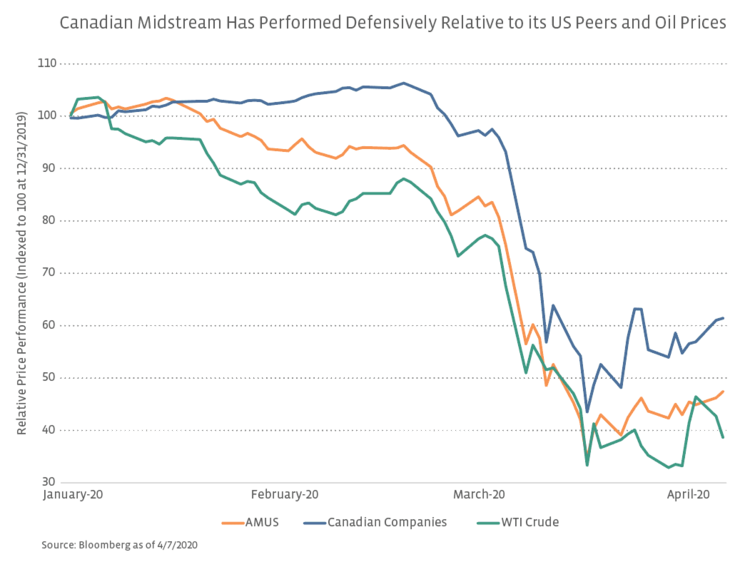

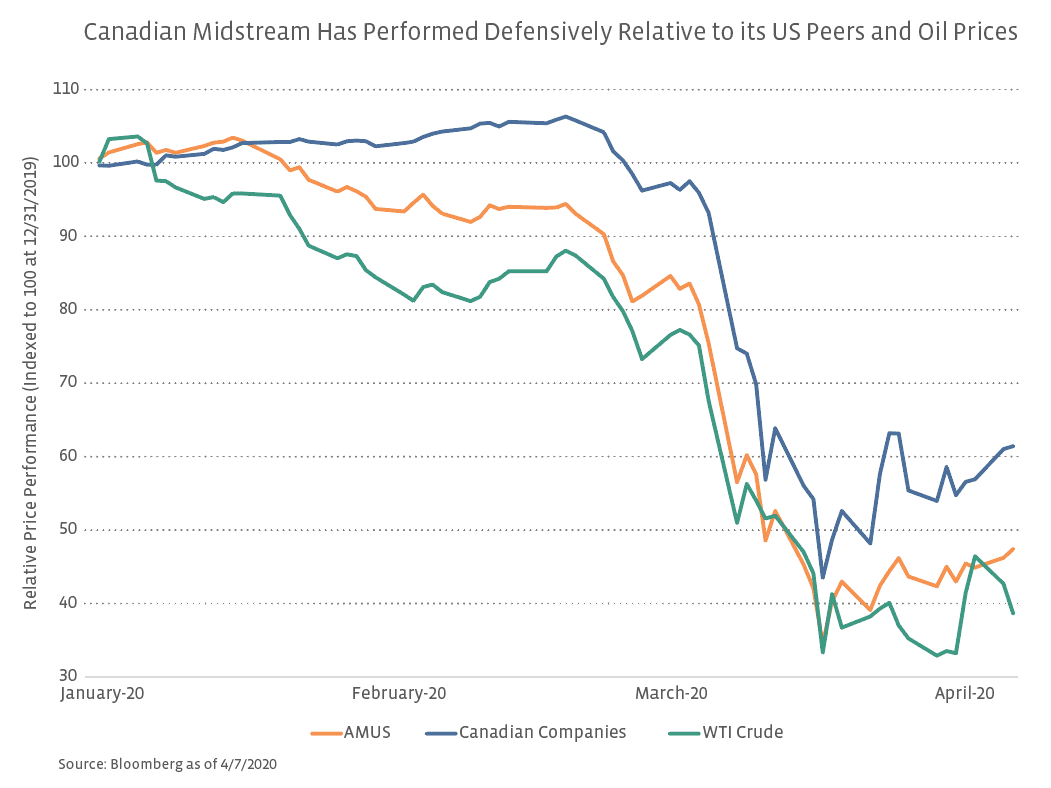

As noted, constructive updates from Canadian companies have also contributed to their more defensive performance. In a recent presentation, ENB reaffirmed 2020 EBITDA guidance, while highlighting its 95% investment grade customer base and 98% fee-based EBITDA exposure. ENB also pointed to the EBITDA growth demonstrated during the financial crisis and 2014-2016 downturn. In mid-March, PPL reiterated 2020 EBITDA guidance, noting that guidance may come in at the low side of the provided range, and reduced expected 2020 capex by 43% at the midpoint. In terms of project updates, TRP announced last week that it will begin the construction of Keystone XL, an 830 thousand barrel per day oil pipeline connecting Alberta to Steele City, Nebraska. Additionally, in support of the project, the Government of Alberta plans to invest $1.1 billion in Keystone XL and will provide TRP with a $4.2 billion project-level credit facility in 2021.

Another significant distinction can be made between Canadian and US midstream companies when it comes to dividends. All the Canadian AMEI constituents continued to grow their dividends during the 2014-2016 downturn, while MLP distribution cuts were prevalent then and subsequently. Earlier this week, PPL announced that it would maintain its April dividend sequentially. Prior to the collapse of oil prices, TRP was guiding to annual dividend growth of 8% to 10% through 2021 and 6% at the midpoint thereafter, and ENB raised its dividend by 9.8% sequentially in 4Q19. The dividend picture isn’t completely rosy, however. IPL reduced its monthly payout by 72% and will use the cash savings to self-fund the remaining equity portion of its Heartland Petrochemical Complex. IPL was the only Canadian name with a yield above 20% in March, peaking at nearly 32%.

Given positive company updates, particularly from larger names, and the defensive characteristics of Canadian midstream equities, these companies are well positioned to continue to outperform in a tough energy environment.

{kind=link}