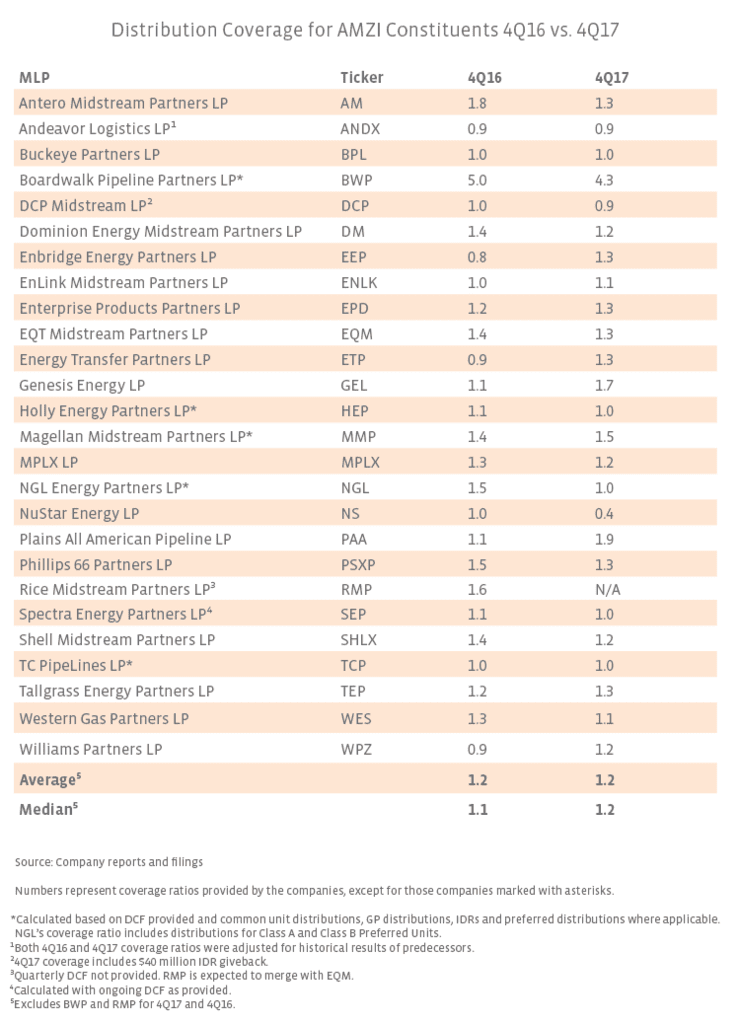

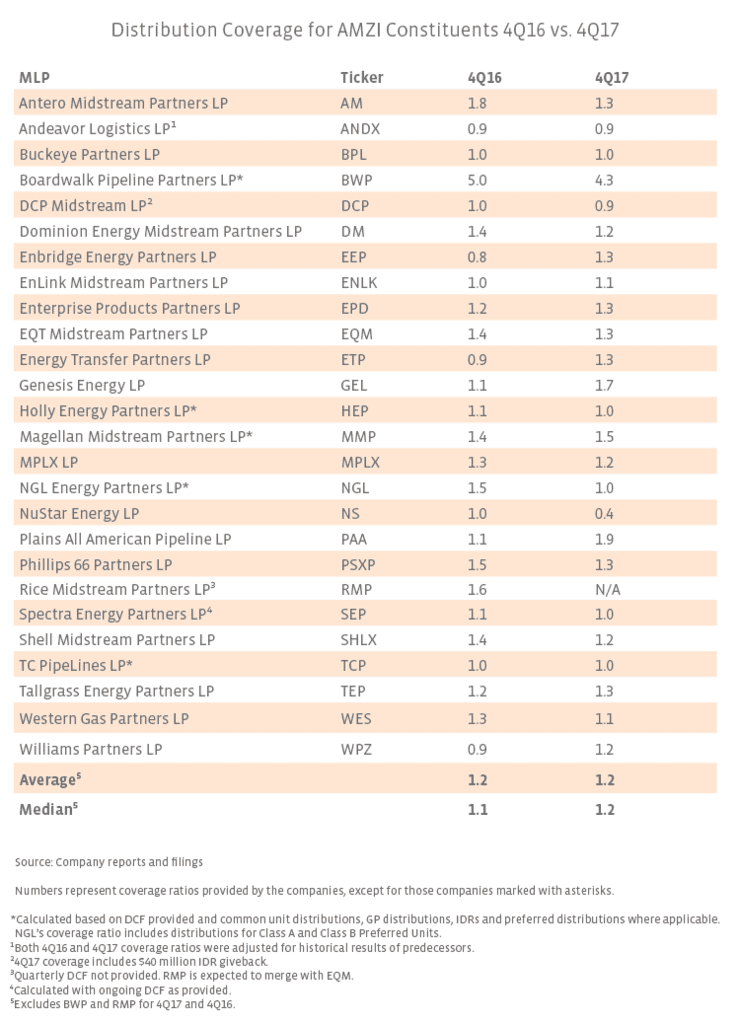

What conclusions can we draw?

For the group as a whole, coverage ratios appear to be healthy, or at least, comfortable. Interestingly, the average is consistent across the two periods, though certainly there are shifts for individual companies. Those MLPs that have guided to steeper distribution growth have seen a decrease in their coverage ratios from 4Q16 to 4Q17, including Shell Midstream Partners (SHLX), Antero Midstream Partners (AM), Phillips 66 Partners (PSXP) and Dominion Energy Partners (DM). These four MLPs have incentive distribution rights (IDRs), which results in higher payments to the general partner as the distribution grows (increasing the denominator in the coverage ratio calculation). Despite the decrease in coverage on a year-over-year basis, all four names were at or above the average for the group for 4Q17.

MLPs with distribution cuts since 4Q16, namely Genesis Energy (GEL), Plains All American (PAA) and Enbridge Energy Partners (EEP), show a notable improvement in coverage ratio from 4Q16 to 4Q17 as one would expect. NuStar Energy (NS) had the lowest distribution coverage ratio for 4Q17 and has already announced a distribution cut for 1Q18. Boardwalk Pipeline Partners’ (BWP) lofty coverage ratio is an outlier (and thus excluded from the average and median) but makes sense given its distribution run rate of $0.10 per unit since its 4Q13 distribution. Coverage ratios should directionally improve for companies pursuing self-funding and more moderate distribution growth, such as Enterprise Products Partners (EPD). Magellan Midstream Partners’ (MMP) relatively strong coverage ratio in both periods, similarly fits with its history of self-funding the equity portion of its capital.

Bottom Line

Coverage ratios will remain dynamic as individual MLPs shift towards self-funding and as high-growing MLPs mature. Admittedly, we’ve just provided a small snapshot of coverage ratios (26 out of 102 MLPs), however these names make up 69% of the total energy MLP market capitalization metric. Aside from NS, which has already announced a distribution cut, the data doesn’t appear to raise any red flags for AMZI constituents. Rather, hopefully it does the opposite and gives midstream MLP investors some peace of mind.

{kind=link}