What fits better in your portfolio based on your objectives?

“I want the yield and tax-deferred return of capital associated with MLPs.”

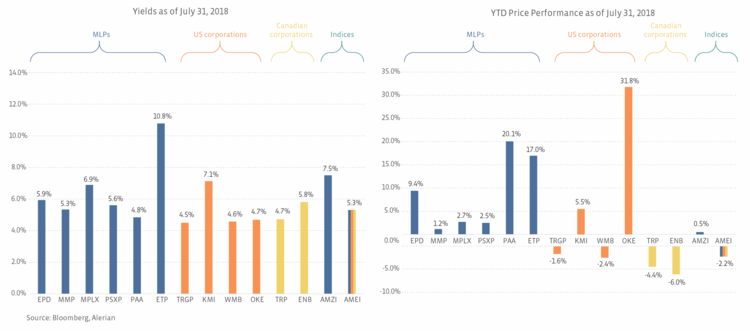

In most of our conversations, investors have allocated to the MLP space for yield and the tax-deferred return of capital benefit. If that is your primary investment objective and you don’t want to own MLPs directly, then you will most likely want to own a product that is predominately MLPs. Though there are some exceptions, corporations generally have lower yields than MLPs. If you really want yield, then you should have no fear of missing out from owning a product that does not include corporations. Funds that predominately own MLPs are more suitable for taxable investors seeking after-tax yield.

“I want broad exposure to energy infrastructure.”

If you want broad exposure to energy infrastructure, you will want to own a product with both MLPs and corporations. For even broader exposure, you may want a product with US and Canadian energy infrastructure companies as well as MLPs. You will most likely want to access the space through a RIC-compliant product that owns no more than 25% MLPs. A RIC-compliant product is more suitable for total-return investors in a taxable account or for tax-advantaged investors.

“I want yield and a handful of corporations that I’m familiar with like Kinder Morgan (KMI) and Williams (WMB).”

Occasionally, we will hear investors express a desire to own both MLPs and some familiar corporations in a product. First, familiarity is not a good reason to include a company in your portfolio; for example, almost everyone has heard of General Electric (GE)… Within a predominately MLP product, adding a handful (10% weighting? 20%?) of corporations will not provide broad exposure and has the potential to dilute the yield. From a product standpoint, this “in-between” of mostly MLPs and a few corporations could lead to suboptimal yield relative to a 100% MLP product and suboptimal diversification relative to a RIC-compliant product. If you want both MLPs and corporations, a separately managed account (SMA) may be an attractive option, as you can avoid the RIC compliance issue, but SMA’s typically require a high minimum investment.

What does fewer MLPs mean for your investment?

First, we should preface this discussion by acknowledging that some MLPs have been delisted and some may delist in the future as a result of consolidation, but we do not believe the MLP structure is going to be fully abandoned. The MLP model is still attractive to investors and is sustainable in the long run, particularly once IDRs have been addressed and capital discipline has been adopted (i.e. self-funding). As an example, last week’s announcement that Energy Transfer Equity (ETE) would acquire Energy Transfer Partners (ETP) eliminates IDRs, and management discussed equity self-funding as a goal on the call. (As a reminder, ETE is an MLP.)

With that said, there are clearly fewer large MLPs today than there were at the start of the year. A decline in the number of large, investable MLPs could have implications for both active and passive products that predominately own MLPs. For example, investments may become more concentrated in the larger names, reducing diversification. The investment product’s yield may also change as holdings change. That said, yield-focused investors will likely still want to own a product that predominately owns MLPs. RIC-compliant products likely see less impact overall and less impact to yield as MLP ownership is already less than 25%.

What are the implications for MLP performance?

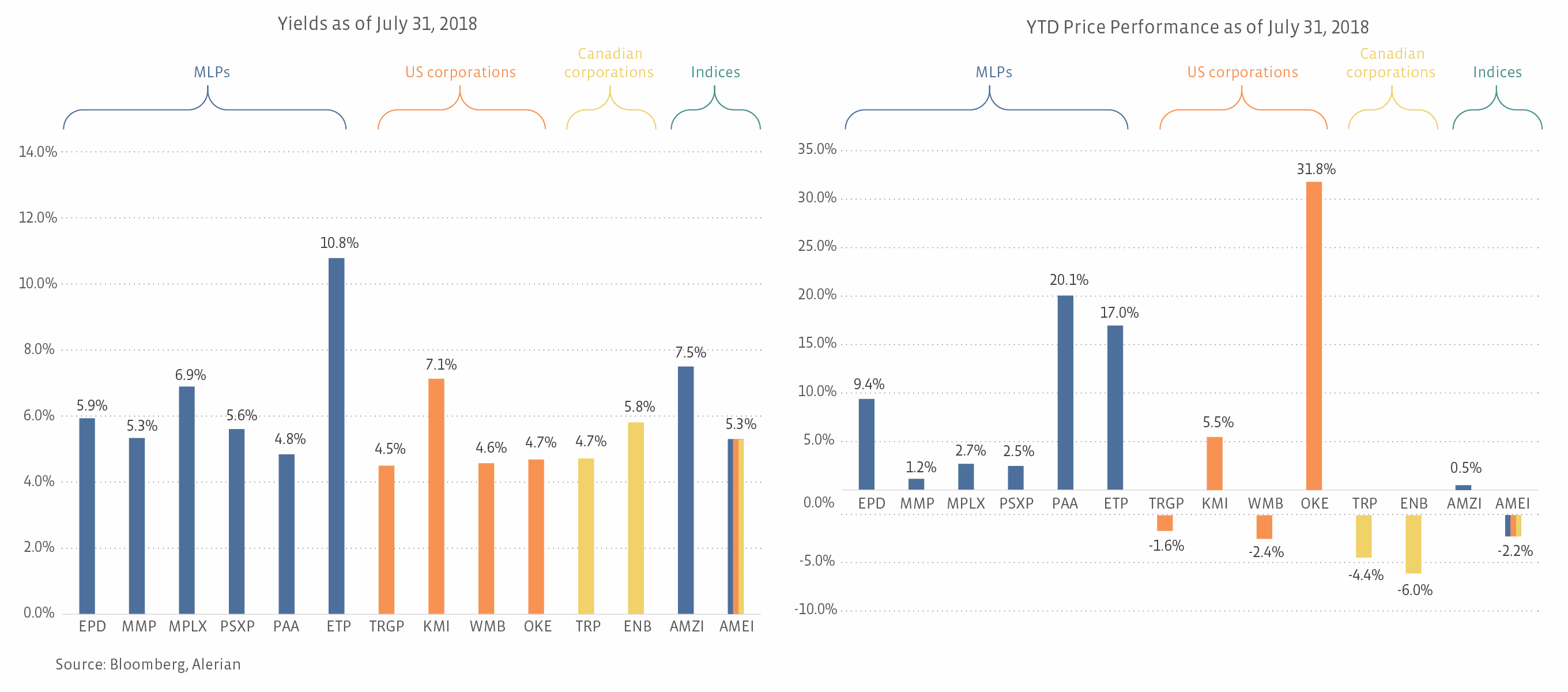

A decrease in the number of large, investable MLPs can also have an impact on performance. If managed money with an MLP mandate has fewer options, money could theoretically crowd into the remaining MLP names, which could be supportive for performance. On the other hand, it’s possible that funds that were predominately invested in MLPs may change their investment objective to become RIC-compliant, which again requires a 25% cap on MLPs. Changes to investment mandates could offset any uplift from MLP investments becoming more crowded.

For the last several months, the uncertainty surrounding potential transactions has likely weighed on performance and contributed to MLPs’ lagging performance relative to the improvement in crude prices. With all the headline risk in the MLP space, some money has likely been sidelined, as some investors prefer to wait for this period of restructuring to resolve before allocating to the space or prefer names without a restructuring overhang. Arguably, the sooner the space can get through this “growing pain phase” or “identity crisis” or “restructuring period”, then the better that may be for performance by alleviating uncertainty around restructurings and attracting fund flows into the space.

What about Alerian indices?

As an index provider in this space, we closely monitor changes in the energy infrastructure and MLP landscape. We have multiple benchmark indices that are formulaic, rules-based indices that rebalance according to their methodology guides, which are available on our website. Methodology guides are reviewed on a quarterly basis. Alerian intends that its benchmarks reflect industry trends and consults with key industry stakeholders in this process. An example is the recent launch of two new midstream indices (AMNA and AMUS) and a methodology change for the AMEI Index, which was renamed the Alerian Midstream Energy Select Index. Next week’s post will discuss the energy infrastructure universe and these two new indices.

Bottom line

Some MLPs have been consolidated by their parents, leaving fewer publicly traded MLPs than there were at the start of the year. If you invested in a 100% MLP product for broad exposure to US energy infrastructure, then these developments may cause you to think twice about your holding. However, if you invested in MLPs for yield, then a direct MLP investment or 100% MLP product should still align with your objective. If you’re looking for broad exposure to energy infrastructure or more focused on total return than yield, then you’ll probably prefer a RIC-compliant product that owns both MLPs and corporations. The bottom line for investors in MLP products is, “Do you want yield (80-100% MLPs) or broad exposure (less than 25% MLPs and 75+% corporations)?”

{kind=link}