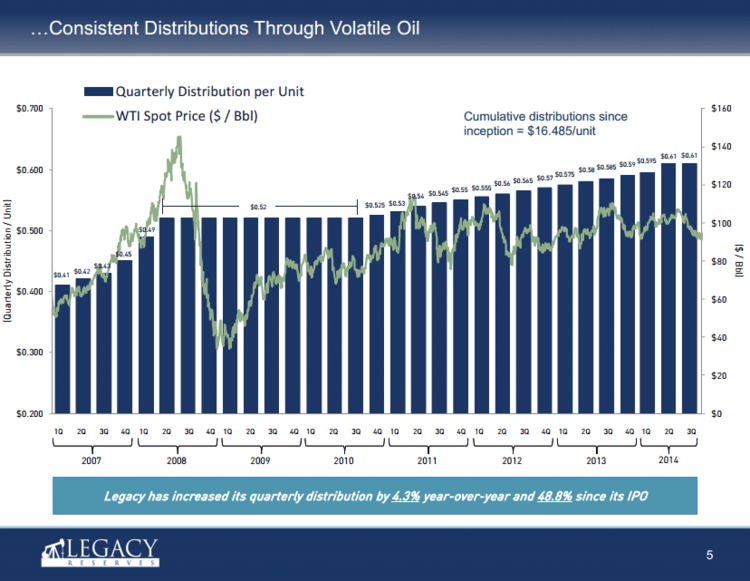

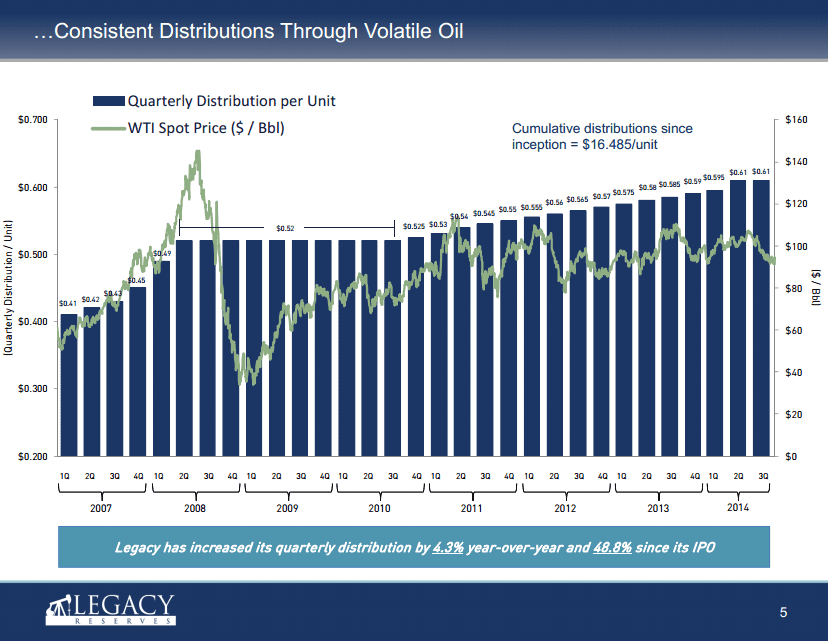

What made the difference? Let’s use an example from each camp. First, Legacy Reserves (LGCY), one of the upstream MLPs that kept its distribution flat this quarter, and has maintained or grown its distribution every quarter since its 2007 IPO. As you can see below, the company managed to do this even during the oil crash of 2008.

When LGCY makes an acquisition, it partially hedges production for the next 3-5 years. Its oil production is 68% hedged for 2015 around $92, and its gas production is 76% hedged at $4.38. For 2016, 21% of oil production is hedged at $89, as is 20% of gas production at $4.26. That’s a decent amount of forward production sold at prices much higher than today’s.

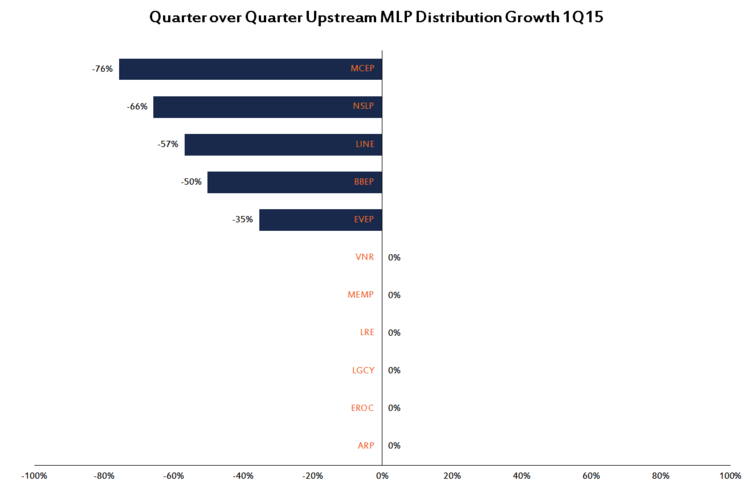

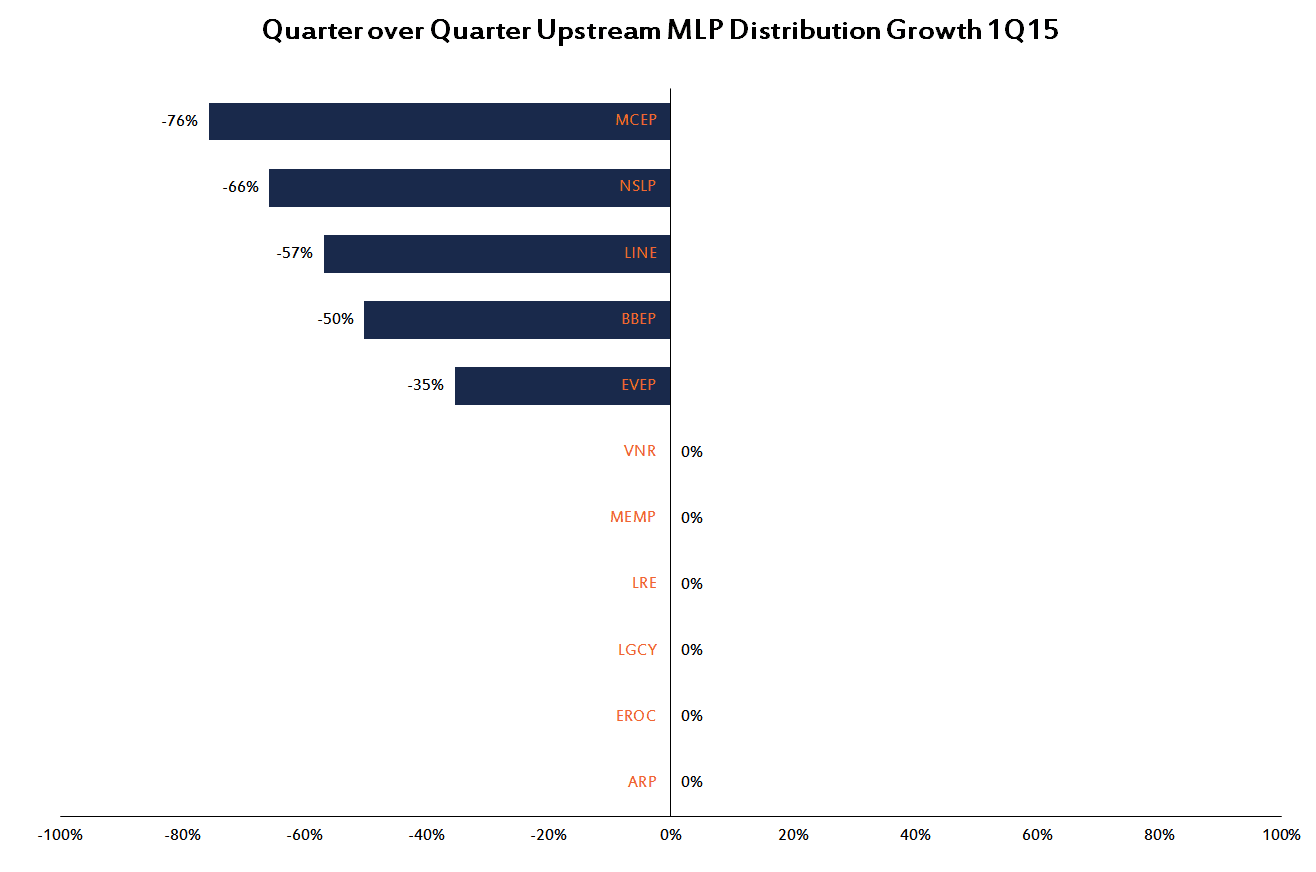

On the other end of the spectrum is Mid-Con Energy Partners (MCEP), which cut its quarterly distribution 76% to $0.125 from $0.515. MCEP has 98% of its production weighted towards crude, and has hedged 74% of 2015 oil production at $76 and 56% of 2016 production at $70.

If the average price of crude stays at $50 for 2015, LGCY’s oil-related cash flow is better positioned.

LGCY 2015: (68% * $92) + (32% * $50) = $78.56

MCEP 2015: (74% * $76) + (26% * $50) = $69.24

But if oil prices stay at $50 through 2016, MCEP is better positioned.

LGCY 2016: (21% * $89) + (79% * $50) = $58.19

MCEP 2016: (56% * $70) + (44% * $50) = $61.20

By keeping its distribution flat for now and hedging out a lower percentage of 2016 production, LGCY is taking the more uncertain route of hoping that oil prices recover before next year is over. By cutting its distribution now instead, MCEP sports a coverage ratio of nearly two times, giving the company some wiggle room if prices don’t rebound sooner. LGCY is waiting it out, and MCEP is being more proactive. It may also be more psychologically difficult for a company that has paid eight years of stable and growing distributions (LGCY) to grab the knife than for a company with just over three years of trading history (MCEP) under its belt to do the same. Since crude oil’s June 20th peak, LGCY is down 52.5% on a price return basis while MCEP is off 69.1%. Sure, the former has done 16.6% better, but the market isn’t exactly treating LGCY’s current distribution as secure.

If you’re panicked that the upstream names are taking the entire MLP structure down with them, remember that they are only about 3% of MLP market cap. Assuming the weightings in your diverse MLP portfolio are consistent with the broader universe, a worst-case scenario where every upstream MLP goes bankrupt costs you 300 basis points of performance.

{kind=link}

{kind=link}