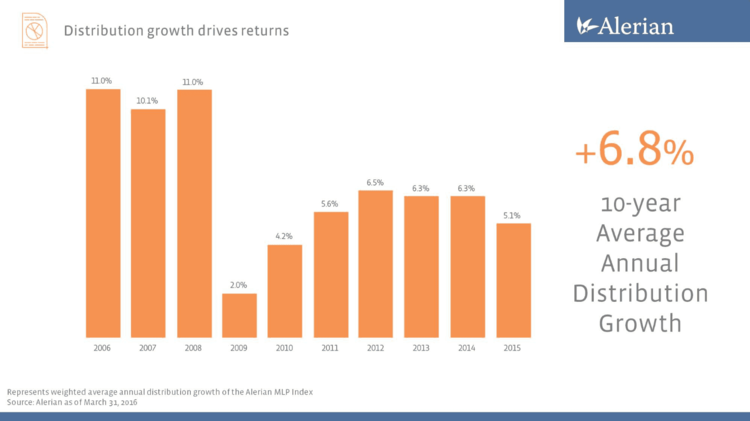

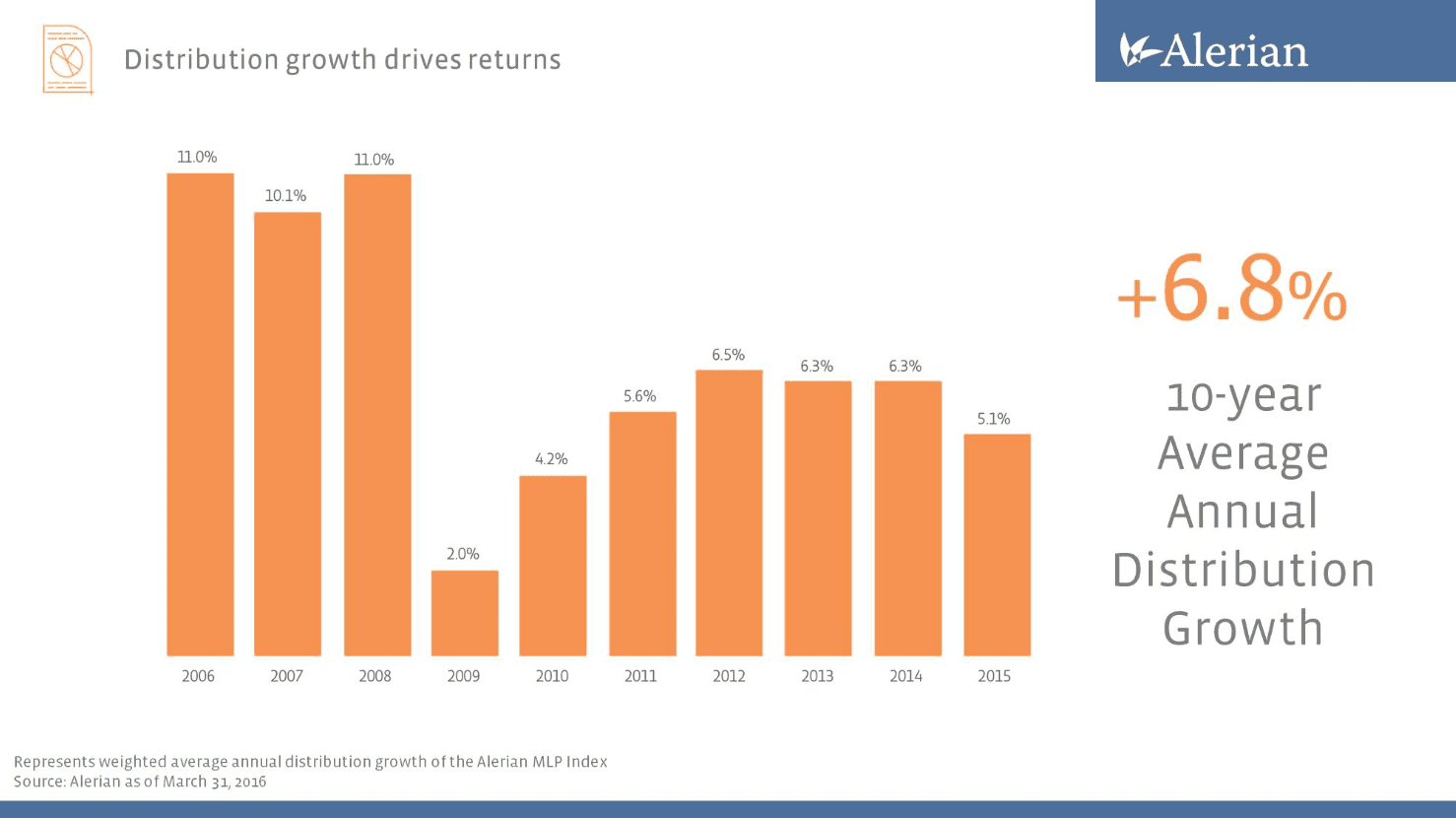

Alerian’s annual distribution chart (reproduced above) is perhaps our most popular chart ever. These numbers are all weighted averages by market cap, which means that Enterprise Products Partners (EPD) will have a heavy influence, but the smaller names (often with larger distribution growth) may not make much of an impact overall. For example, NGL Energy Partners (NGL) has a market cap of just $1.3 billion (giving it about a 0.5% weight in the AMZ), but raised its distribution by over 10% last year. Even so, investors are also appropriately concerned about a headline where any MLP has cut its distribution. We decided to make a series of histograms to see just how many MLPs raised their distributions by how much in the past decade.

The method for this study considered only those MLPs which intended to pay a stable distribution (ie, no variable distributors), and we also excluded the MLP GPs. For a company to be included, it needed to be trading for two full calendar years so we could measure annual distribution growth. Then, for example: total 2015 distributions are compared to total 2014 distributions to give a 2015 distribution growth number. Please note: this unavoidably introduces some survivorship bias as an MLP in hard times will often be acquired, which would remove it from this study. This method is a bit less complicated than the way Alerian calculates distribution growth in the above chart.

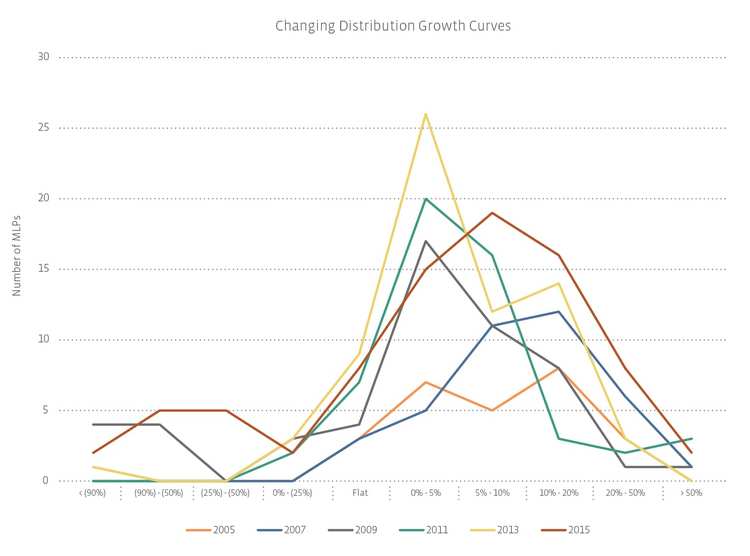

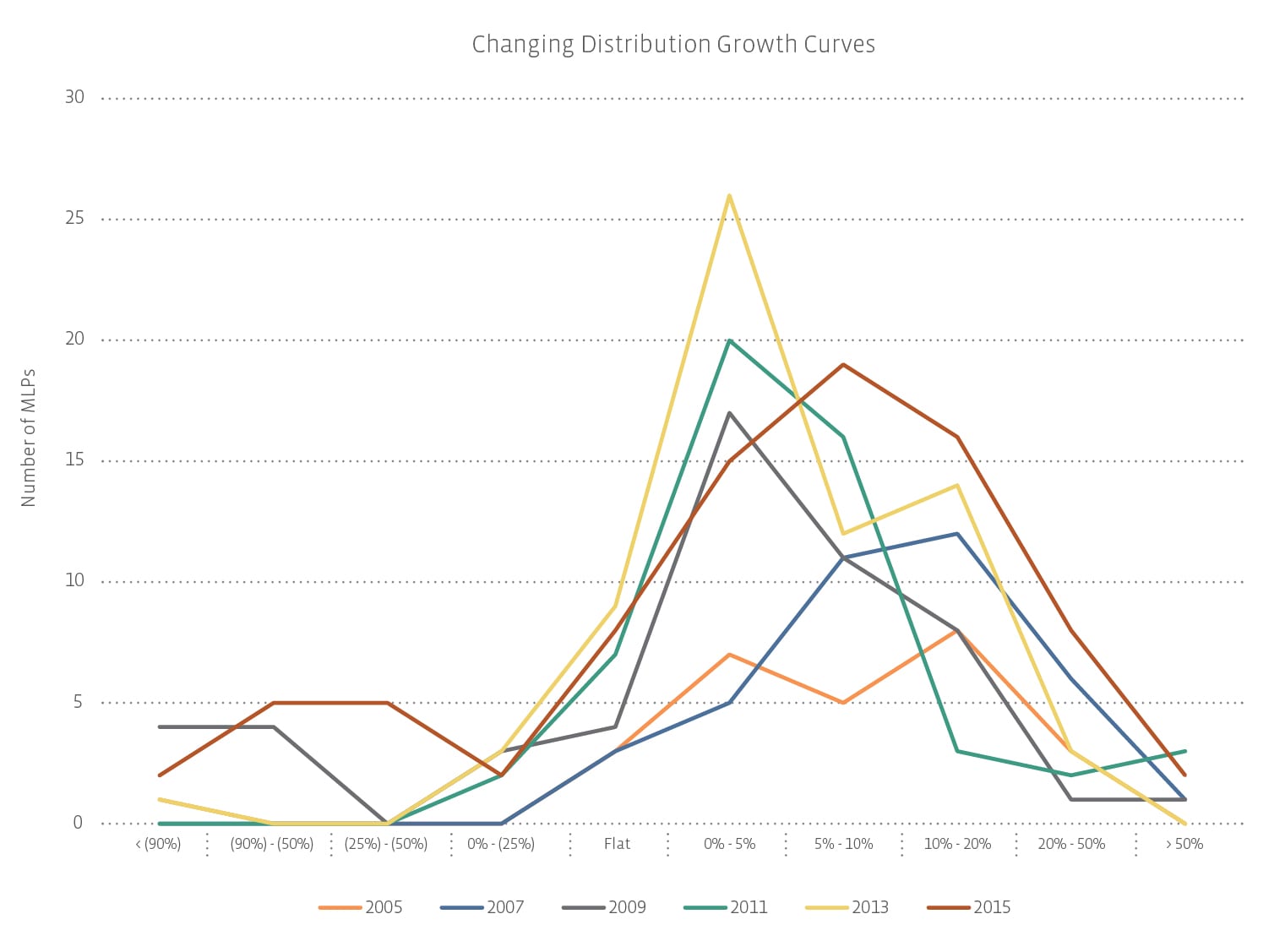

Once the data was compiled, the histogram categories were chosen to be:

(a) cut by more than 90%, which often represents an MLP eliminating its distribution entirely,

(b) a cut of 50%-90%, which is either a very significant cut, or an elimination later in the year,

© a cut of 25%-50%, perhaps indicating those MLPs that just need a bit more wiggle room,

(d) a cut of 25% or less,

(e) 0%, representing those companies which simply maintained distributions,

(f) growth of up to 5%, very common for established MLPs not making large acquisitions,

(g) 5%-10% distribution growth, where the annual weighted average tends to be,

(h) 10%-20%, an exceptional level of growth that can occasionally be maintained for several years for a high growth MLP,

(i) 20%-50% growth, often the result of a transformative transaction or a very generous GP

(j) growth of more than 50%, which is most often an MLP that previously cut its distribution reinstating it. Not always, though. In 2015, Tallgrass Energy Partners (TEP), thanks to its GP, was able to grow the distribution 52.8%.

What we found was that in the early years 2005-2008, distribution cuts were exceptionally rare and a plurality of MLPs actually grew their distributions in the 10%-20% range. An MLP was considerably more likely to grow its distribution by more than 20% than it was to cut the distribution.

Starting with 2009, the peak shifted downward, and the majority of MLPs raised their distribution by less than 5% each year. Of course, the two most difficult years, 2009 and 2015, also saw the most distribution cuts.

More recently, starting around 2012, as the number of MLPs continued to grow, the roughly normal distribution curve started to disappear. In 2012, the most common thing was to raise your distribution by 5% or less, or by 10%-20%. Same thing in 2013—the chart shows two peaks (the best fit line actually looked like a great sled riding hill). Some MLPs have matured and are now growing distributions in the stately low single digits, while other, newly formed MLPs are still experiencing new, early, and quite high growth. There are slightly fewer companies in between these options.

In 2015, one can perhaps see a Gaussian (or normal) distribution curve, but the tail risk is much fatter. In fact, as the number and variety of MLPs grows, so does the variety of distribution growth numbers.

Taken as a whole, the weighted average distribution growth has fallen, the histogram peak has shifted to the left, and the diversity of distribution growths all speak to an asset class that, at least in terms of its distribution growth, has been quietly maturing for the past several years.

With an emerging asset class, picking a winner is often as easy as one of those children’s balloon dart games at the carnival: everyone’s a winner! As we grow older, the games become more difficult and everyone does not win, and yet, the rewards are often just as valuable. Investors may not be able to expect standard double-digit distribution growth from MLPs anymore (well, at least not without a strong GP or aggressive appetite for M&A). More and more MLPs are keeping distributions flat, which doesn’t mean that it’s impossible to pick a winner, only that, unlike ten years ago, it’s just much harder to do.

{kind=link}

{kind=link}