Why the potential transactions?

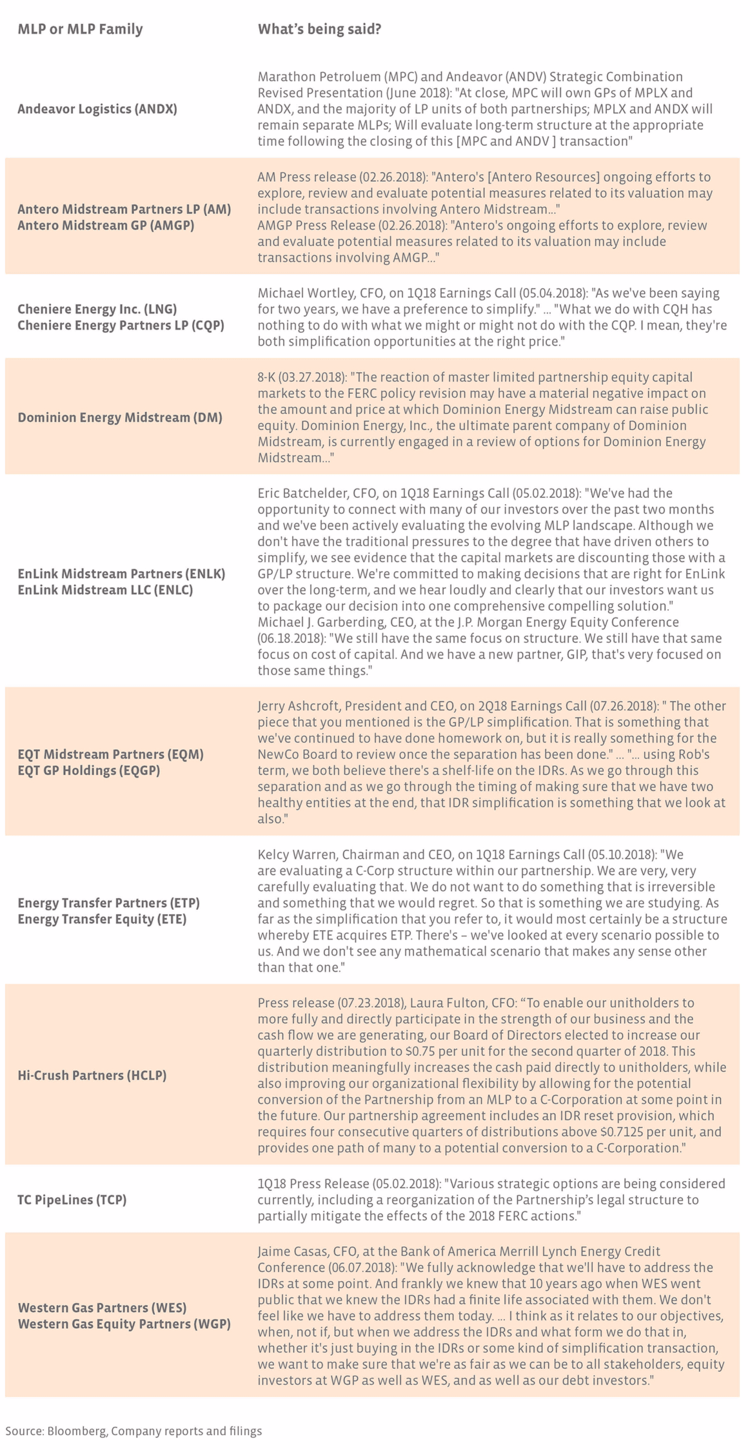

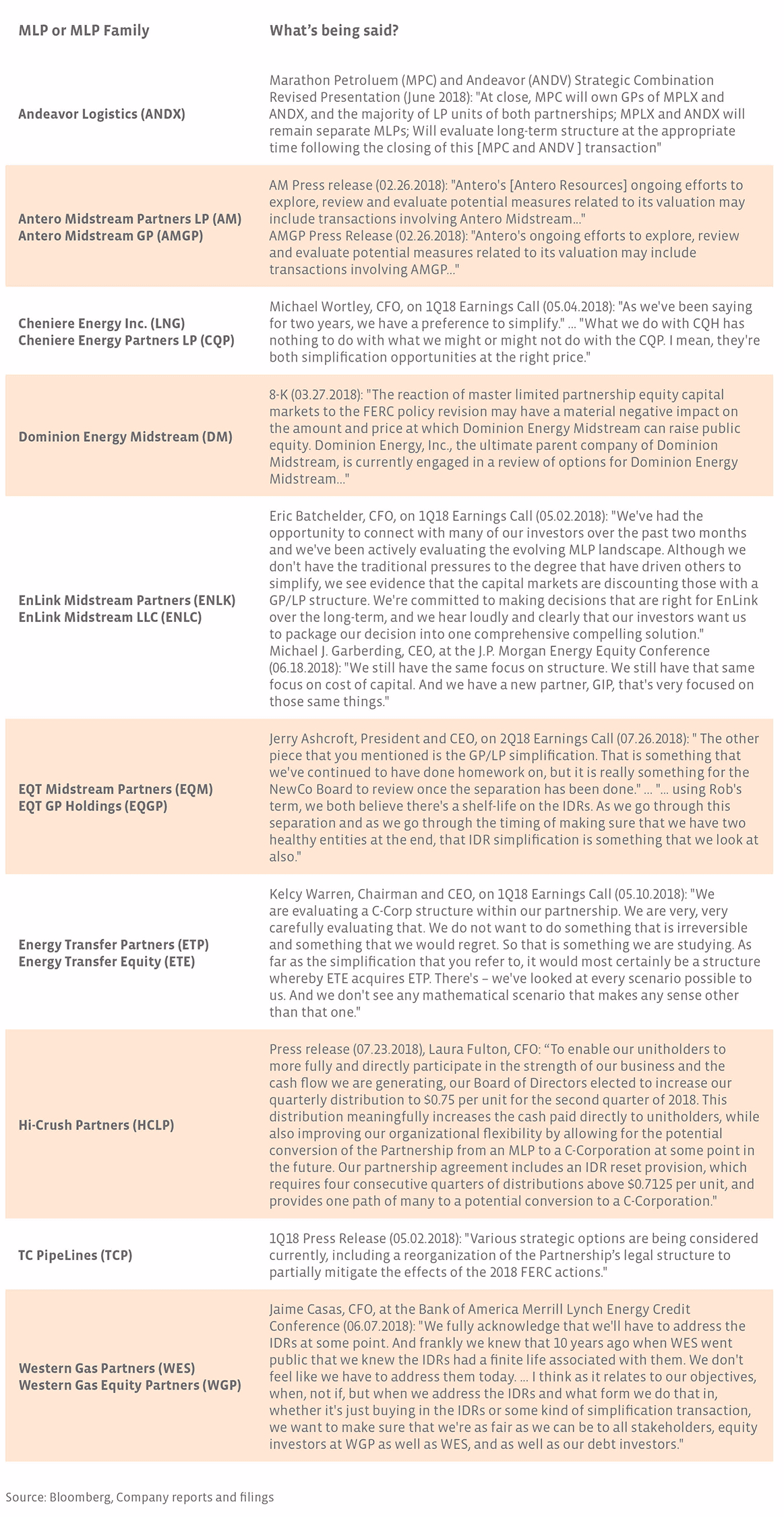

The rationale for potential transactions or structural changes varies, but in many of the cases above, reorganizations or simplification transactions are discussed in the context of the GP/LP structure or IDRs needing to be addressed. As we have discussed in the past, IDRs can become a burden to the cost of equity over time. A company doesn’t have to undergo a reorganization to eliminate IDRs, though a reorganization may be more common if the GP is a publicly traded pure play. Even in that case, the MLP could be the surviving entity, as we saw with NuStar’s (NS) merger with NuStar GP Holdings (former ticker: NSH). Alternatively, both entities could continue to trade as we saw in the simplification transaction between Plains All American (PAA) and Plains GP Holdings (PAGP) that eliminated PAA’s IDRs in 2016. Clearly there is optionality when it comes to addressing IDRs or pursuing simplification, and eliminating IDRs is not the only possibility. At the end of June, Dominion Energy Midstream (DM) (discussed more below) issued 26.7 million units to its GP in an IDR reset, which helps reduce the cost of equity.

If history is any guide, an acquisition of the MLP’s parent by another company with an MLP tends to result in a merger of the MLPs owned by the acquirer and the target. A recent example includes EQT Midstream’s (EQM) merger with Rice Midstream Partners (former ticker: RMP) following EQT Corporation’s (EQT) acquisition of Rice Energy. In February 2018, EQT announced that it would pursue the merger of EQM and RMP along with its plans to create a new corporation focused on midstream. Of the MLPs listed in the table above, Andeavor Logistics (ANDX) is the only company whose parent is in the process of being acquired by another MLP parent.

Both DM and TC PipeLines (TCP) discuss the FERC policy revision from March 15th (Alerian commentary) in the context of reviewing options. Both equities had suffered following the announcement, with DM discussing the potential negative impact on its ability to raise equity and TCP noting the impairment of dropdowns. From March 14th through July 18th, both MLPs had seen their prices fall by more than 40%. DM and TCP gained 23.4% and 27.3%, respectively, on July 19th after FERC’s final ruling (Alerian commentary) was viewed to be more favorable than the initial policy revision from March. It will be interesting to see what each company says on its 2Q earnings calls in light of the latest FERC announcement and any bearing the final ruling may have on how management views structure going forward. DM will hold its 2Q call tomorrow morning, August 1st, and TCP will hold its 2Q earnings call Thursday afternoon, August 2nd.

In the case of the Antero family, Antero Resources (AR) announced in late January that it was evaluating measures to address the discount in AR’s stock relative to peers. In February, special committees were announced at AM and AMGP to consider any potential transactions related to AR’s strategic evaluation. A transaction involving AM and AMGP may or may not occur. Turning to the Cheniere complex, management has discussed simplification for some time and has taken the first step in announcing Cheniere Energy’s (LNG) acquisition of Cheniere Energy Partners LP Holdings (CQH), with the announcement following the 1Q18 call referenced above.

Bottom Line

While several MLPs have discussed restructuring, addressing IDRs, consolidation, and/or simplification, questions around timing, the structure of any transaction, and the direct implications for unitholders are difficult to answer until a transaction is announced. Our intention has been to avoid speculating on the answers to these questions, and we would note that transactions may not materialize. Instead, we have tried to identify those companies that are potential candidates for reorganization based on public statements. As a reminder, last week, we discussed some of the repercussions for direct MLP investors for transactions that have been announced, and that could provide helpful context. Looking forward, next week we’ll address what this all means for MLP investors and the ways MLP investors choose to gain exposure to energy infrastructure. Please stay tuned!

{kind=link}