(click to enlarge)

Average outperformance of a company added to either index has been 316 basis points (bps), ranging from 4 bps to as high as 612 bps. We like to call this phenomenon “The Alerian Effect”, shamelessly coined after the “S&P Effect”, describing how a company’s share price jumps when they are selected to the S&P 500 Index (SPX), since all the products tracking the index will need to buy the company’s shares.

As of August 29, over $21 billion in assets (via ETNs, ETFs, SMAs, mutual funds, structured notes, total return swaps, and variable insurance products) are linked to the AMZ ($7.7 billion) and AMZI ($13.3 billion).

If an MLP is added to the AMZ with a 1% weighting, then $77 million worth of units (shares) would need to be bought by tracking products. Read By the Numbers: Trading Days to Exit for how many trading days it would take to buy $77 million worth of an MLP.

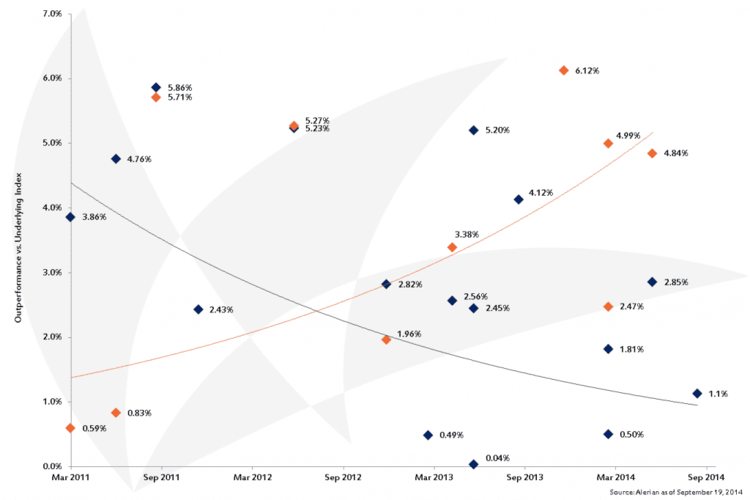

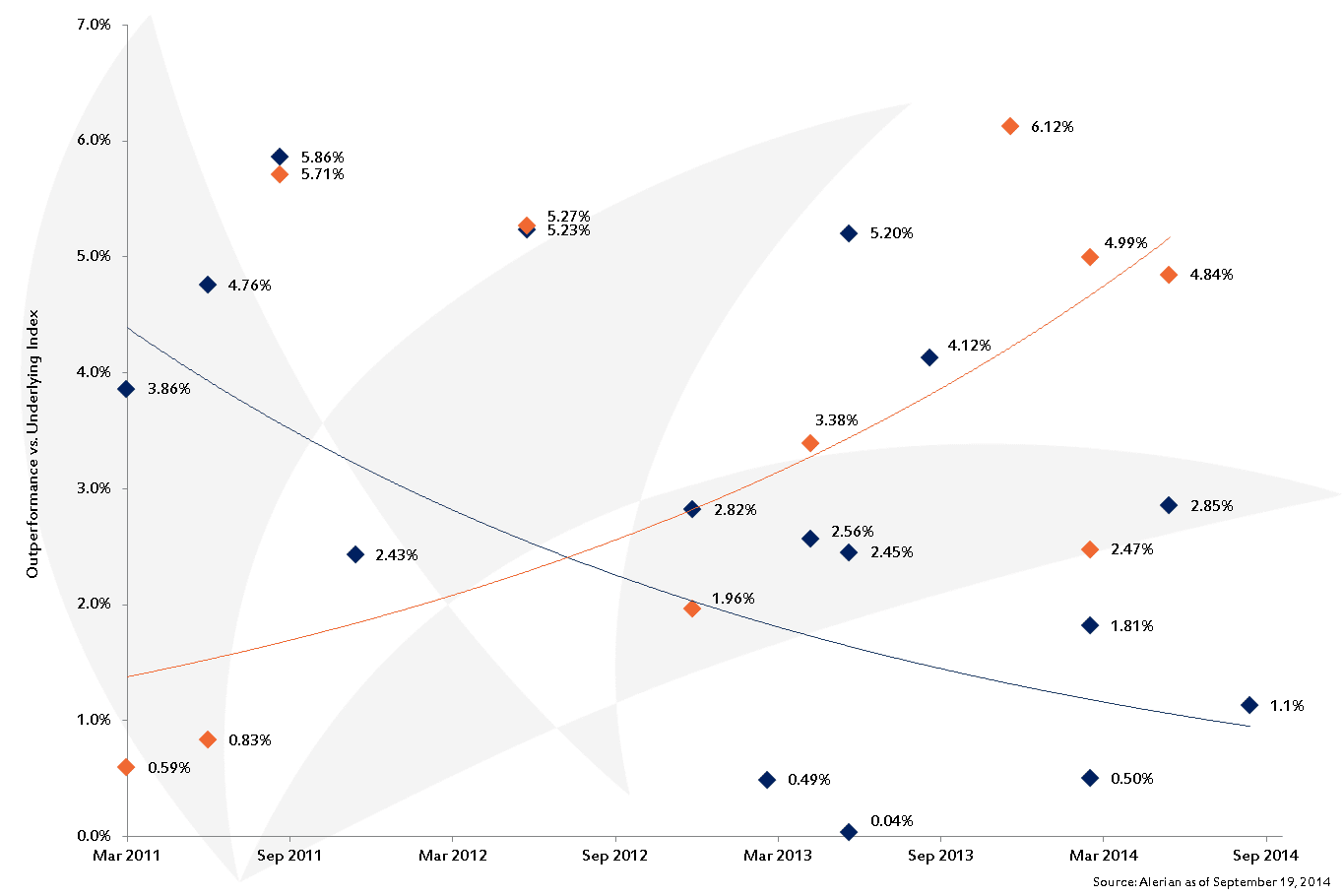

As you look at the chart, you’re probably noticing the upward trending orange line for the AMZI and downward plateauing blue line for the AMZ. The R-squared value for the AMZI orange line and AMZ blue line are 0.36 and 0.14, respectively, so neither line is definitely conclusive of a trend. But, we wanted to include the line to show that the “AMZI Effect” (362 bps outpeformance) has become more pronounced than the “AMZ Effect” (288 bps outperformance), as the amount of linked product AUM tracking the AMZI has exceeded that of the AMZ since late 2012. The AMZI also only has 25 constituents to the AMZ’s 50, so constituent weightings tend to be higher in the AMZI, meaning more units need to be bought.

Due to the Alerian Effect, AMZI Effect, and AMZ Effect (or whatever you want to call it), we cannot stress enough the importance of an index provider being independent and without conflicts of interest. Similar to how public companies have quiet periods before earnings, Alerian engages in a two-week quiet period from the first to third Friday of every quarterly rebalancing month, where we refrain from discussing rebalancing and/or clarifying methodology. Now that the September rebalancing is complete, we’re happy to answer any questions you may have.

In the next part of this series, we will discuss the day-of announcement impact to MLPs being removed from the index, as well as equity performance between the announcement and rebalancing dates for entering and exiting names. Stay tuned.

{kind=link}