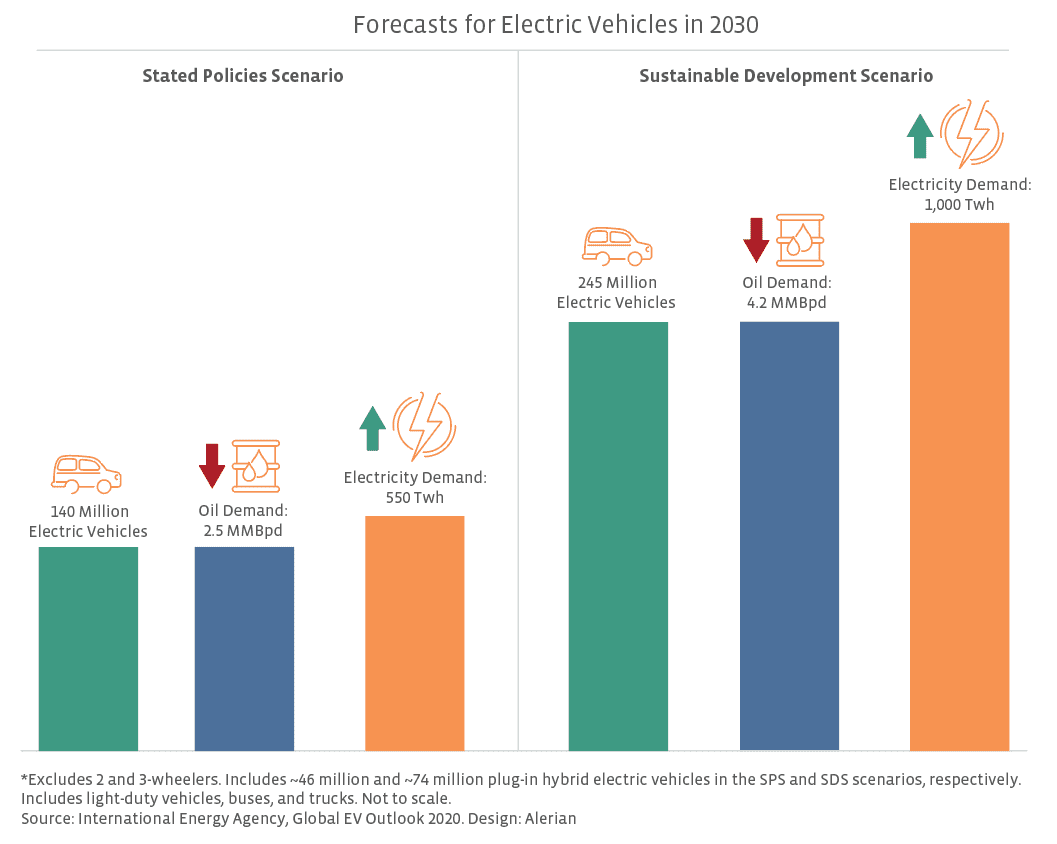

The two scenarios may be considered bookends of a range of possible outcomes. However, there is an element of execution risk in both scenarios, and clearly much could happen to change the global outlook in either direction. For example, the results of the upcoming US election could have implications for the rate of EV adoption in the US given Vice President Biden’s plan to invest in 500,000 charging stations and bring back the EV tax credit. Trends in China and India also bear watching. If the SDS forecast materializes, the impact to oil demand of 4.2 million barrels per day (MMBpd) in 2030 seems manageable. Keep in mind that oil demand in 2Q20 was down 16.4 MMBpd year-over-year due to the impact of COVID-19 and is expected to be down 7.9 MMBpd for the year. The 2030 threat of EVs seems modest by comparison, and the impact will be gradual, unlike the demand shock in 2020. For the next five years, the impact of EVs on oil demand is likely to be relatively insignificant. Of course, EVs will increase electricity demand as also shown in the chart, which has implications for power demand and the grid.

What challenges remain for greater EV adoption?

The often-cited knocks on EVs are range concerns, lack of charging infrastructure, and their costs. Governments are stepping in to help with the last two issues. In its historic stimulus package, the European Union was targeting two million electric and hydrogen vehicle charging points and had earmarked 20 billion euros to encourage sales of cleaner autos. France and Germany have recently announced increased subsidies for EVs. Meanwhile, China extended incentives for EVs through 2022, including tax exemptions for purchases of new EVs, and also committed to significant investment in charging infrastructure. Subsidies have proven effective in the past when it comes to supporting EV sales and may prove useful again, especially as the higher up-front cost of EVs may be less palatable when gasoline prices are relatively cheap.

While government policy can help alleviate some of the challenges facing EV adoption, other issues may prove more difficult. Clearly, there is an onus on auto manufacturers to roll out new electric models at reasonable costs, but there is some element of execution risk. For example, Volkswagen has delayed the rollout of its ID.3 electric model due to software challenges. A secure supply of minerals produced in an environmentally conscious manner can be another obstacle, with an EV having five times the mineral requirements of a traditional car. For example, TSLA has been looking for a source for sustainable nickel. BloombergNEF estimates that a nickel shortage could emerge as soon as 2023. The challenges around lithium and cobalt have been well documented, but other issues like the recycling of EV batteries are concerns as well. The burden to the grid and incremental electricity needs are also issues to be addressed. Vehicle-to-grid technology (EV batteries provide power to the grid) could help alleviate this burden during peak demand, but technological improvements and policy support are needed for these solutions to be realized. With the widescale rollout of a new technology, there are bound to be challenges, and these are a few examples.

What is expected to drive future oil demand?

Many people associate oil demand with cars because that is often their firsthand experience with oil consumption, but the reality is that passenger vehicles are not expected to drive the growth in long-term oil demand. Perhaps growth could come from some developing countries as an emerging middle class bought vehicles, but the primary drivers of demand are expected to be petrochemicals, trucking, shipping, and airplanes. In its World Energy Outlook from 2019, the IEA forecast that oil demand from passenger vehicles would top out in the late 2020s, but the agency did not expect overall oil demand to peak before 2040 under the Stated Policies Scenario. One caveat to the late 2020 peak for passenger vehicle demand is the assumption that sports utility vehicles (SUVs) would moderate in popularity. If consumers continue to prefer SUVs, the result would be an incremental 2 MMBpd in 2040 oil demand, which would likely offset a good portion of EV-related demand destruction.

Setting aside transportation, petrochemicals are expected to be a significant driver of petroleum demand going forward driven by increased demand for plastics. Emerging middle classes in developing countries will likely want the same plastics that we take for granted but that add significant convenience to our daily lives. Even in the IEA’s Sustainable Development Scenario in the 2019 World Energy Outlook, petrochemicals would spur an incremental 3 MMBpd in oil demand despite recycling rates improving from 15% in 2019 to 35% in 2040. Bans on plastic bags and increased recycling are anticipated to have little impact on oil demand. Petrochemical feedstocks – specifically naphtha, liquefied petroleum gases, and ethane – are expected to account for half of the growth in global demand through 2025 according to the IEA’s Oil 2020 report from March. In recognition of this trend, midstream companies like Enterprise Products Partners (EPD) and Inter Pipeline (IPL) are expanding into petrochemicals (read more).

Long-term projections for anything energy-related are difficult, but COVID-19 has further clouded the crystal ball for estimating future oil demand. Work-from-home trends may lead to permanent demand destruction from would-be commuters. Other areas of oil consumption, like shipping, may not see any lasting impact. Even international travel for pleasure or business will likely return with a vaccine. In short, projections made prior to COVID-19 should be viewed in context, but the extent to which COVID-19 has impacted the outlook for 2030 oil demand is likely debatable and possibly minimal.

Bottom line

There are a multitude of moving parts surrounding the future adoption of electric vehicles and the impact to oil demand, including government policies, infrastructure investment, mineral supplies, and technological developments to name just a few. Overall, the oil demand impact over the next few years does not appear needle moving. Even in a scenario with significant EV sales share in 2030, the oil demand implications look moderate. Going forward, petrochemicals are expected to lead the way for demand growth as oil demand from passenger vehicles peaks.

{kind=link}