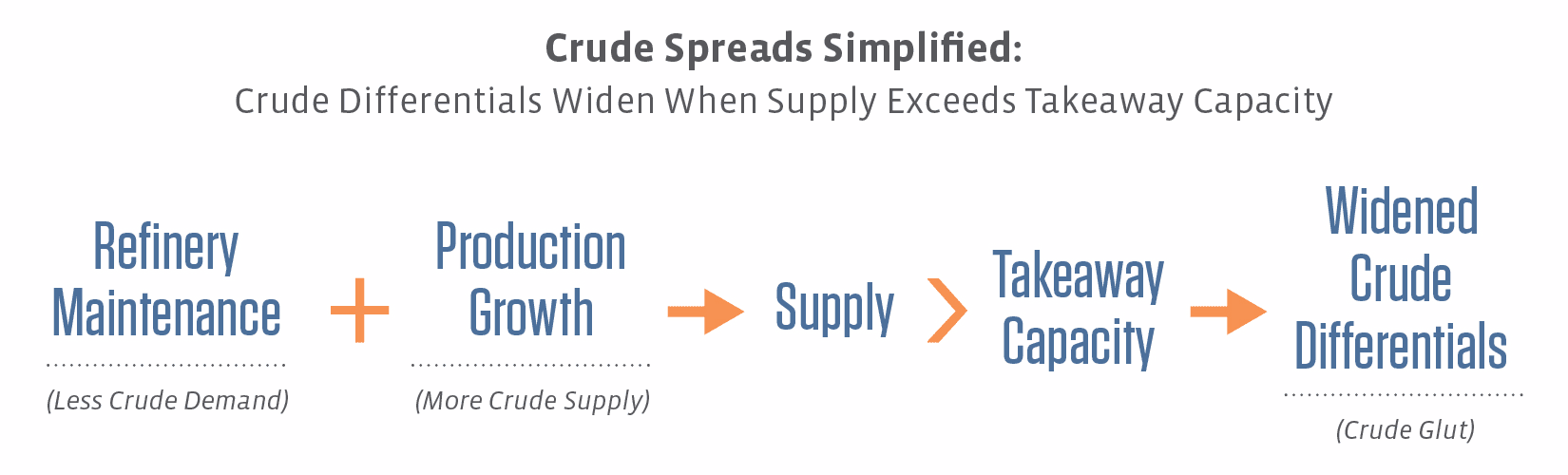

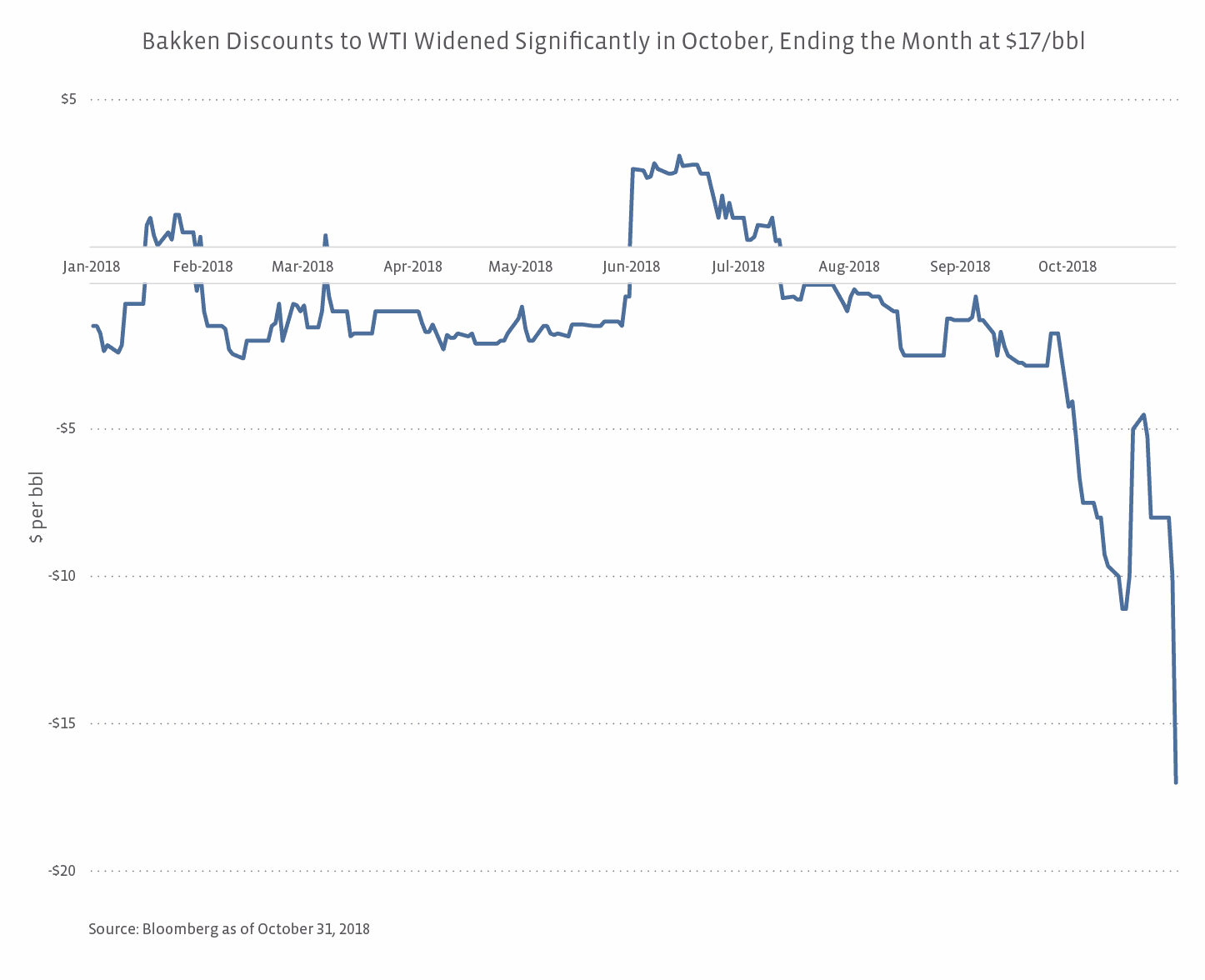

The transient exacerbates the structural in the Bakken.

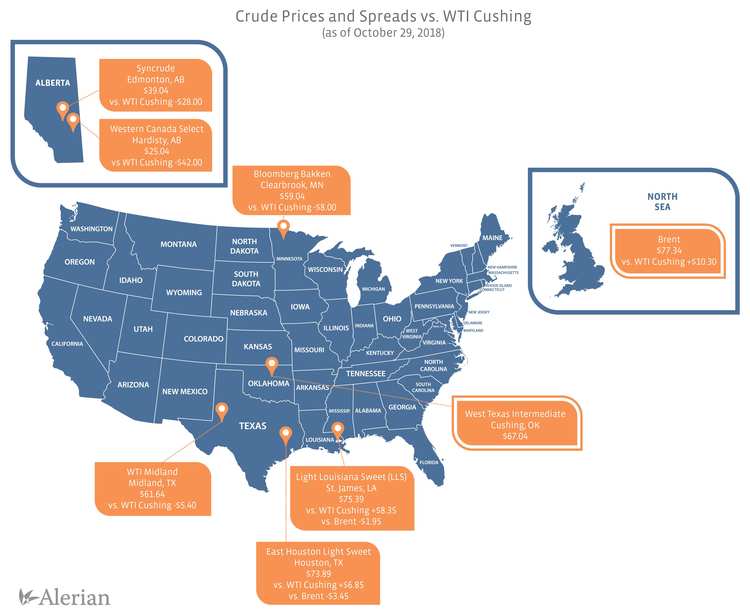

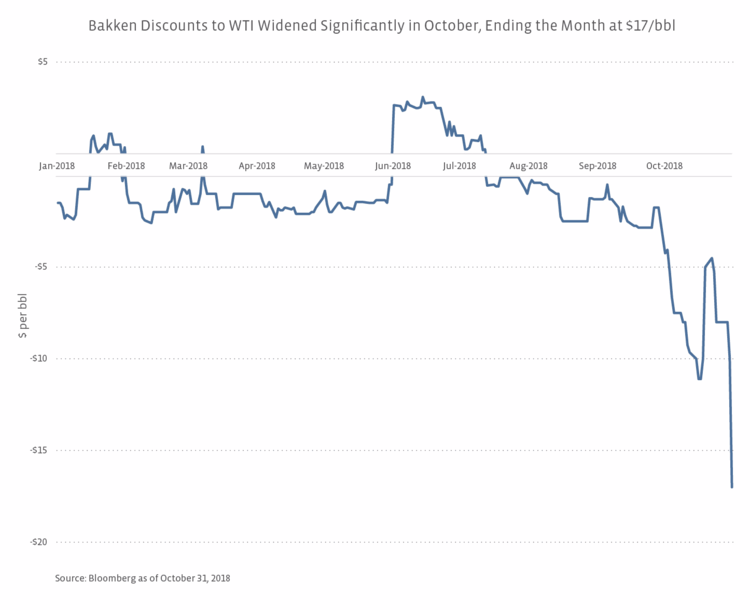

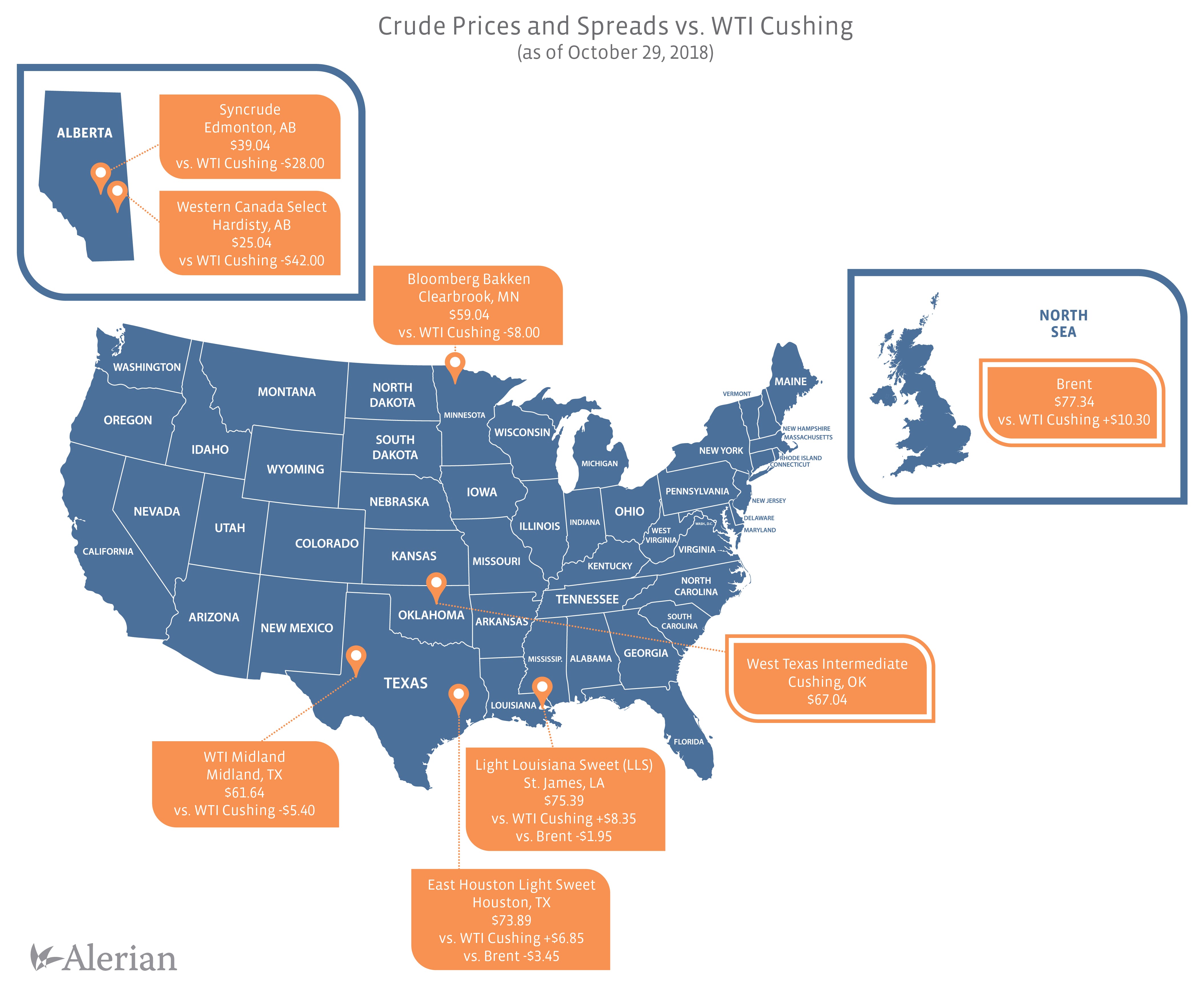

Last year, Bakken crude priced at Clearbrook, Minnesota, traded at a $0.23/bbl premium to WTI Cushing on average. Energy Transfer’s (ET) Bakken Pipeline started operations on June 1, 2017, providing 520 thousand barrels per day (MBpd) of needed takeaway capacity. As shown below, the WTI Cushing – Bakken differential has widened significantly in October to as much as $17/bbl, as PADD II refinery utilization dropped from 96.1% in mid-September to 70.0% in mid-October. While this equated to reduced oil demand of 1 million barrels per day (MMBpd), utilization has since increased, and refining capacity returning from maintenance should help ease the crude oversupply. To be clear, the Bakken Pipeline originates in North Dakota, not Clearbrook, but Marathon Petroleum (MPC) said on its earnings call that the differential at the pipeline’s Beaver Lodge origin point was $14/bbl as of October 31st.

Structurally, however, production growth has also tightened takeaway capacity. Phillips 66 Partners (PSXP), a partner in the Bakken Pipeline, indicated on their recent call that the pipeline was running at 508 Mbpd in 3Q18 (98% capacity), and turnaround activity didn’t begin until the end of the quarter. On October 19, ET announced an open season for its Bakken Pipeline, which is expandable by 50 Mbpd to 570 Mbpd. PSXP’s management noted that the expansion would require minimal to no capital, but any larger expansion would require more significant investment. On the Phillips 66 (PSX) call, management pointed out that production growth has accelerated lately, and they expect Bakken differentials to remain wide. The EIA estimates November production to be up almost 50 Mbpd from August 2018. While rail will help with takeaway, PSX noted that rail cars could be a potential bottleneck. BNSF reportedly told shippers this summer that it was going to ban retrofitted oil tank cars (DOT 117Rs).

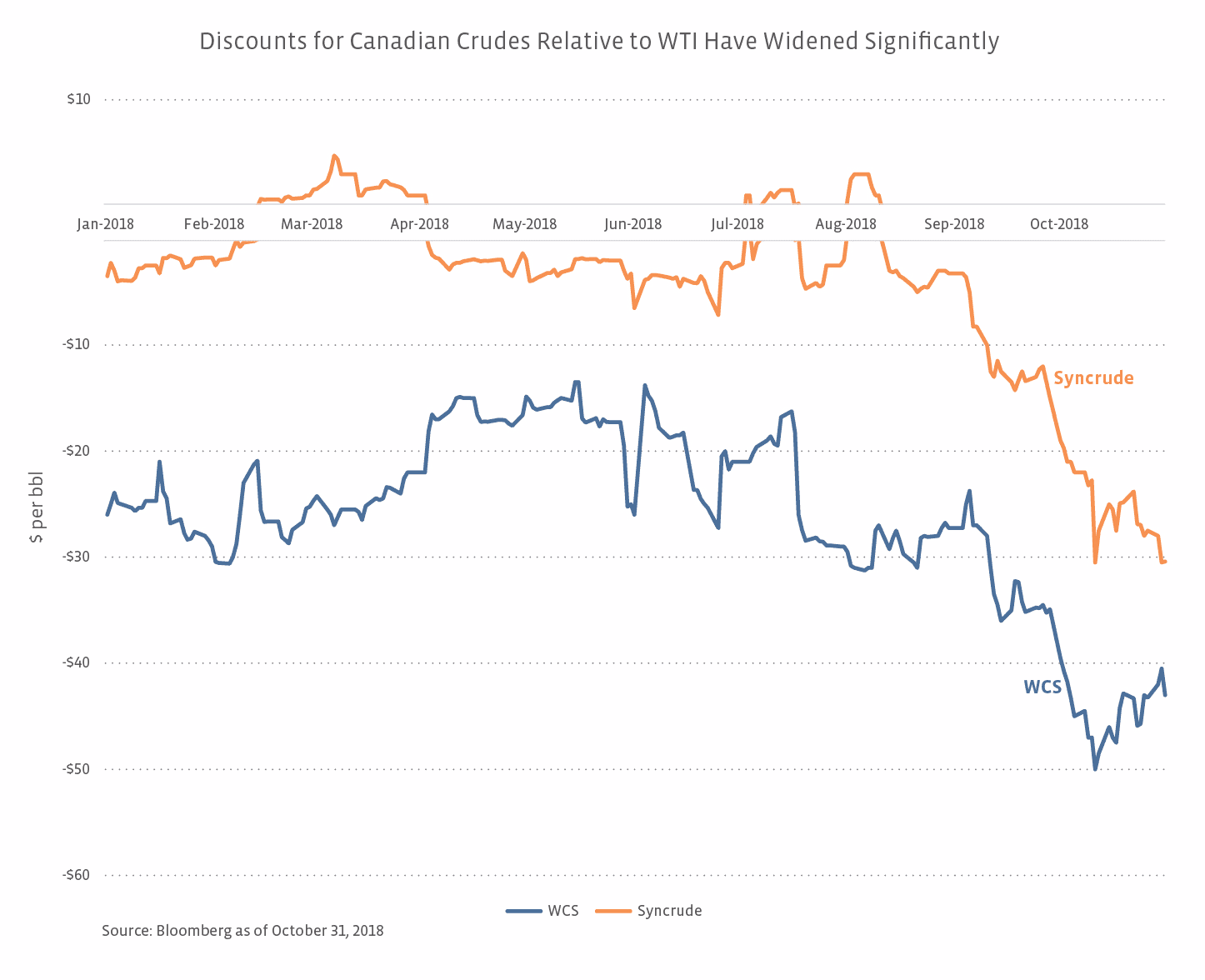

Structural constraints seen persisting in Canada.

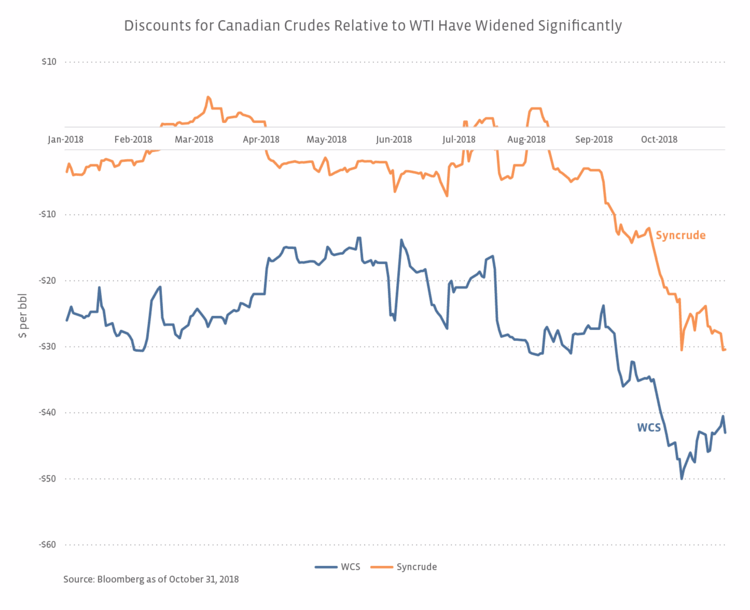

Differentials for Canadian crudes versus WTI Cushing have also blown out considerably, as shown below. Western Canadian Select (WCS) is heavy Canadian crude, and Syncrude is light, sweet crude produced from oil sands. While PADD II refinery maintenance is also contributing to these differentials and increased utilization could provide some relief, Canada has several other issues at hand. On the supply side, the Syncrude oil sands facility is fully back online after a power outage in mid-June interrupted production, which was not fully restored until mid-September. Suncor’s (SU) Fort Hills oil sands project has ramped more quickly than expected, and SU has noted that it has market access for Fort Hills through existing pipelines, presumably displacing other barrels.

Pipeline takeaway remains constrained, with no relief anticipated until Enbridge’s (ENB) Line 3 replacement is completed in 2H19, adding 370 MBpd of takeaway. That leaves rail to fill the gap. Management of HollyFrontier (HFC) indicated on their call last week that rail takeaway from Canada was averaging 225 MBpd and would hopefully increase to 250 MBpd by year-end. Cenovus Energy (CVE) has inked three-year contracts with rail companies to move ~100 MBpd of heavy crude from Alberta to the US Gulf Coast, beginning in 4Q18 with CN (CN) and 2Q19 with CP (CP), with volumes ramping through 2019. CVE also announced last week that it would trim part of its production until prices improved. An added wrinkle may be that Transport Canada (i.e. Canada’s equivalent to the Department of Transportation) has pushed forward the removal of certain unjacketed rail cars (CPC 1232) from crude service in Canada to November 1, 2018 from April 1, 2020.

As structural issues in the Permian are alleviated in 2019, what does it mean for midstream?

As we discussed a few weeks ago, Permian crude differentials are expected to narrow in late 2019 as pipeline capacity comes online. Differentials have already narrowed relative to levels seen in August. Narrowed crude differentials will not necessarily mean growth opportunities for crude pipelines have ended. Enterprise Products Partners (EPD) made it clear on their earnings call last week that people should not assume that they are done building pipelines out of the Permian. Management believes the Permian offers substantial upside. As an example, PSXP recently increased the capacity of the Gray Oak Pipeline (currently being constructed) from 800 to 900 MBpd.

We are already hearing concerns that the Permian will have too much pipeline capacity once the proposed projects are built. Often, production and pipeline takeaway capacity will not perfectly align but fluctuate between oversupply and undersupply. The reassurance we can provide to midstream investors is that midstream companies don’t build projects and hope they will have customers once completed. Rather, they will proceed with projects when firm, long-term commitments are in place that provide visibility to cash flows and project returns. This should help avoid scenarios with underutilized pipelines, though re-contracting can become a risk once initial long-term commitments expire.

Another common concern is that once the Permian bottleneck is alleviated then the next bottleneck will become inadequate export capacity from the Texas Gulf Coast. Time will tell, but relative to the Permian or Bakken, a crude glut on the Gulf Coast has the advantage of significant nearby refining capacity. The limiting factor will be the ability of complex Gulf Coast refiners (geared to run heavy crude) to process incremental light, sweet crude. For midstream, export bottlenecks would be opportunities to build or expand export facilities to ship crude overseas.

Bottom Line

Refinery turnaround season, particularly in the Mid-Continent of the US, has likely exacerbated already tight crude pipeline takeaway capacity in Canada and the Bakken. For midstream companies, the number of crude price blowouts is tangible evidence of the need for infrastructure. As pipeline capacity is added in places like the Permian or Bakken, differentials will narrow again, but that doesn’t mean pipeline growth opportunities have vanished. Keep in mind the average differential between WTI Cushing and WTI Midland was just $0.20/bbl for 2015-2017. If the past couple years are any indication, it will just be a matter of waiting for production to catch up to takeaway.

{kind=link}

{kind=link}

{kind=link}

{kind=link}