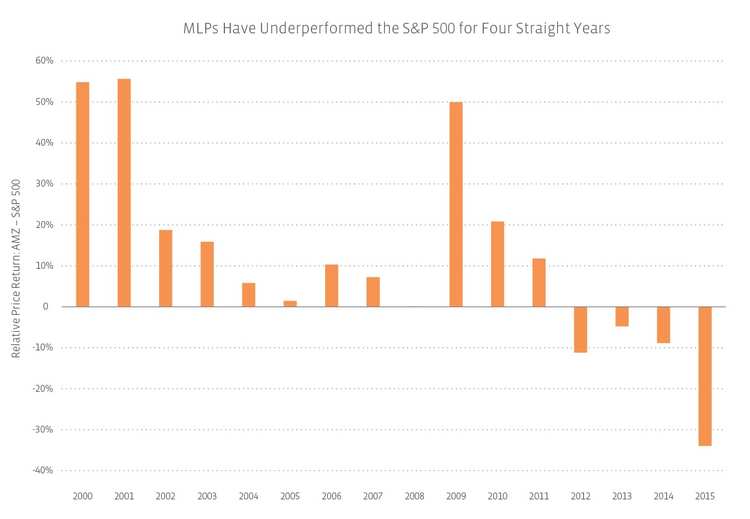

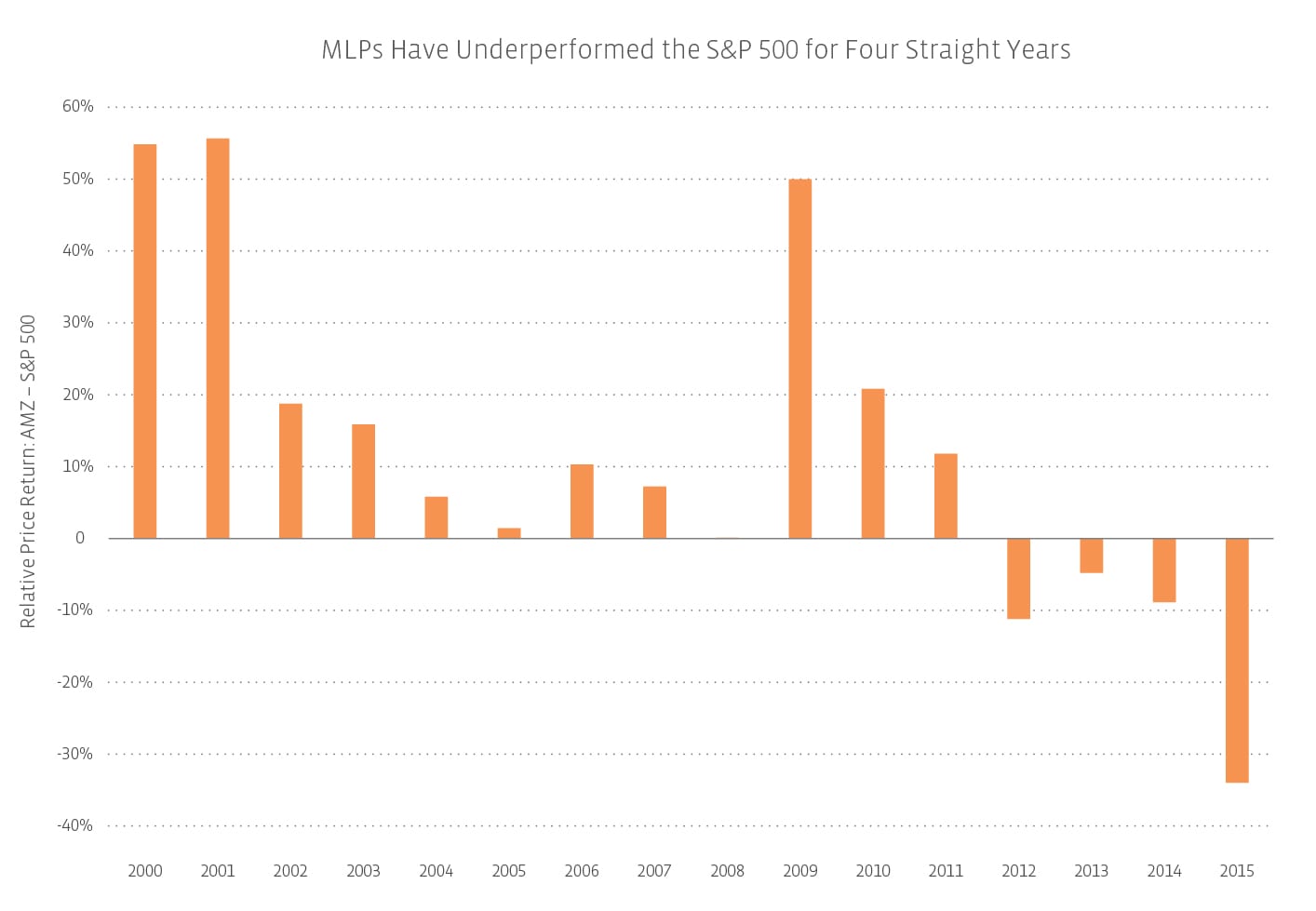

The AMZ shed 58.2% on a total return basis over 365 days, peak to trough. During the last MLP selloff, the AMZ lost 50.1% over 344 days. So why did it feel worse? The answer, as is often the case when discussing the financial markets, is a function of expectations. For one, it was assumed that a downturn of this magnitude couldn’t happen again after the 2008 commodity bust. And yet, when crude cratered again, many businesses were far less resilient than advertised. It also felt worse because MLPs were supposed to be due in 2015; after outperforming the S&P 500 for 12 straight years after the dot-com bubble burst, the AMZ had fallen short against the US bellwether benchmark for three in a row. Instead, MLPs posted their worst year of relative performance in the AMZ’s 20-year recorded history.

(2) The AMZ largely delivered on its beta equals one objective, with one caveat.

The index’s price return was -62.3% from peak to trough, outperforming the median of 105 MLPs by 4.6 percentage points. But if you take out the 17 production and mining MLPs, the universe’s median return was -62.5%, virtually identical to the AMZ’s drop.

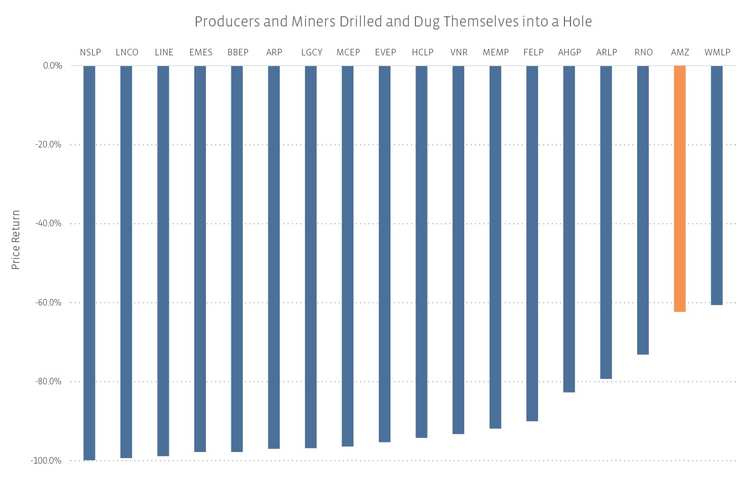

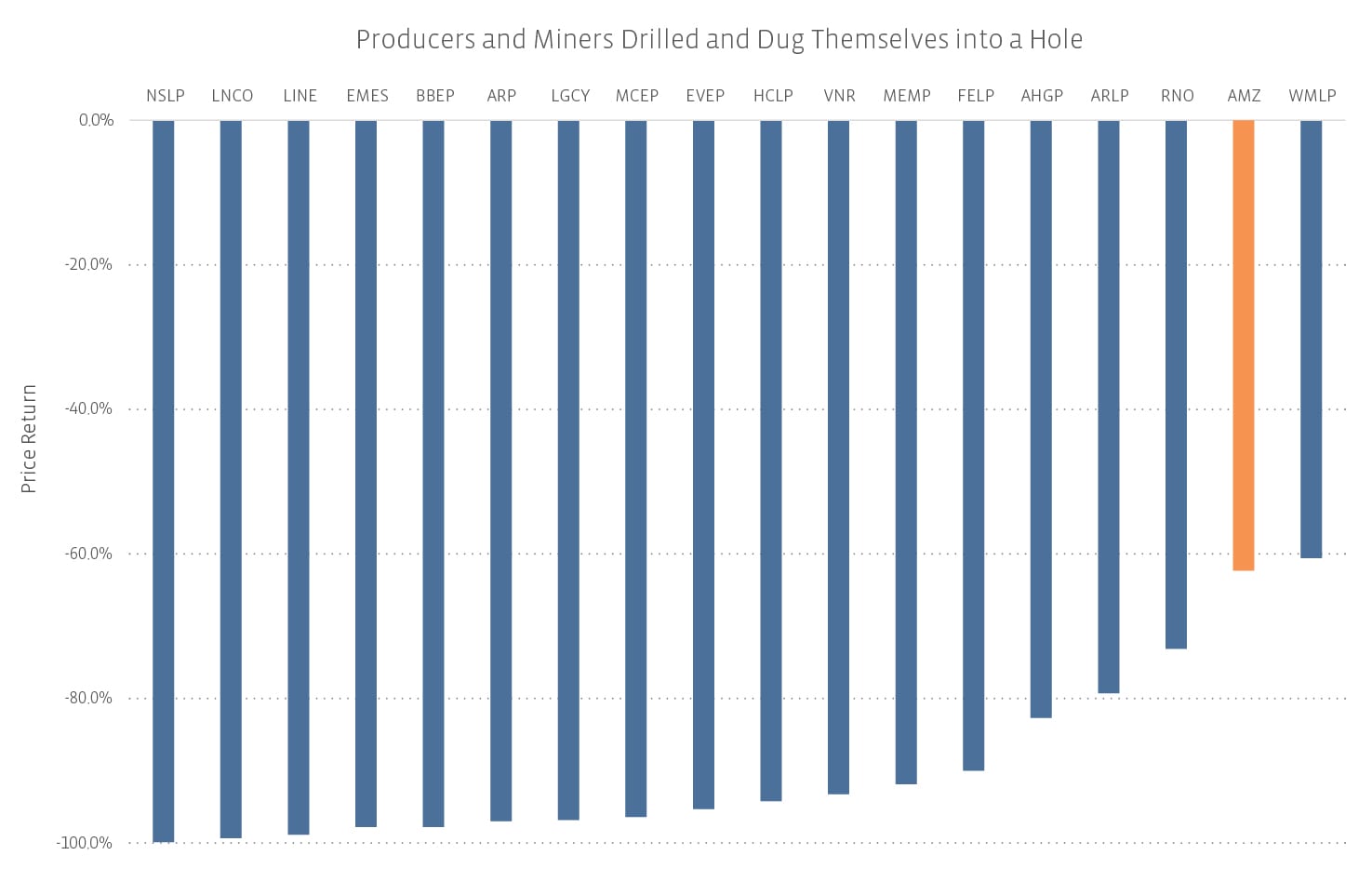

(3) Production and mining: Save Our Ship (or well, or mine).

On that note, breaking news: a business that is directly exposed to commodity prices is going to do poorly when those prices fall. 16 of the 17 production and mining MLPs were in the bottom half of performers during the downturn, and every producer of drill-bit hydrocarbons (DBHs) and both frac sand miners were down at least 90%. Even Alliance Resource Partners (ARLP), which has financed its growth internally for 13 years and had maintained or grown its distribution each quarter since its 1999 IPO, sold off to the tune of 79.3%.

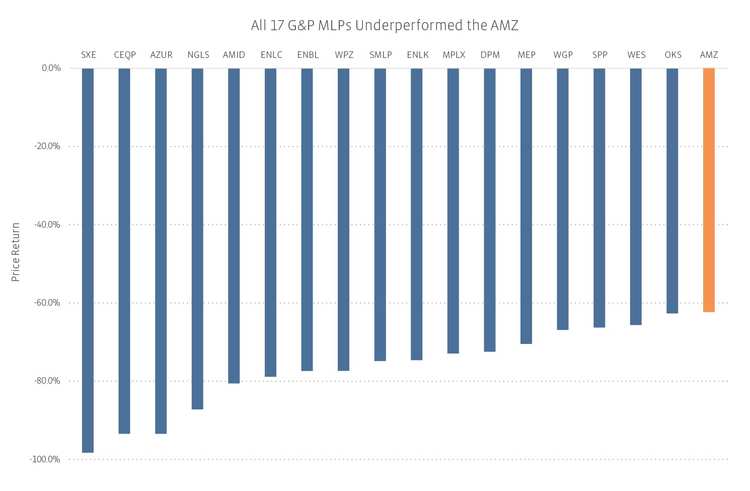

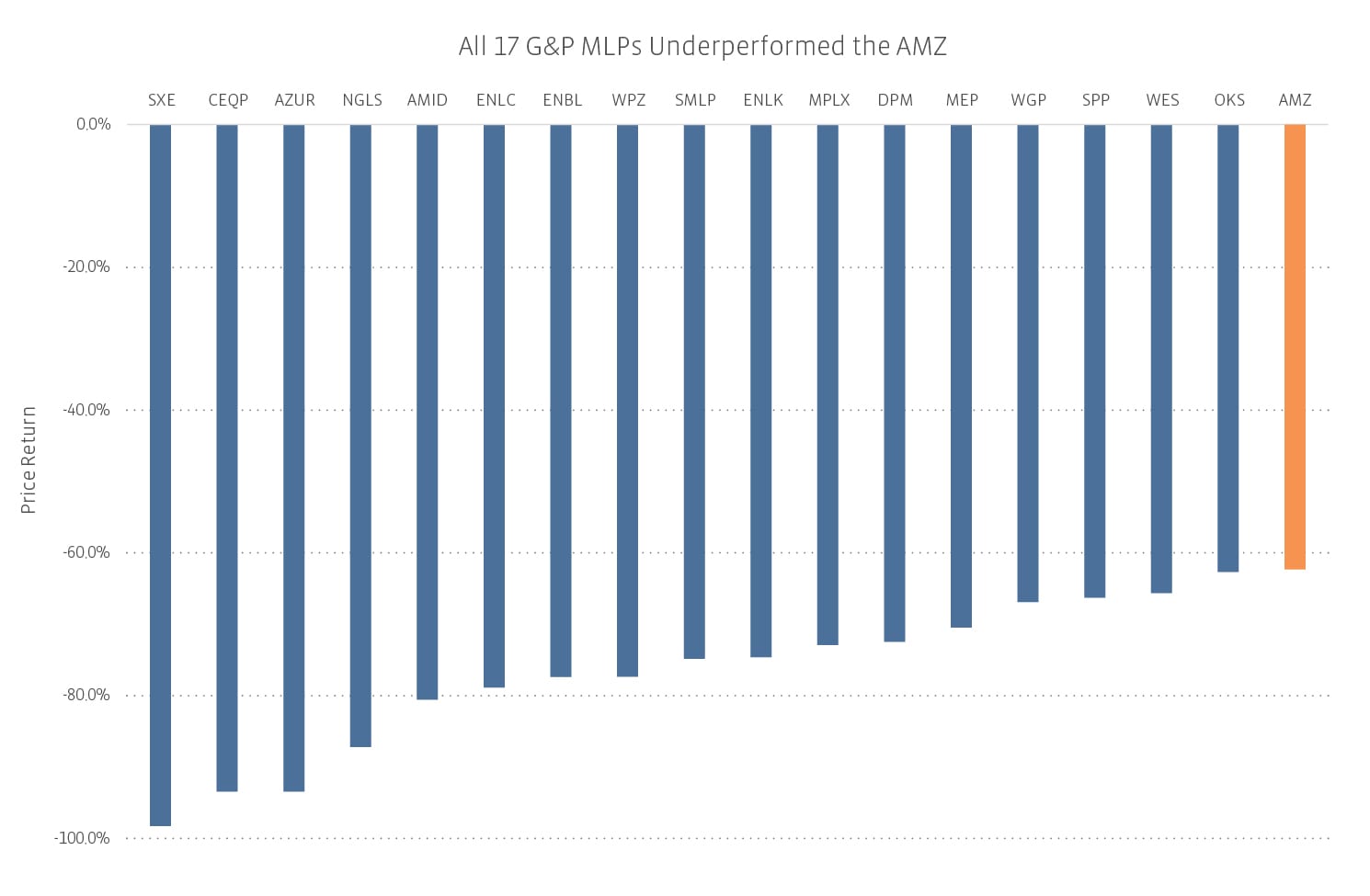

(4) Gathering and processing: closer to upstream = closer to upstream performance.

Fee-based doesn’t mean a whole lot if your volumes are drying up, and minimum volume commitments don’t help if a judge can throw out your service agreement in bankruptcy proceedings. The 17 G&P MLPs had a median return of -74.8%. Three posted returns in the top half of the universe: ONEOK Partners (OKS) at -62.6%, Western Gas Partners (WES) at -65.6%, and Sanchez Production Partners (SPP) at -66.3%. If you use the ex-production and mining median instead, not one G&P MLP was in the 50th percentile or above.

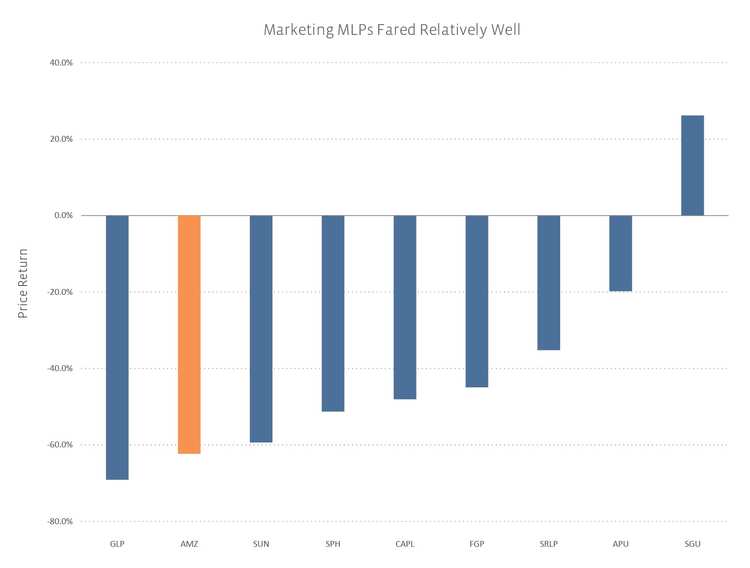

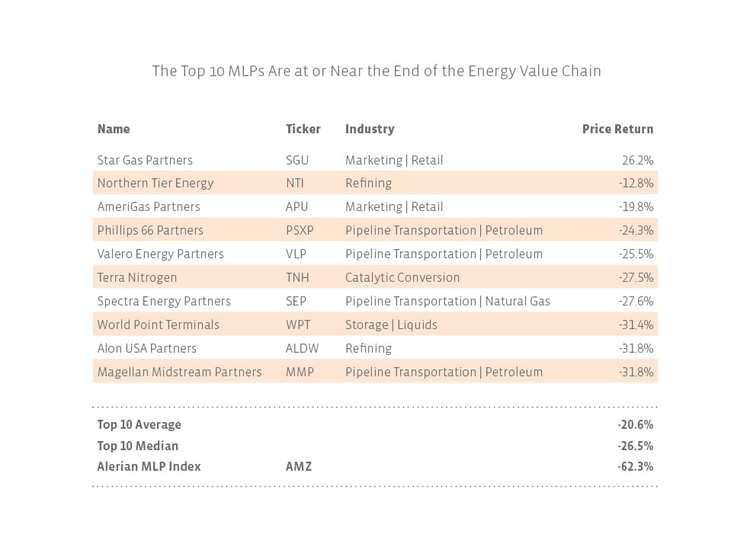

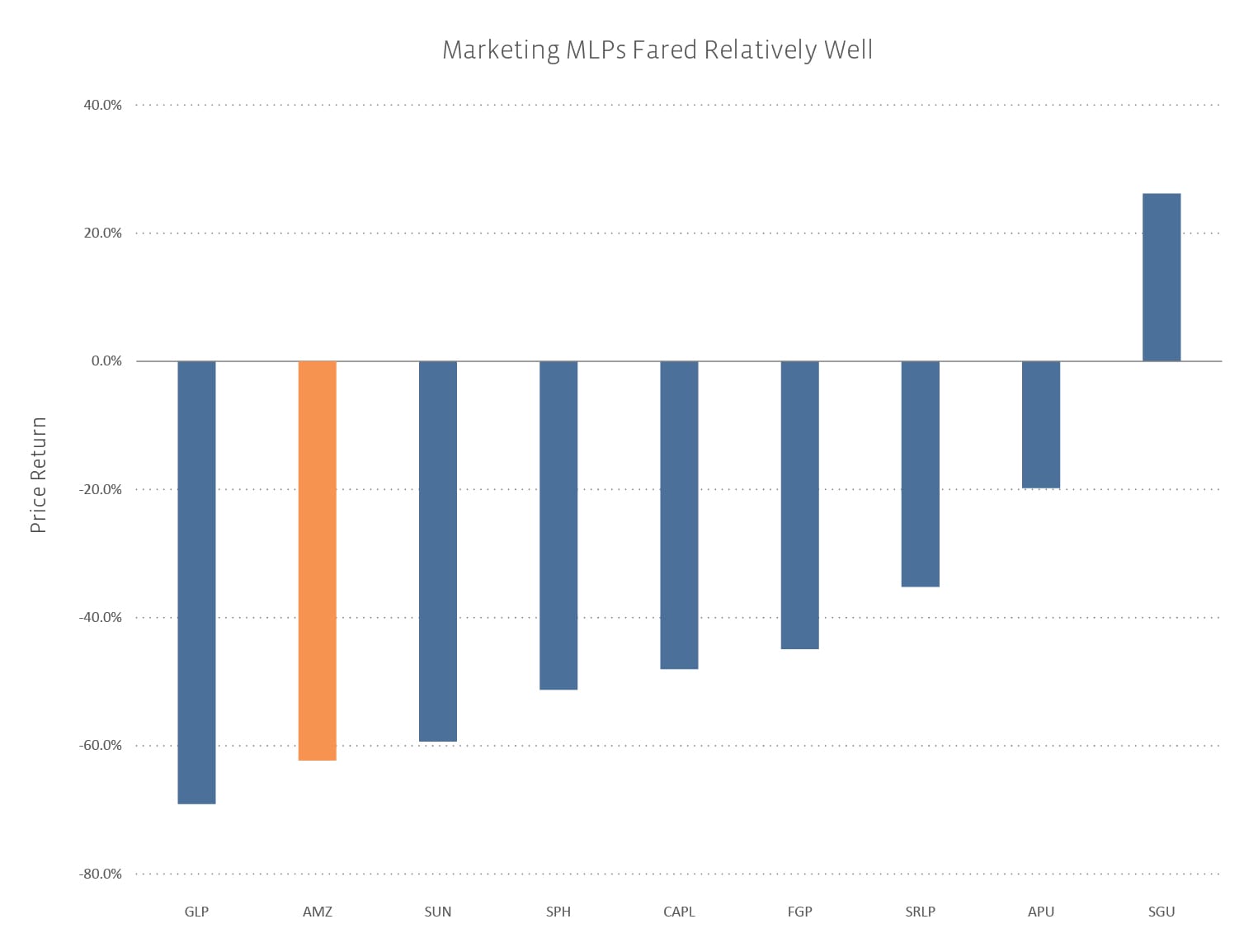

(5) One positive light in an oil and gas well of darkness: Star Gas Partners (SGU).

That’s not a typo. Out of 105 MLPs, only SGU escaped negative territory, returning 26.2%. The next best performer, Northern Tier Energy (NTI), was a whopping 39.0 percentage points behind at -12.8%. Six of the other seven wholesale and retail marketers also held up relatively well, with returns ranging from -59.4% to -19.8%. The lone exception was Global Partners (GLP), which tumbled after cutting its distribution earlier this year.

(6) Boring (pipeline and storage MLPs) was less exciting (outperformed).

The 34 pipeline and storage MLPs had a median price return of -49.6%, well ahead of the overall universe. Only seven names were among the bottom half: Rose Rock Midstream (RRMS) at -88.1%, NGL Energy Partners (NGL) at -86.6%, Energy Transfer Equity (ETE) at -81.8%, Plains GP Holdings (PAGP) at -81.8%, Niska Gas Storage Partners (NKA) at -77.4%, Plains All American Pipeline (PAA) at -74.2%, and NuStar GP Holdings (NSH) at -67.2%. NKA was already distressed before the downturn started. The other six suffered from a combination of crude logistics exposure, high leverage, and external financing needs.

(7) Nice defense from the Fab Five.

The five so-called pure-play refinery logistics dropdown MLPs—Delek Logistics Partners (DKL), PBF Logistics (PBFX), Phillips 66 Partners (PSXP), Valero Energy Partners (VLP), and Western Refining Logistics (WNRL)—all posted returns in the top 25. Tesoro Logistics (TLLP), which muddied its story with a G&P acquisition, was 27th. MPLX (MPLX) did the same but fared much worse, underperforming the AMZ due to continued downward revisions of its distribution growth guidance.

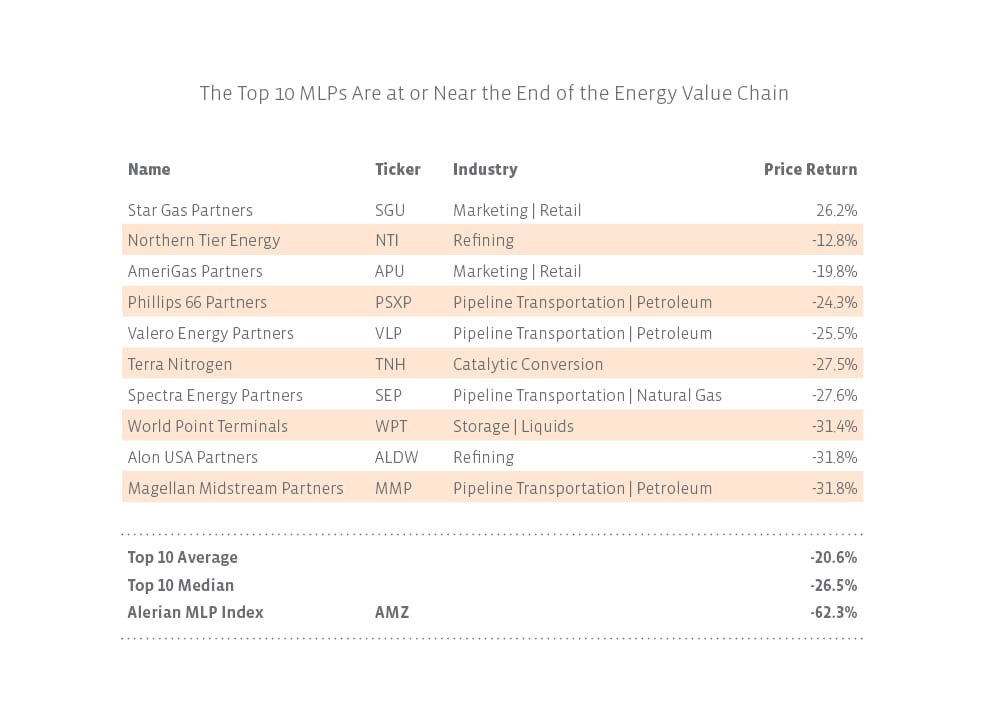

When the problem is with excess supply, demand-pull businesses are better equipped to weather the storm. Rounding out the top 10 alongside the aforementioned SGU, NTI, PSXP, and VLP were companies at or near the end of the energy value chain: AmeriGas Partners (APU), Terra Nitrogen (TNH), Spectra Energy Partners (SEP), World Point Terminals (WPT), Alon USA Partners (ALDW), and Magellan Midstream Partners (MMP).

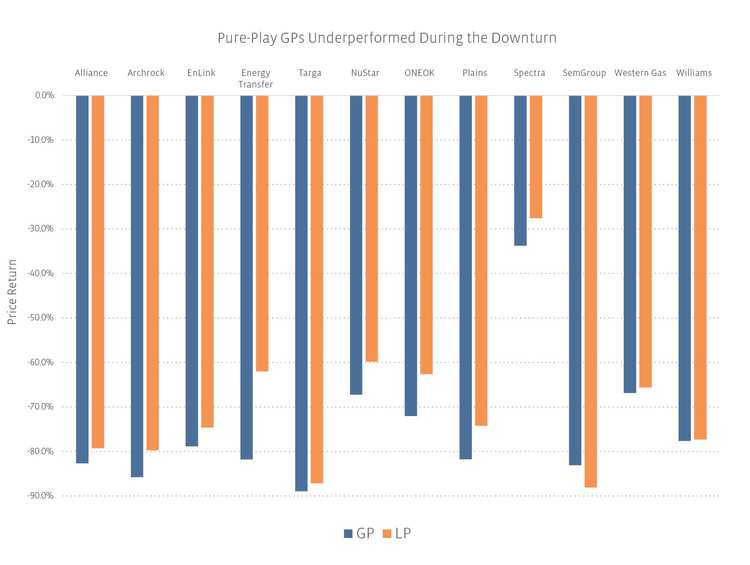

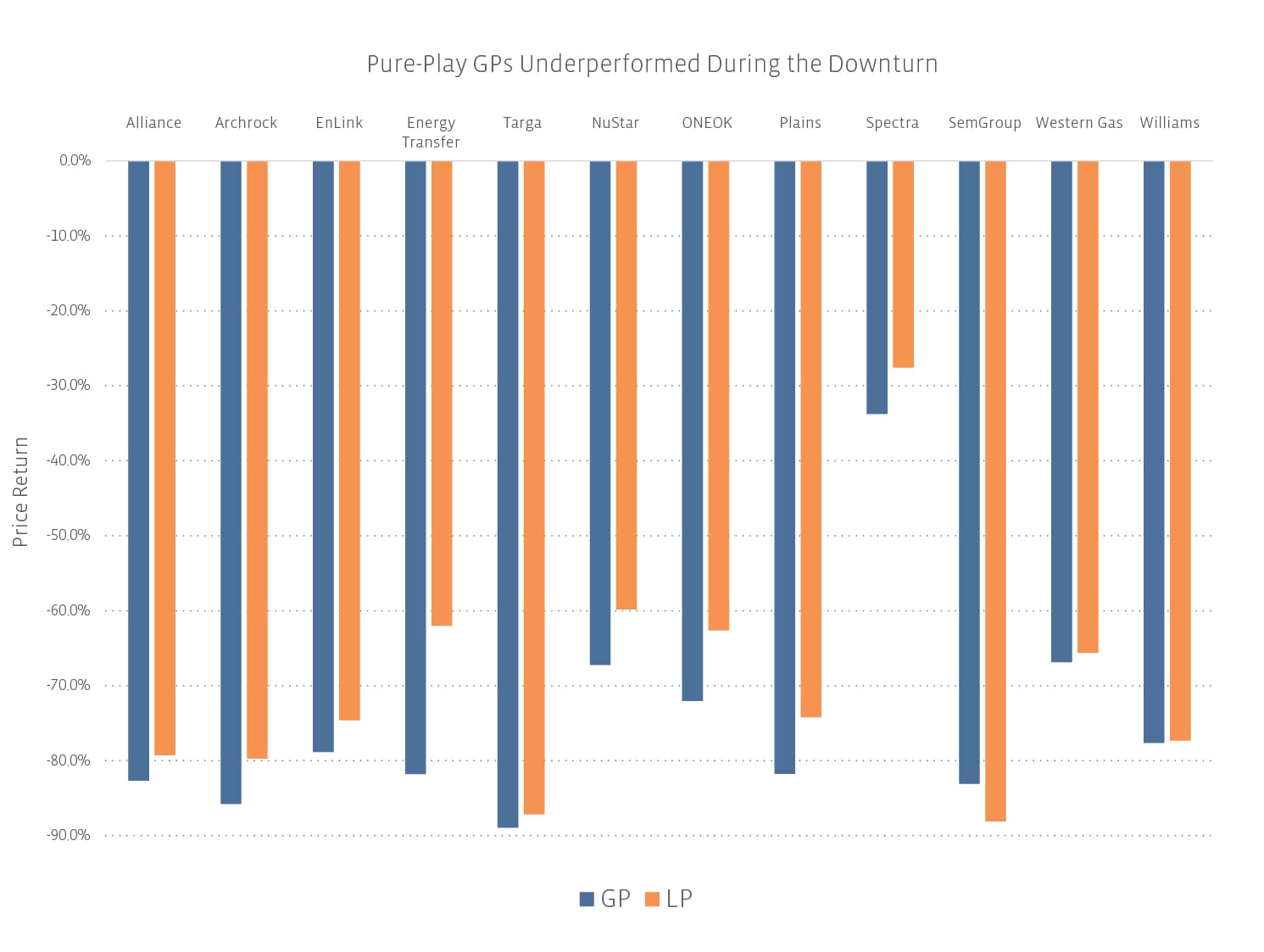

(9) Leverage is leverage, and GPs don’t always win.

The median price return differential between the 13 pure-play GPs and their underlying LPs was 6.1 percentage points in favor of the latter, and none of the GPs outperformed their underlying LPs on a total return basis during the downturn. In theory, GPs should underperform in a selloff because they are a leveraged play on their underlying LPs. Many stakeholders rightly questioned whether that would pan out empirically given the GP’s lack of fiduciary duty to the LP, particularly when M&A is involved, so it’s interesting to see that it did. That said, mid-single-digit underperformance isn’t much considering this was the worst energy bust we’ve seen in the modern MLP era. Many investors accordingly may be willing to take that modest downside risk to invest alongside management, particular as investor sentiment appears to be stabilizing and inching upward.

2016.05.10 12:45pm CST – Edited to correct three instances in the post where relative performance was stated using % rather than percentage points.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}