With inflation debated daily among investment professionals and media reporters, it is virtually impossible to predict interest rate movement or the economic landscape. Given that many retail investors focus on equity investments, choosing a fixed income allocation can be particularly difficult given the lack of accessible tools and models. As interest rates and inflation expectations evolve, a tactical rules-based approach to portfolio optimization can help provide investors with a flexible fixed income allocation in different scenarios.

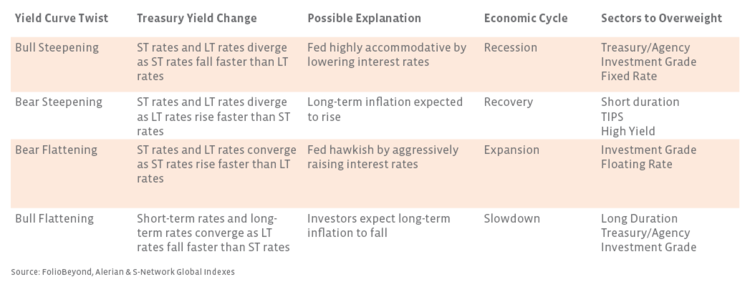

The yield curve can help investors make decisions based on the economic cycle.

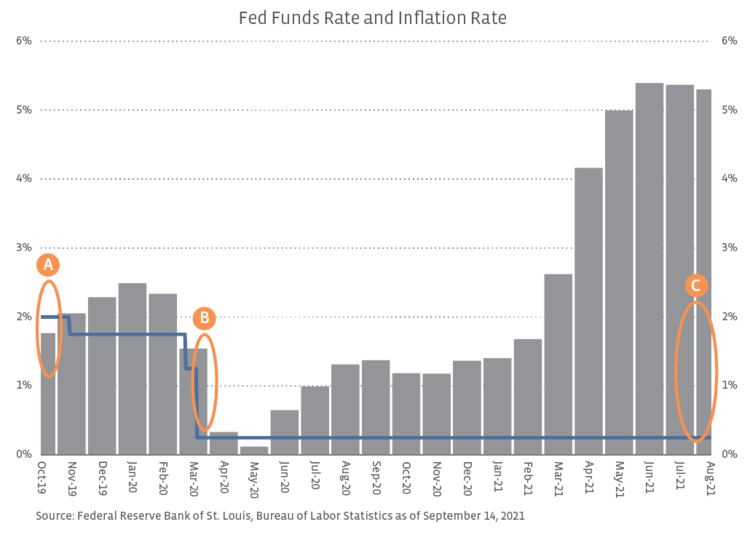

The yield curve is one of the most important concepts for fixed income investors to understand. The short end of the yield curve is anchored by Fed policy when they adjust their short-term target (i.e., Fed funds rate). The long end of the yield curve is partly driven by inflation expectations and economic growth forecasts. Short-term rates and long-term rates can move by different orders of magnitude depending on the phase of the economic cycle, which causes the yield curve to steepen as rates diverge or flatten as rates converge. During a recession, the Fed can lower interest rates to stimulate the economy. This would lead to a bull steepening if long rates don’t come down as quickly. During the recovery part of the economic cycle, long-term inflation expectations usually rise, and the market can experience a bear steepening. During the expansion phase, however, the yield curve may experience a bear flattening when the Fed raises interest rates aggressively as the economy strengthens. Then an ensuing economic slowdown may lead to a bull flattening, where long-term inflation rates are expected to fall.

Different fixed income strategies are appropriate as short-term rates and inflation expectations change.

Three of the more common fixed income characteristics are duration, credit quality, and product/sector type. An investor’s allocation to each of these may depend on the economic cycle and yield curve as discussed above. For example, duration is a measure of interest rate risk. Bond duration is expressed in years, and a bond with a longer duration is more sensitive to rising interest rates. Credit quality is the measure of a bond issuer’s ability to repay its debt. A high yield bond, for instance, has a higher chance of default than an investment grade bond. However, high yield bonds can offer higher coupon payments and are more highly correlated to equities so they may perform better in periods of strong economic growth. Product types include corporate, municipal, agency, and Treasury bonds. Certain products like Treasury Inflation Protected securities (“TIPS”) are indexed to inflation and can help protect a portfolio against rising inflation rates.

A rules-based approach can help investors adjust their fixed income allocations, addressing changing expectations in a rapidly changing environment.

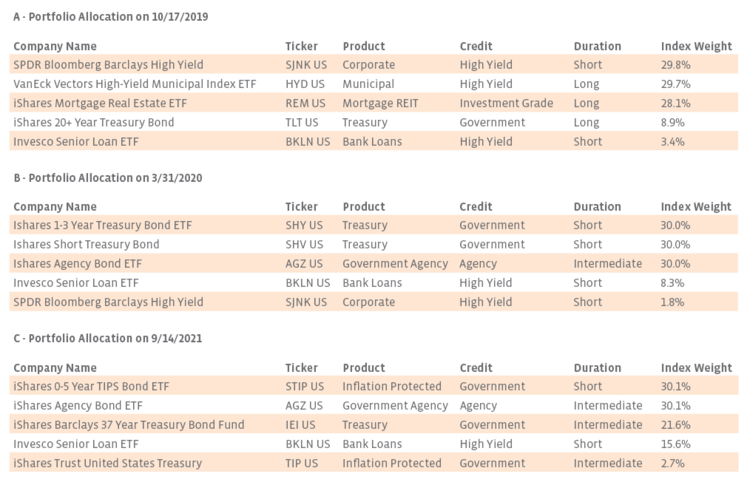

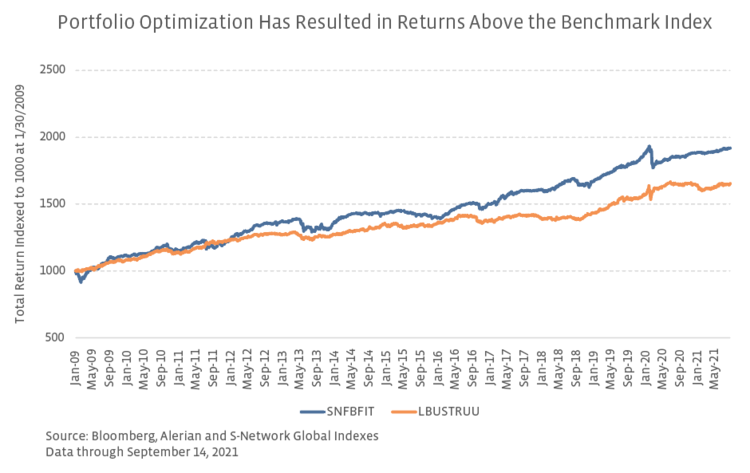

As mentioned above, the fixed income sector fortunately offers a variety of strategies for different scenarios. Unfortunately, without perfect foresight it is impossible in any market to pick just one strategy. There is currently a lot of debate whether interest rates will rise, inflation is “transitory”, or we’re in a market bubble. A rules-based approach to fixed income portfolio optimization takes the “educated” guesswork out of portfolio optimization to address market movements. The S-Network FolioBeyond Optimized Fixed Income Index uses FolioBeyond’s unique factor-based optimization algorithm to optimize portfolio allocations. The base model targets the return volatility of the Bloomberg Barclays U.S. Aggregate Bond Index (also known as Agg, ticker: LBUSTRUU) and optimizes allocations across 23 sector ETFs, subject to maximum allocations to any one sector. Although many other basic models use predominantly backward-looking variables, this model uses forward-looking value measures, momentum effects, correlations, volatility, and stress testing. These value measures are also adjusted for options, defaults, inflation, taxes, and other variables. Historical simulations seen below have shown that the FolioBeyond algorithm has outperformed the Agg. See here for more details on the FolioBeyond Fixed Income Algorithm.

Bottom Line:

A fixed income investment can serve as diversifier against equities, a source of income, or even protection against inflation when using TIPS. Different fixed income strategies can be appropriate during different parts of the economic cycle, but it’s never straightforward what type of fixed income strategy is preferred at each point of the cycle. Investors can benefit from a rules-based approach to portfolio optimization, which can select appropriate portfolio allocations in different risk/return environments, while aiming to outperform the benchmark fixed income index.