Summary //

- While the potential for generous, tax-advantaged income from MLPs is appealing, it does not come without a little complexity.

- For investors not interested in owning MLPs directly because of the associated K-1 or for other reasons, there are over 70 MLP investment products like ETFs, ETNs, mutual funds, and closed-end funds that provide access to the MLP space with a Form 1099.

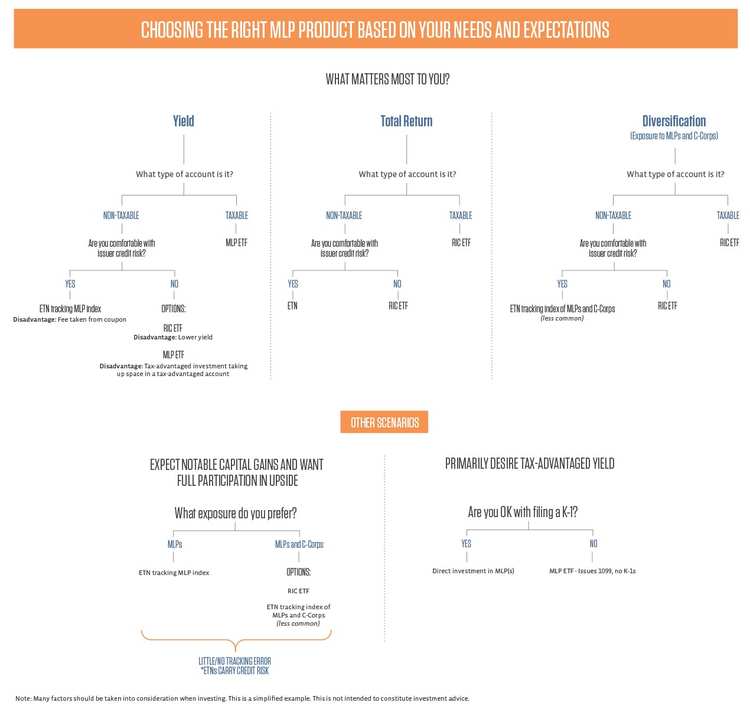

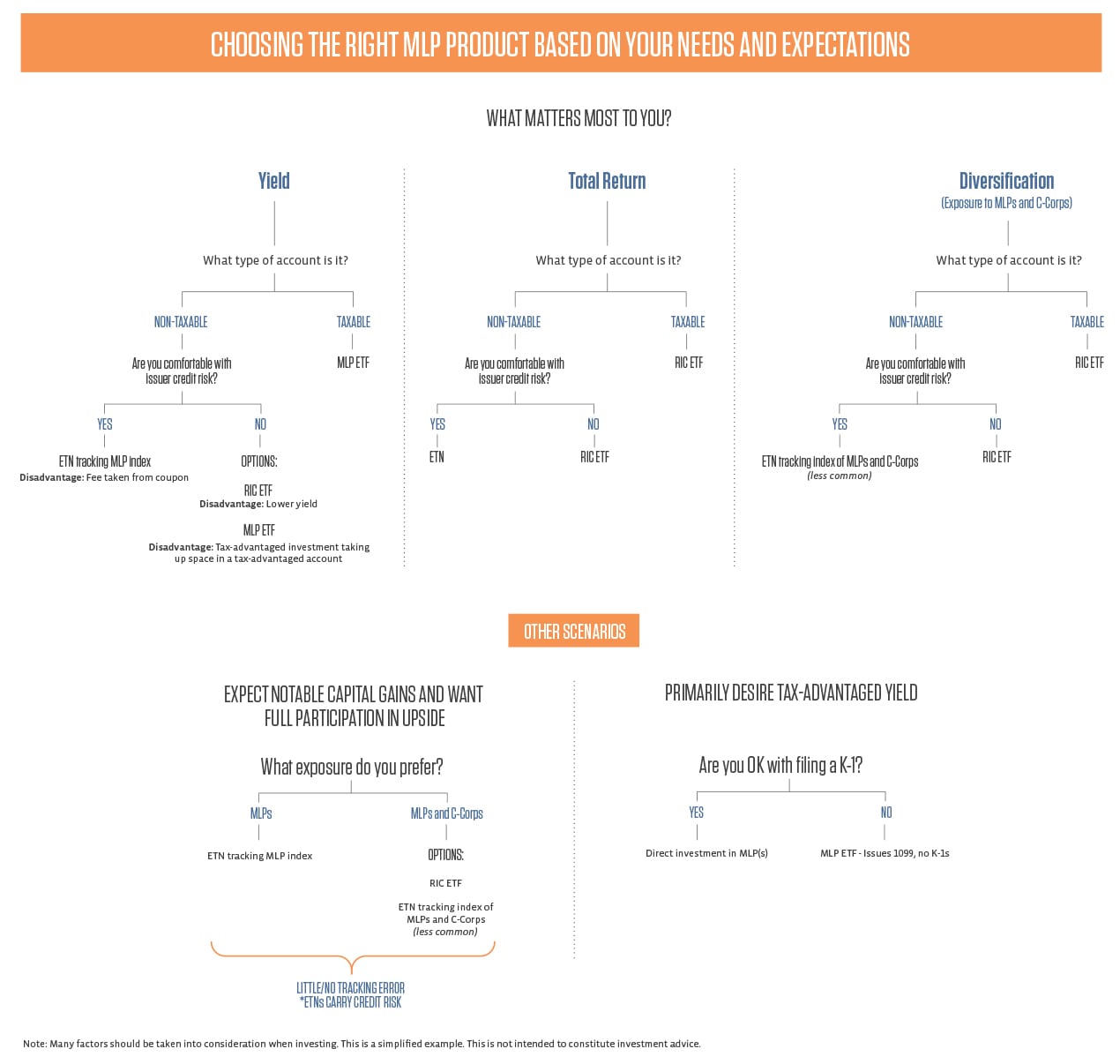

- Given the nuances of different MLP investment products, the simplified decision tree included below attempts to streamline the investment options based on an investor’s needs or expectations and the type of account.

With interest rates near historic lows and energy equities also depressed after oil’s rout, financial advisors and investors looking for income and value may be taking a fresh look at the MLP and energy infrastructure space. While the potential for generous, tax-advantaged income from MLPs is appealing, it does not come without a little complexity. For new investors and even seasoned midstream investors, today’s piece provides a helpful overview of the nuances of MLP investing, including commentary around direct MLP investing and the different types of MLP products like exchange-traded funds (ETFs) and exchange-traded notes (ETNs). For more information and detail, there is a list of relevant resources at the end of this piece. Alerian is not an investment advisor, and this piece does not constitute investment advice (please see our disclaimers for more information).

Direct investment in MLPs.

MLPs pay no taxes at the entity level, and as pass-throughs, they avoid the double taxation associated with investments in C-Corps. MLP units trade on stock exchanges like corporate stock shares, but investors in MLPs will receive a Schedule K-1 each year for tax purposes. The K-1 details the investor’s portion of income, losses, gains, and deductions from the MLP that the investor will need to report when filing taxes. Additionally, MLP investors may be required to pay state income taxes in each state where the MLP operates; however, unless the ownership position is large, the investor’s share of state-level income may not meet minimums for filing a return at the state level.

While the K-1 adds complexity, the advantage of investing in MLPs is that typically 70-100% of MLP distributions (dividends) are considered a tax-deferred return of capital, with the remaining portion taxed at ordinary income rates in the current year. Distributions lower the investor’s basis in the units. As long as an investor’s adjusted basis is above zero, taxes on the return of capital portion of the distribution are deferred until the units are sold. For more detail and an example, please see this note from November 2019.

In our conversations, there seems to be a bifurcated view on K-1s. Some investors don’t mind them, and others see them as a headache. These opinions may depend on how individuals prepare their taxes or how much their accountant charges for handling K-1s. Regardless, for a US taxable investor that is comfortable filing K-1s and state taxes (if required) and building a diversified portfolio, he or she will always be better off buying individual MLPs directly as it is the most tax-efficient way to own MLPs. For clarity, a taxable investor means someone investing in a taxable account (not an IRA or 401-K, for example). Direct investment in MLPs in a tax-advantaged account could lead to Unrelated Business Income Tax (read more). While some investors prefer to directly own individual MLPs, others choose to access the MLP space through a product like an ETF, ETN, closed-end fund or mutual fund to avoid a K-1 and single security risk. The rest of this note explores MLP investment products and the pros and cons of the different options. For a discussion of how energy infrastructure fits into portfolios, please see our white paper from August 2019.

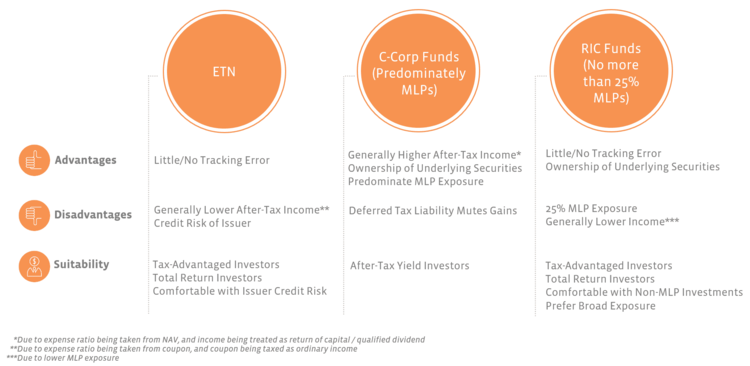

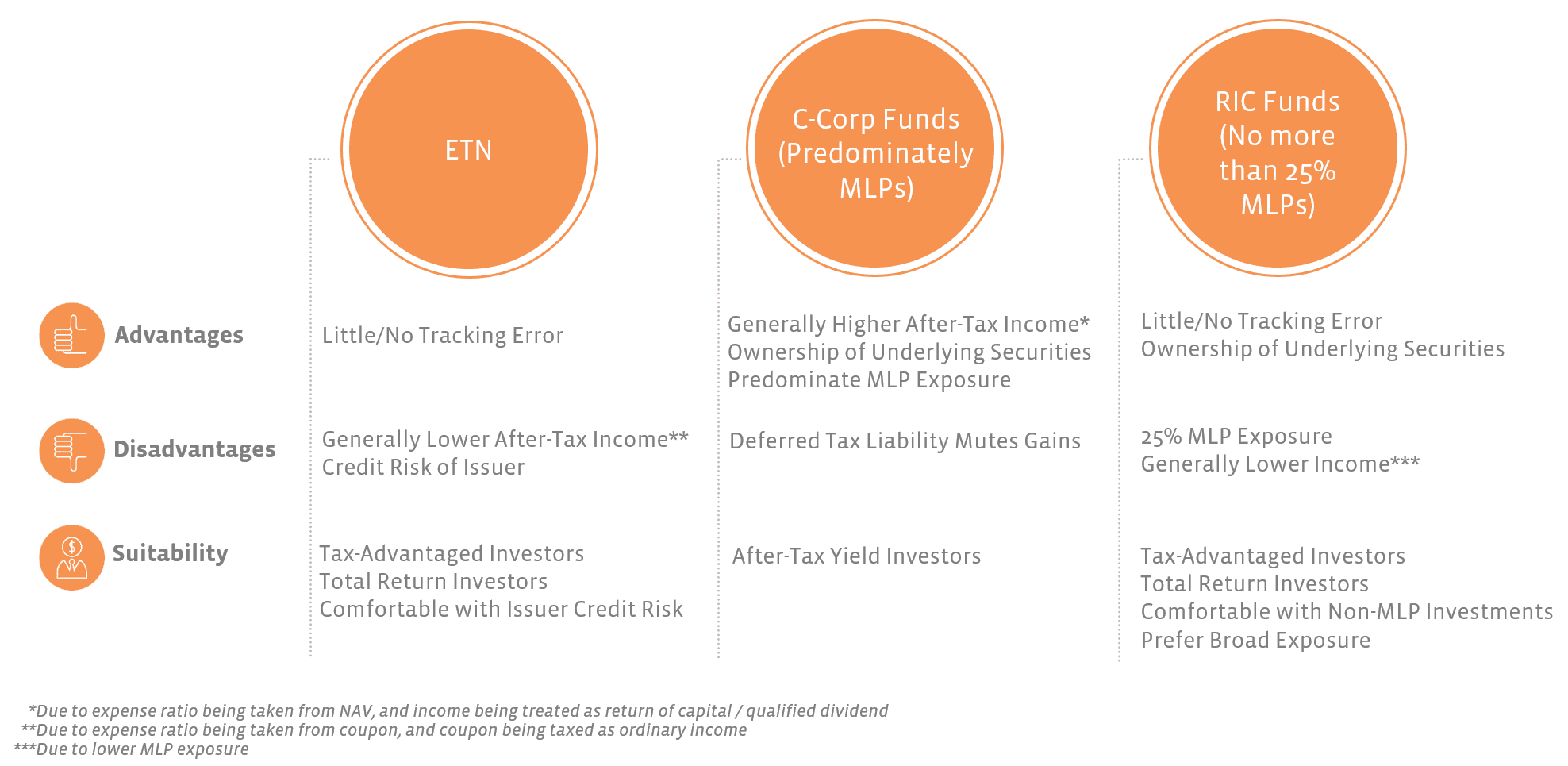

There are two main types of MLP funds: C-Corps and RICs.

For investors not interested in owning MLPs directly, there are over 70 investment products like ETFs, ETNs, mutual funds, and closed-end funds that provide diversified exposure to the MLP space with a Form 1099 and no K-1. These products come with their own structural nuances. Most investment funds are structured as Regulated Investment Companies (RICs), which function as pass throughs and avoid taxes at the fund level. RICs cannot own more than 25% MLPs. To frame it another way, if any fund (mutual fund, closed-end fund, or ETF, whether active or passive) owns more than 25% MLPs, then the fund will be taxed as a corporation. In the energy infrastructure space, funds will typically either own a majority of MLPs (80-100%) and be taxed as a corporation at the fund level or own 20-25% MLPs and be structured as a RIC.

While it may seem that a C-Corp fund would be less desirable than a RIC given fund-level taxation for the C-Corp fund, there are benefits to each fund type, and the suitability of each fund depends on the investor’s needs (see the decision tree below). For example, a C-Corp fund holding mostly MLPs will offer a higher and more tax-advantaged yield than a RIC. Distributions from the fund retain the tax character of the distributions received from its holdings, so a fund owning predominately MLPs is more likely to provide tax-deferred return of capital distributions. MLPs also tend to offer higher yields than C-Corps given the lack of entity-level taxation. While one cannot directly invest in an index, this can be seen in the yield difference between the Alerian MLP Infrastructure Index (AMZI), which consists of MLPs, and the Alerian Midstream Energy Select Index (AMEI), which limits MLPs to 25%. As of May 29, the AMZI’s yield was 10.7% compared to 7.9% for the AMEI, and for the last five years, the AMZI has had an average yield advantage of 224 basis points over the AMEI. While a C-Corp fund will typically provide a higher and more tax-advantaged yield than a RIC, a C-Corp fund could experience tax drag as its underlying holdings gain due to the fund-level taxation (read more).

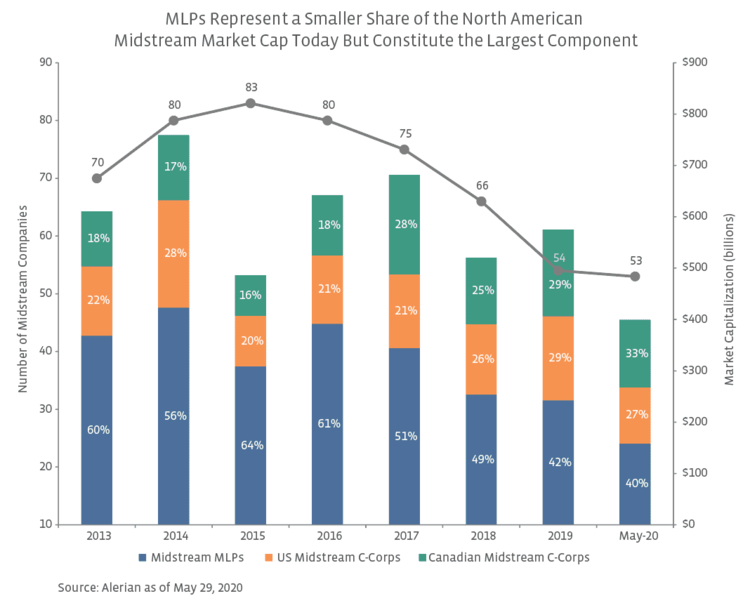

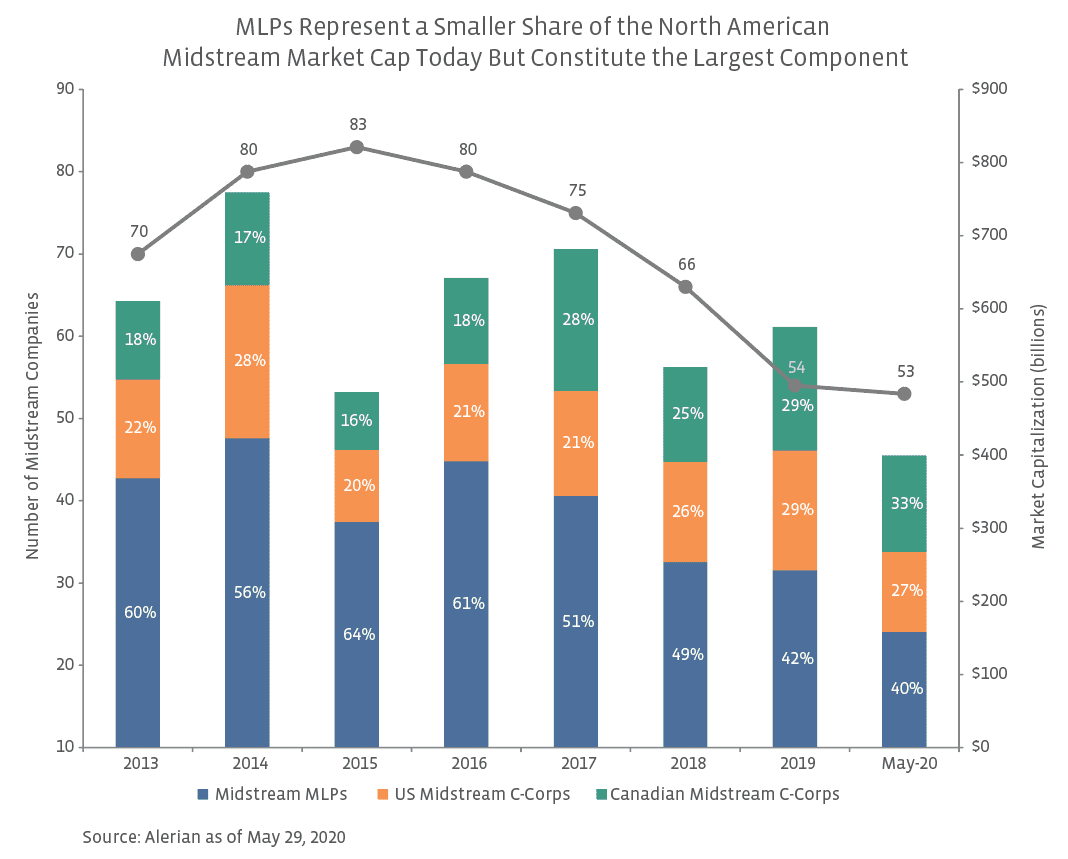

Of course, yield is not the only consideration when investing in the MLP and energy infrastructure space. Investors may be more concerned with total return and diversification than tax-advantaged yield. In those cases, a RIC is likely to be more suitable than a C-Corp fund owning mostly MLPs. A RIC can also offer attractive income compared to other income-oriented investments. However, investors should be careful that the 75% of a RIC not invested in MLPs provides the desired exposure. An energy infrastructure RIC will be more representative of the broader midstream universe given the inclusion of C-Corps, but the 25% limit on MLPs will lead to a greater C-Corp weighting and lower MLP weighting than what would be implied by the universe market capitalization. To explain further, MLPs represented 40% of the North American midstream universe by market cap as of May 29 as shown below, but an investment fund with 40% MLPs is inefficient because the fund would be taxed as a corporation (potential tax drag) and have a lower, less tax-advantaged yield given the prevalence of C-Corps.

{kind=link}

{kind=link}

{kind=link}