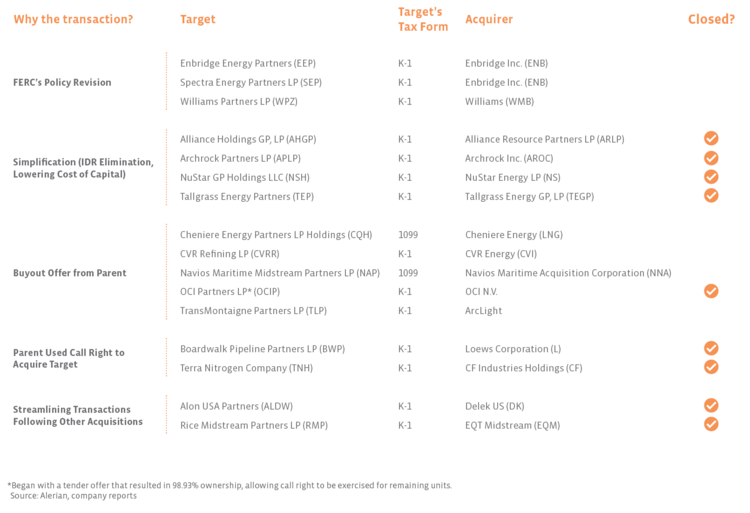

Why the transactions?

In the table, we oversimplify by grouping transactions into different categories, but please don’t think the category represents the only reason for the transaction. We classified the roll-ups from Williams (WMB) and Enbridge (ENB) as being motivated by the FERC’s policy revision from March 15th (Alerian’s commentary), because FERC was prominently discussed in the press releases announcing the transactions. However, both also point to a simplified structure as a benefit of the transactions. To be clear, ENB had discussed simplifying its corporate structure at its December 2017 analyst day – well before the FERC announcement on March 15, 2018. FERC’s final ruling last week (Alerian’s commentary), which clarified that a natural gas MLP pipeline with a C-Corp parent is eligible for an income tax allowance in its cost-of-service rates if its financials are fully consolidated on the income tax return of its parent, is an interesting development, which we will discuss in greater detail next week.

Three of the four transactions included in the Simplification category resulted in the elimination of incentive distribution rights (IDRs). AHGP/ARLP is the exception, as ARLP’s IDRs were already eliminated in 2017. As we’ve written about in the past, IDRs can become burdensome to an MLP’s cost of capital over time, and they can be off-putting to investors. Consolidating the GP and LP is one way to eliminate IDRs, but it’s not the only way. Other MLPs have bought out their GP interest and the associated IDRs, primarily by issuing LP units in exchange for the GP’s interest.

Other transactions involve a parent or sponsor offering to buy out the public units of an MLP or using a call right to buy the outstanding LP units. The motivations for the transactions may vary, but clearly, the parent sees some value in consolidation and/or views the MLP as undervalued. CVR Energy (CVI) believes holders of CVR Refining (CVRR) may prefer to be invested in common stock, rather than partnership interests, as noted in its exchange offer announcement. As a private equity firm and owner of the GP, ArcLight must see value in owning TransMontaigne Partners (TLP) outright. Cheniere’s (LNG) consolidation of CQH fits with the goal of reducing the complexity of its corporate structure in its investor presentation.

What are the repercussions for direct MLP investors?

These transactions can be frustrating or cause headaches for investors depending on how they’re structured. For example, holders of Spectra Energy Partners (SEP) and Enbridge Energy Partners (EEP) are likely frustrated by the fact that no premium was offered for their units – a concern addressed by ENB in transaction-related FAQ’s on its website. It’s unclear at this point whether the clarifications in FERC’s final ruling will have any bearing on the proposed transactions.

The tax implications of these transactions could also be frustrating, but each situation will be unique and depend on the unitholder’s basis. For example, transactions are expected to be (or were) taxable for holders of EEP, SEP, WPZ, APLP and TEP as basis is stepped up. That said, ENB’s management indicated on the restructuring call that they expected minimal tax, if any, to be paid by holders of EEP and SEP. Notably, the surviving entity tends to reap the benefits of this basis step-up, delaying cash taxes for years. For example, WMB doesn’t expect to pay cash taxes through 2024, and Tallgrass Energy (TGE), the renamed entity following the TEP/TEGP merger, doesn’t anticipate paying cash taxes for at least a decade.

For investors who bought these MLPs for their yield, changes to income are likely a concern in some cases. NS announced a distribution cut in its merger announcement. Other unitholders will see less income post-transaction from the surviving corporation than they enjoyed with their MLP investment. For example, WMB’s most recent dividend of $0.34 and a stock-for-unit ratio of 1.494 per WPZ unit implies a quarterly dividend of $0.508 per legacy WPZ unit post-transaction, compared to WPZ’s most recent distribution of $0.629. Similarly, APLP’s last distribution paid in February was $0.285 per unit, while AROC’s May dividend was $0.12. Adjusting for the 1.40 AROC shares received for each APLP unit, a unitholder’s quarterly income would have fallen by $0.117 per legacy APLP unit post-transaction. Notably, there was no distribution cut for legacy TEP holders in the TEP/TEGP transaction.

Another potential tax issue could be the changing profile of the dividend received post-transaction. Typically, 70-100% of an MLP’s distributions are considered a tax-deferred return of capital. A significant portion of a corporation’s dividend could still represent a return of capital, but it’s also possible that less of the dividend will be considered a return of capital going forward, either immediately or in the future. The tax treatment will likely be situational, but Kinder Morgan (KMI), which consolidated four public entities into one corporation in 2014, provides some commentary on its website about its dividend that may be helpful context. [Editor’s Note: Please consult your tax advisor on these matters.]

Bottom line

Reorganizations are happening for a variety of reasons. While several have already been announced, there are likely more to come as we’ll discuss next week. Each company will ultimately have to choose the structure that is best for its situation. For some companies, a C-Corp structure is viewed as a better fit given the potential to attract a broader investment base that may be hampered by a K-1. However, converting to a corporation does not change the asset base or business prospects of a company. In other words, it’s not a silver bullet. Stay tuned for next week!

2018.07.24 3:45pm CST – Added the word “potentially” in the second paragraph.

Alerian is now on Twitter! Join the conversation with @AlerianIndices.

{kind=link}