The original cotillion was an 18th century social dance that involved four couples dancing simultaneously, often changing partners throughout the song. As commodity prices change, a modern day market dance has investors examining how movements affect MLPs.

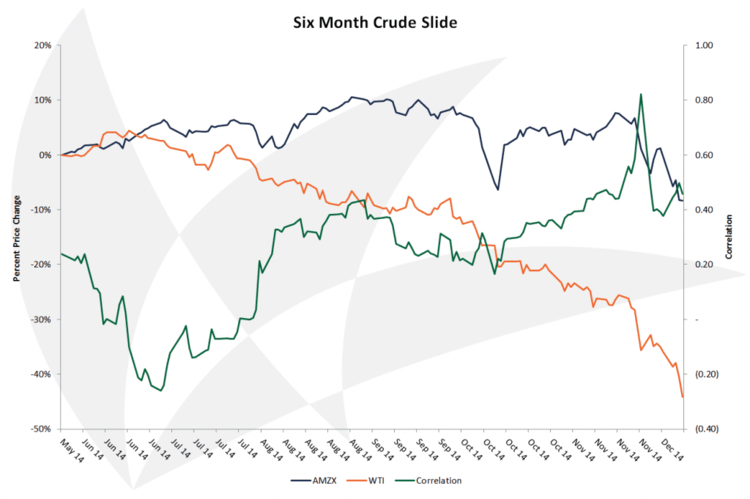

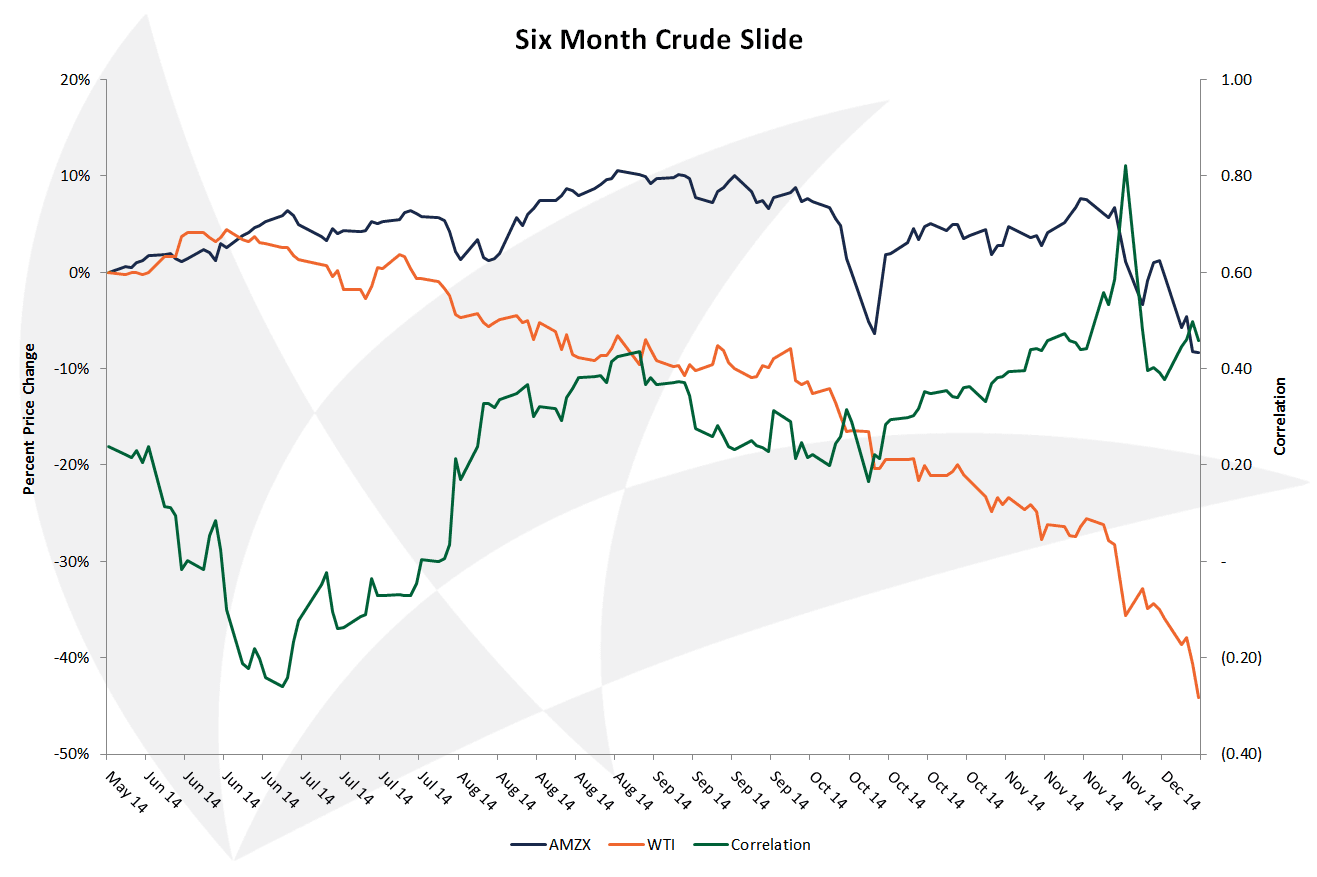

MLPs with direct commodity price exposure, such as upstream MLPs, have been the hardest hit by the six-month slide in crude prices. Many of these companies hedge their forward exposure for one to five years, if not longer. So while their cash flows have not yet been affected, they are already trading as if 2016 is just around the corner. Additionally, investors are concerned about upstream MLPs tripping their debt covenants, as the value of their reserves (the base against which they can borrow, determined semi-annually) are repriced at lower levels.

Historically, Gathering and Processing (G&P) MLPs have signed percentage-of-proceeds (POP) or keep-whole contracts, in which they share commodity price risk with the producer. In a POP contract, the MLP receives a percentage of proceeds from the sale of natural gas and NGLs, so its margins rise and fall with natural gas and NGL prices. In a keep-whole contract, the MLP keeps the NGLs and returns the natural gas to the producer, so the partnership’s margins are directly related to NGL prices and inversely related to natural gas prices. However, since the commodity bust that occurred in the second half of 2008, most MLPs have moved to fee-based contracts, where the MLP earns a fixed fee per volume of gas processed. Though fee-based contracts eliminate direct commodity price exposure for the G&P MLP, volumes at the processing plant are dependent on production volume at the wellhead.

If commodity prices remain depressed, producers will shut in current production and delay drilling new wells, reducing volumes moving through all supply-based infrastructure assets, including pipeline takeaway capacity and related storage with a toll-road business model (tariff x volume). This scenario, which lowers revenues on those assets, has played out in the Haynesville and Fayetteville, which are primarily dry gas fields. On the other hand, a sustained period of very high prices will push consumers to cut back on consumption, reducing volumes moving through demand-based infrastructure assets. Both of these are mitigated to some extent: mineral rights land leases often include minimum production requirements, pushing producers to operate at prices below marginal cost over the short term. And US energy demand has a floor based on the necessity to heat northern homes in the winter, cool southern homes in the summer, turn the lights on, and drive to work, regardless of how high prices go. Both phenomena should also be self-correcting over the long term: lower pricing reduces supply, creating an imbalance with higher demand that is corrected by an increase in prices. Higher pricing has the exact opposite effect.

This is all a very long way of saying that long-term fundamentals for energy infrastructure assets remain generally unscathed. But MLP unit prices are a different matter entirely, being decided solely by the market. In an efficient market, prices are informed by the fundamentals of the underlying businesses. In reality, investor psychology, cognitive and emotional biases, and broader market contagion also play a role. Shorter-term investors may trade MLPs based on fear of headline risk of moving commodity prices.

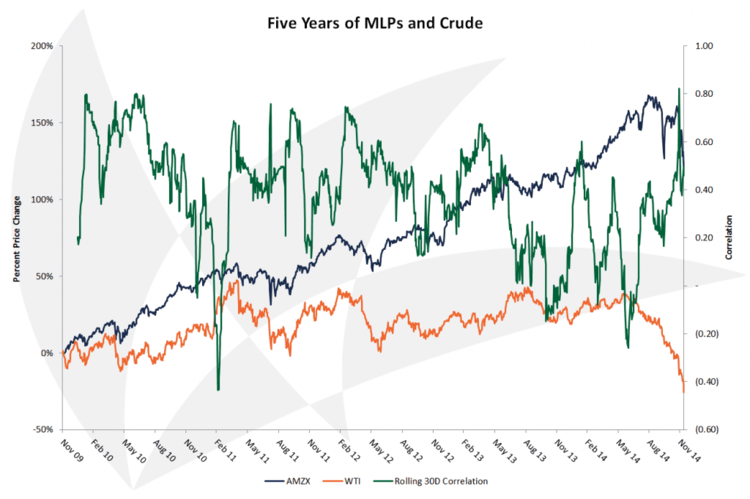

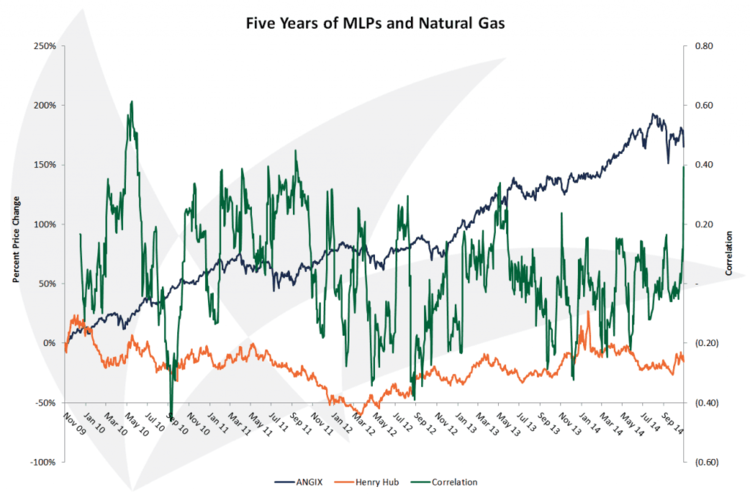

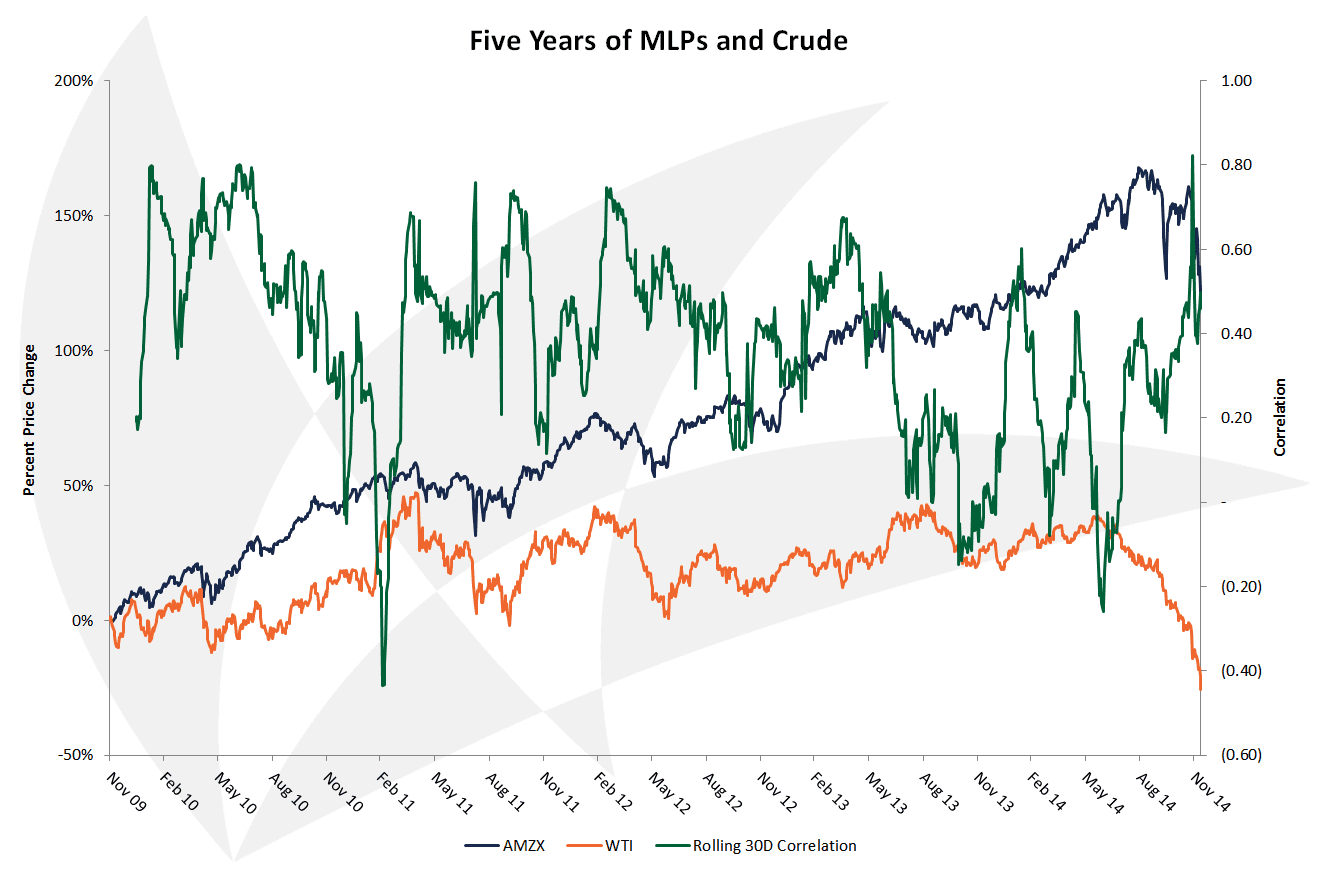

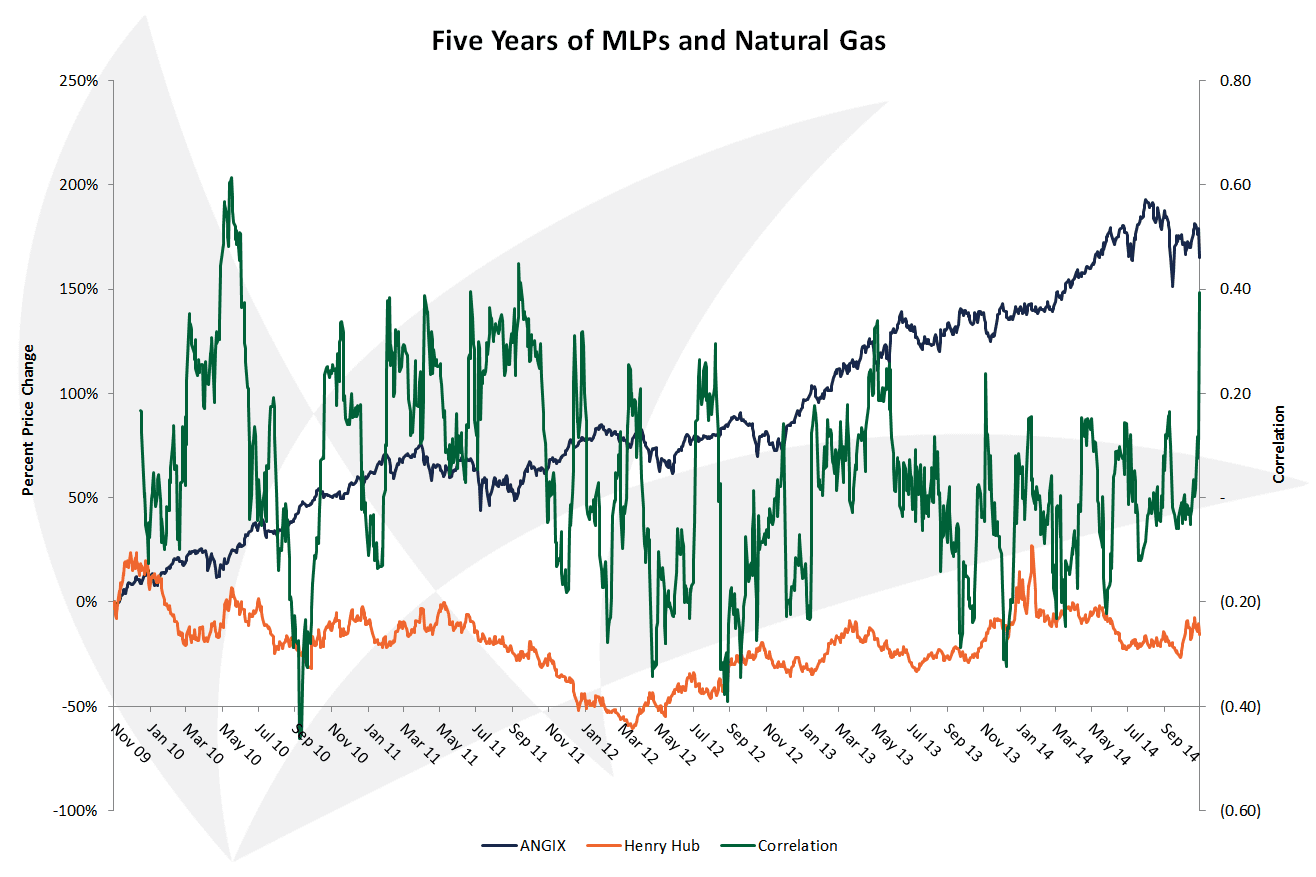

That said, the correlation between MLPs and crude has actually been rather inconsistent over the past five years.

{kind=link}

{kind=link}

{kind=link}