Maybe next year.

Now, before we start talking about the CSI Compressco (CCLP) analyst day (slides available here), we have to talk about compression. Most MLP and energy infrastructure investors first became aware of compression as an integral part of the energy value chain in 2006, when Exterran Partners (EXLP), then known as Universal Compression Partners (former ticker: UCLP), was taken public by its C Corp sponsor. These large (and loud) units provide the necessary compression to keep natural gas pipelines pressurized so that product continues to flow.

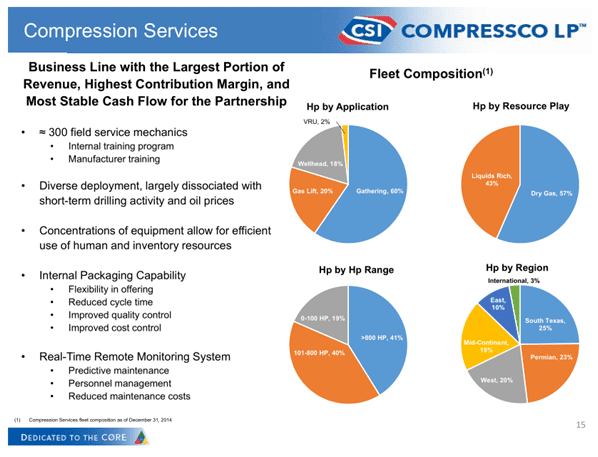

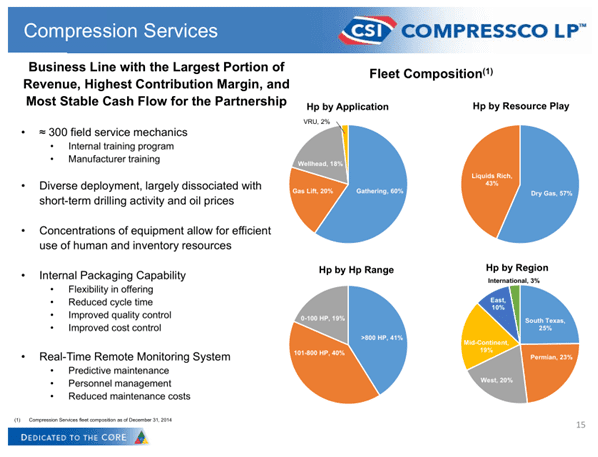

But now there are other kinds of compression units in the MLP structure. CCLP owns and operates:

- Gathering compression, which increases the pressure in small diameter pipelines.

- Gas lift, which is the cleverest kind of compression (to my mind). It involves injecting natural gas into a horizontal well to increase oil and liquids recovery, and is the exact same mechanism a coffee percolator uses to brew coffee. In a percolator, the rising steam forces the water up the center tube and over the coffee grounds. In gas lift, the injected natural gas comes back to the surface, bringing oil or natural gas liquids (NGLs) along with it.

- Wellhead compression, which lower the pressure at the wellhead to increase the flow of natural gas through the use of negative pressure.

- Vapor Recovery Units (VRUs), which capture the vapors associated with storage tanks. VRUs are the smallest part of CCLP’s compression services business.

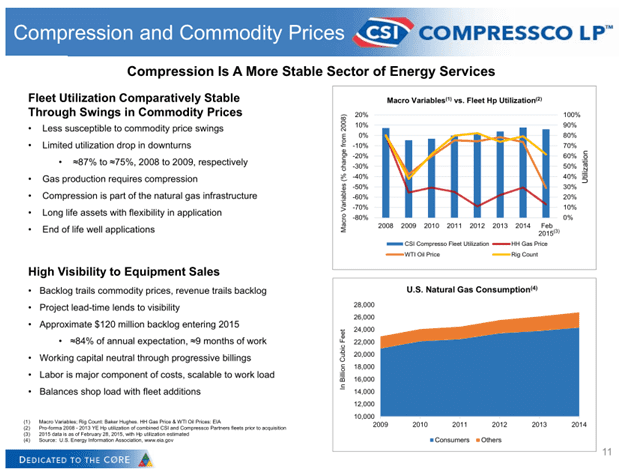

As regular readers of Alerian Insights know, the closer a company or business is to the wellhead, the more sensitive that company generally will be to commodity prices. CCLP is involved primarily with natural gas wells. Despite being closer to the wellhead and falling natural gas prices, the company has posted a 53% YTD total return. On the surface, the stock appears highly correlated to oil prices, given its shellacking during the second half of 2014 as crude tumbled. But digging deeper, it was more likely a case of overly pessimistic expectations. Investors have slowly come back to the stock as the board continues to approve quarterly distribution increases and fleet utilization remains fairly constant. CCLP remains partially insulated from natural gas prices as their near-term fleet utilization is dependent on existing wells, not future drilling.

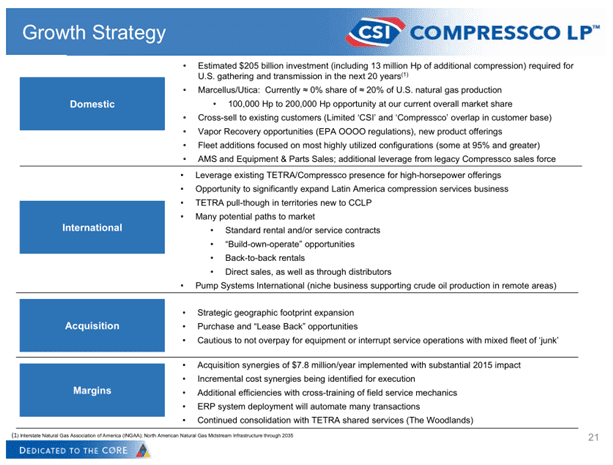

The market nearly always trades on future expectations, and management outlined its growth strategies for CCLP. Two notable opportunities include expansion into the Marcellus/Utica and a leaseback program. Given that the Marcellus is the big new play in America for natural gas and that CCLP currently has no assets there, it could present a large opportunity, but also a significant risk to future growth should CCLP fail to gain a foothold there. The leaseback program is particularly smart given their customer’s need for capital in the current commodity environment. CCLP will buy back the compression units that have been recently sold, and then lease them to the customer instead.

Given the recently released IRS proposed regulations on qualifying income and the fact that compression is not a typical down-the-middle midstream asset, it’s worth noting that the proposed regulations permit activities considered intrinsic to a qualifying activity. While I am certainly no tax expert, I did a little digging through the regulations and CCLP SEC filings. To be an intrinsic activity, three tests must be passed:

- The activity must be specialized to the qualifying activity.

- It must be essential to the qualifying activity.

- It must provide significant services.

Given that CCLP’s compressor units are frequently sold in custom packages, that natural gas cannot flow to the processing facility without compression, and that considerable compression is necessary throughout the value chain, it appears as if CCLP’s activities will continue to generate qualifying income. However, CCLP has not requested a PLR from the IRS and has no plans to do so. Should compression no longer qualify, there is no guarantee that CCLP would be able to remain an MLP during the transition period.

A compression name like CCLP is not what springs to mind for most MLP investors who traditionally prefer large-cap, stable, predictable names. There is more risk involved in a name that is smaller, closer to the wellhead, less geographically diverse, and has shorter duration contracts. In markets that are even moderately efficient, risk is balanced with potential rewards. CCLP does have a sponsor from which it can acquire potential dropdowns, a 10% yield, and a management team with an eye toward growth. Plus, the smaller size of CCLP means growth will be more meaningful on a relative basis.

{kind=link}

{kind=link}

{kind=link}

{kind=link}