Summary

- US oil production likely saw its relative low in May, but current prices are not high enough to incentivize an acceleration in upstream activity, though the rig count appears to have stabilized.

- Oil production is expected to remain largely steady throughout the rest of 2020 and most of next year before trending upward later in 2021.

- Midstream is well positioned to withstand the pressured commodity price environment relative to its energy peers as its fee-based business model and contract protections support greater cash flow stability.

US energy production has been significantly impacted by the commodity price weakness and demand destruction that came as a result of COVID-19. Curtailments and revised exploration and production (E&P) spending plans have created a dramatic shift in the industry as companies respond to the low oil price environment. Recent data and company updates have helped to frame the current and future state of oil production in the US. Today’s piece takes a closer look at this data to provide an update on US oil production and discuss the potential implications for energy infrastructure companies.

US oil production has likely already bottomed.

As WTI crude prices plummeted in March and April, E&Ps had to rapidly adjust their activities in response to the lower price environment and rising storage levels (read more). Many producers quickly shut in wells, with some curtailing as much as 70% of their total oil production in May (read more). This had a dramatic impact on overall US production. Per the Energy Information Administration (EIA), US oil production in May was only 10.0 million barrels per day (MMBpd), which was roughly in line with levels from January 2018. Since the lows in May, volumes have gradually recovered as oil prices above $35 per barrel (bbl) incentivized restoring shut-in production, but July oil production of 11.0 MMBpd was still 14.2% below peak production of 12.8 MMBpd from December 2019. With monthly production data lagging by two months, keep in mind that August and September volumes will be impacted by hurricane-related shut-ins in the Gulf of Mexico.

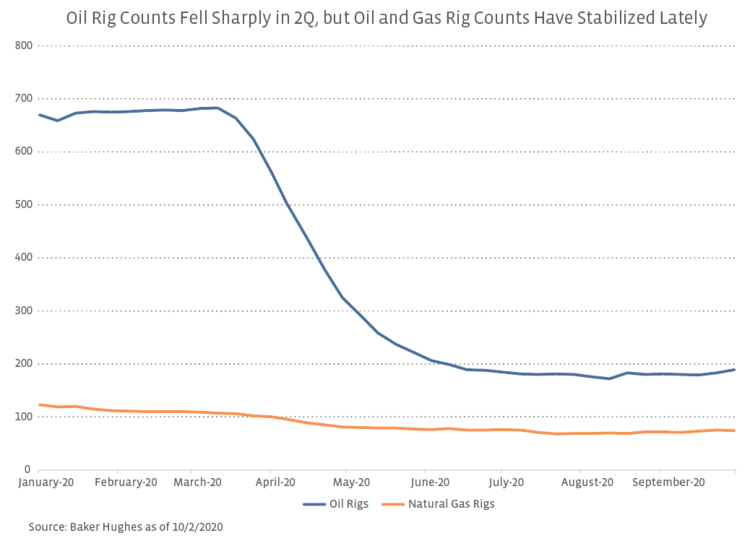

Rig counts weak but seem to have stabilized.

In response to weaker oil prices, oil and gas producers slashed upstream drilling activity, as reflected in the US rig count from Baker Hughes (BKR). As shown in the chart below, oil rig counts fell sharply after the March oil price collapse and remain depressed relative to history but have stabilized in recent months. The natural gas rig count has also fallen this year by ~40% but from a low starting point given weakness in natural gas prices well ahead of COVID-19. August was the first month this year since February that saw an increase in the total rig count, and September was the first month since February in which the oil rig count rose. While 189 oil rigs as of October 2 represents a ~10% increase from the relative low of 172 rigs on August 14, the oil rig count is still down over 70% year-to-date. With prices increasing sharply in August, natural gas has been a relative bright spot within energy as lower oil production has also resulted in less production of associated gas (read more). On 2Q calls in late July, natural gas producers like Cabot (COG) and EQT Corporation (EQT) were discussing flattish volumes for 2021 relative to 2020, but expectations could change if prices continue to improve.

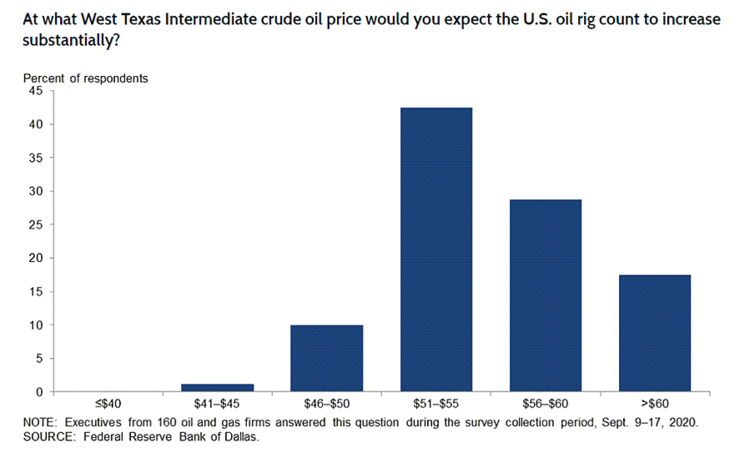

While the recent stabilization of oil prices around $40/bbl has been an improvement for the energy industry, the current oil price environment is simply not high enough to support noticeable production growth. A recent survey of 160 oil and gas companies conducted by the Dallas Federal Reserve indicated that 43% of executives believe WTI crude prices would have to be between $51/bbl and $55/bbl before the US would see a sizable increase in oil rig counts (see below). Almost 30% believed prices would need to be between $56 and $60/bbl for oil rig counts to noticeably increase. In the current price environment, producers are focused on capital discipline. For example, in the presentation discussing the merger of Devon Energy (DVN) and WPX Energy (WPX), management indicated that the combined company would limit production growth to 5% in any year even in a higher price environment, and with oil under $40/bbl, the company’s capex would be at maintenance levels. Producers tend to respond to the price environment with a lag, but until there is a greater recovery in prices, reduced upstream activity will not be sufficient to offset natural declines in wells, resulting in declining production.

Production forecasts remains muted for oil in the near-term, but there are some silver linings.

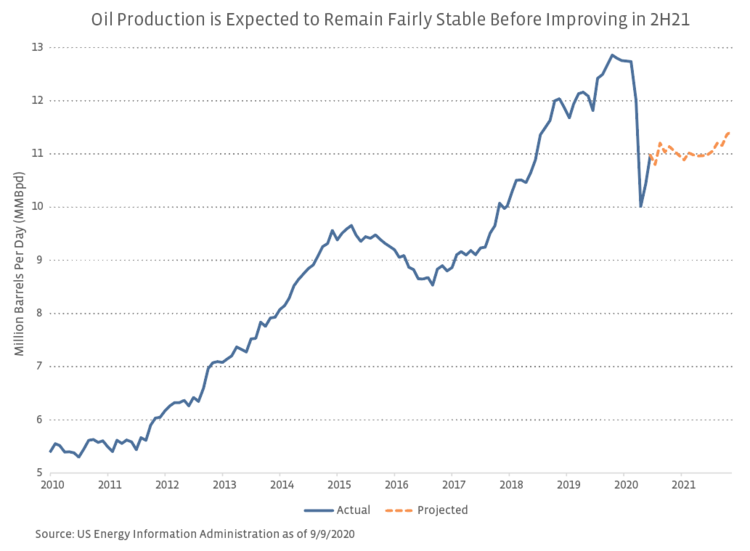

Looking ahead to the balance of 2020 and to 2021, oil production is expected to remain below pre-COVID levels. Per the EIA’s September Short-Term Energy Outlook (STEO), oil production is expected to hover around 11.0 MMBpd through August 2021 before growing to an estimated 11.4 MMBpd in December 2021. While this is a far cry from the lofty production seen in late 2019, it represents a significant rebound from May’s relative bottom. For context, the EIA is forecasting WTI oil prices at $45/bbl next year. A higher price environment would likely incentivize more upstream activity and support an improved production outlook.

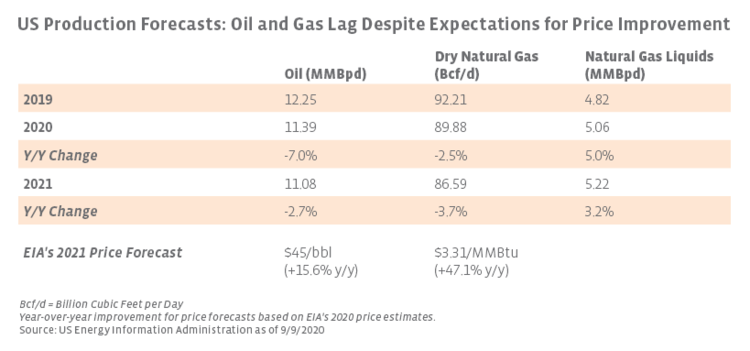

The table below provides some additional context by including the EIA’s annual production forecasts for natural gas and natural gas liquids (NGLs) alongside oil. The shut-ins following oil’s collapse clearly weigh on the 2020 oil forecast. While expected oil production in 2020 and 2021 looks weak when compared to the record high set in 2019, it bears mentioning that both annual forecasts are higher than 2018 production of 11.0 MMBpd. For natural gas, the EIA anticipates that production will decline through February 2021 and expects declining inventories to support notable price improvement, estimating that Henry Hub natural gas prices will be above $3.00 per million British thermal units (MMBtu) throughout next year. In contrast to oil and natural gas, natural gas liquids are expected to see production growth potentially driven by higher ethane recovery or greater production of NGLs from increased refining utilization (read more). While production and price forecasts are rarely correct, the EIA’s numbers are helpful for framing expectations based on what is known today. Despite expectations for oil and gas production declines in the near term, the US enjoys long-term advantages compared to other producing regions such as a significant resource base, the lower risk nature of onshore shale production, and the infrastructure network provided by midstream.

How does the production outlook impact midstream?

The expectation for declining oil and natural gas production has weighed on equities and raised concerns about midstream companies as volume-driven businesses. That said, the nature of midstream contracts has helped insulate their cash flows from the negative impacts of the current pressured environment (read more). Contract provisions like minimum volume commitments have ensured that energy infrastructure operators continue to receive steady cash flows even if lower volumes are flowing through their pipelines (read more). Additionally, 2Q20 earnings commentary in July and August indicated that the impact of the oil price decline on production was better than feared in April and May. Many midstream companies made upward revisions to 2020 financial guidance (read more), while others discussed improving pipeline flows. After initial expectations that 25 – 50% of volumes in oil-weighted basins would be shut in during 2Q and 3Q, Crestwood Equity Partners (CEQP) noted in early August that 90% of its Arrow system’s available production was flowing in the Bakken and expected 100% flow rates in 3Q20. While declining production reads negatively, we will discuss in our next note why it may not be as bad as it seems, especially for near-term equity performance.

Bottom Line

While the short-term outlook for US oil and gas production remains somewhat lackluster compared to the significant growth of recent years, the worst of the production impacts from oil’s price collapse appear to be in the rearview mirror. Oil prices would likely need to improve to over $50 per barrel to see a meaningful uptick in drilling activity. In the interim, midstream is well positioned to withstand the pressured commodity price environment relative to its energy peers as its fee-based business model and contract protections support greater cash flow stability.