President Biden’s Proposed Tax Hike: Potential Implications and Opportunities for Tax-Efficient Income

While tax-efficient investing has an evergreen appeal, the prospect of higher tax rates in the US for corporations and wealthy individuals has made tax considerations top of mind for investors and their advisors. President Biden supports raising the corporate tax rate from 21% to 28% as has been widely reported. Additionally, the Biden Administration has proposed raising the income tax rate for the highest earners from 37% to 39.6% (or 43.4% including the Medicare surtax) and increasing the rate on capital gains and dividends from 20% to 39.6% (43.4% with the surtax) for those with annual income above $1 million. Acknowledging that there is plenty of politicking and possible compromising yet to be done, this note discusses a few of the potential implications of the tax hike and solutions for investors seeking tax-exempt or tax-deferred income.

Broad market implications and the impact on mutual funds.

With the strength in broad US equity markets over the last several years, wealthy individuals likely have sizable capital gains that they may choose to realize ahead of any potential hike in the capital gains rate. This could result in some selling pressure for equities. As discussed in this Bloomberg article, investors in mutual funds may sell to realize gains at a lower tax rate and reallocate to more tax-efficient ETFs. Recall, mutual funds often have to sell out of positions to raise cash to satisfy redemptions, resulting in capital gains for their shareholders, whereas ETF shares are bought and sold among investors. A higher capital gains rate would be expected to further underscore the tax efficiency of ETFs relative to mutual funds.

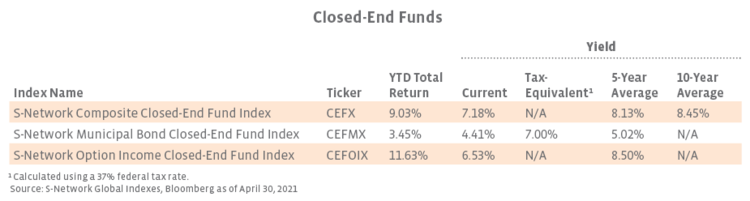

Wealthy individuals are likely to reexamine opportunities for tax-exempt or tax-deferred income. Municipal bonds can provide income exempt from federal taxes and potentially state taxes if owned by a resident of the state of issue. Closed-end funds may be an attractive way to gain diversified exposure to municipal bonds with leverage potentially enhancing yield. At the end of April, the S-Network Municipal Bond Closed-End Fund Index was yielding 4.4% or 7.0% on a tax-equivalent basis using the current top tax rate of 37% (learn more about this index).

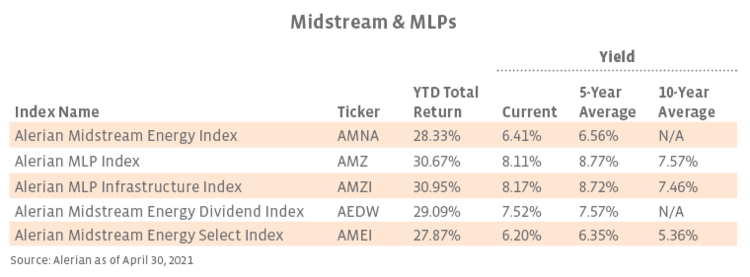

For tax-deferred income, Master Limited Partnerships (MLPs) may represent an attractive option for investors. Typically 70-100% of MLP dividends (called distributions) are considered to be a tax-deferred return of capital, which means the taxes on that portion of the income are not paid until the investment is sold. The portion of the distribution that is not a tax-deferred return of capital is taxed at ordinary income rates in the current year. Investors comfortable with filing a form K-1 for tax purposes can invest directly in MLPs for potential tax-deferred income, or alternatively, MLP ETFs provide a 1099 tax form and greater diversification while maintaining the tax character of distributions from their underlying holdings. For additional information, please see this piece on MLP Taxation and this piece on MLP Investment Products. As of the end of April, the Alerian MLP Index was yielding 8.1%. Finally, as pass-through entities, MLPs do not pay taxes at the company level, and an increase in the corporate tax rate would widen MLPs’ tax advantage relative to corporations (read more).

Alerian is not a tax advisor. This commentary is not intended to be tax advice.

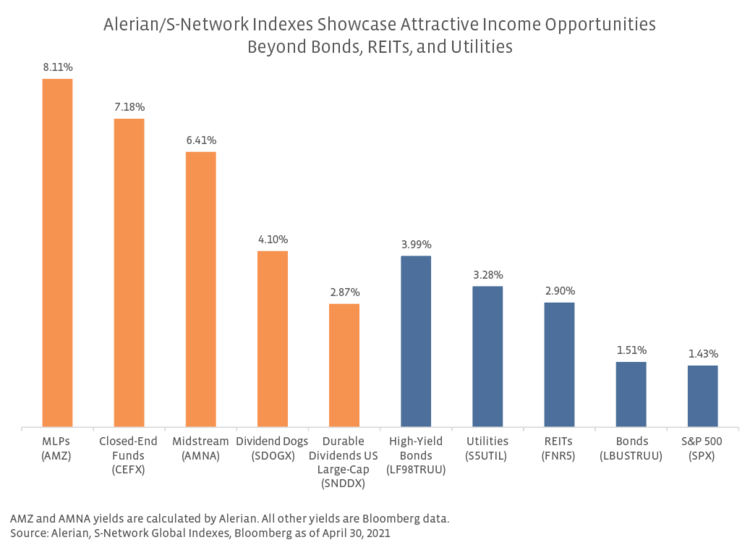

Current Yields vs. History

Midstream yields are largely in line with historical 5-year averages, though above the 10-year averages.

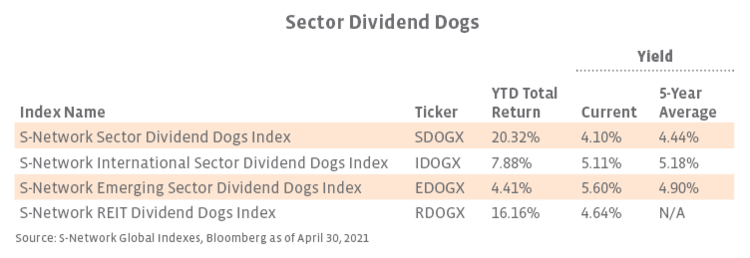

The S-Network Sector Dividend Dog Indexes have provided solid year-to-date performance, while offering more generous yields than their relevant benchmarks.

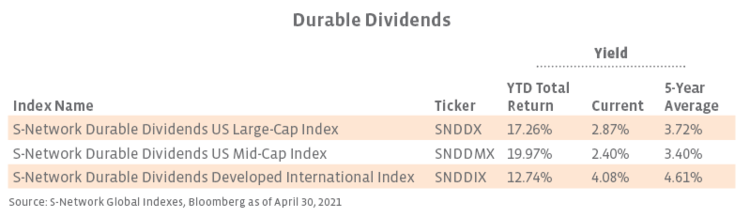

Multiple screens for dividend durability, including evaluating cash flows, EBITDA, and debt-to-equity ratios, help ensure reliable income from the durable dividend indexes. While current yields are below the 5-year average, they are well above the S&P 500’s current 1.43% yield.

Though current yields are below historical averages, closed-end funds continue to represent an attractive option for enhancing the yield of an income-oriented portfolio. As noted above, municipal bond closed-end funds may be particularly attractive given that muni bonds generate interest income that is exempt from federal taxes.

Related Research:

MLPs Taxation: The Benefits and What You Need to Know

Muni CEFs: Enticing Tax-Exempt Income and Diverse Exposure

A Smarter Approach to Closed-End Funds

Could Private Equity Activity in Midstream Pick Up in 2021?

Midstream/MLPs: 2020 Cost Discipline Has Benefits into 2021

| Underlying Index |

Associated Product |

| Midstream/MLPs |

|

| ETRACS Alerian Midstream Energy Index ETN (AMNA) |

|

| JP Morgan Alerian MLP Index ETN (AMJ), ETRACS Alerian MLP Index ETN Series B (AMUB), ETRACS Quarterly Pay 1.5X Levered Alerian MLP Index ETN (MLPR), Available on the C8 platform |

|

| ETRACS Alerian Midstream Energy High Dividend Index ETN (AMND), Alerian Midstream Energy Dividend UCITS ETF (MMLP) |

|

| Alerian MLP ETF (AMLP), ETRACS Alerian MLP Infrastructure Index ETN Series B (MLPB), Available on the C8 platform |

|

| Alerian Energy Infrastructure ETF (ENFR), Available on the C8 platform |

|

| Sector Dividend Dogs |

|

| ALPS Sector Dividend Dogs ETF (SDOG) |

|

| ALPS International Sector Dividend Dogs ETF (IDOG) |

|

| ALPS Emerging Sector Dividend Dogs ETF (EDOG) |

|

| ALPS REIT Dividend Dogs ETF (RDOG) |

|

| Durable Dividends |

|

| Available on the C8 platform and the SMArtX platform |

|

| Available on the C8 platform and the SMArtX platform |

|

| S-Network Durable Dividends Developed International Index (SNDDIX) |

Available on the C8 platform |

| Closed-End Funds |

|

| Invesco CEF Income Composite ETF (PCEF), ETRACS 1.5X Leveraged Closed-End Fund ETN (CEFD), Available on the C8 platform |

|

|

S-Network Municipal Bond Closed-End Fund Index (CEFMX)

| VanEck Vectors CEF Municipal Income ETF (XMPT), Available on the C8 platform |

| S-Network Option Income Closed-End Fund Index (CEFOIX) | Available on the C8 platform and the SMArtX platform |