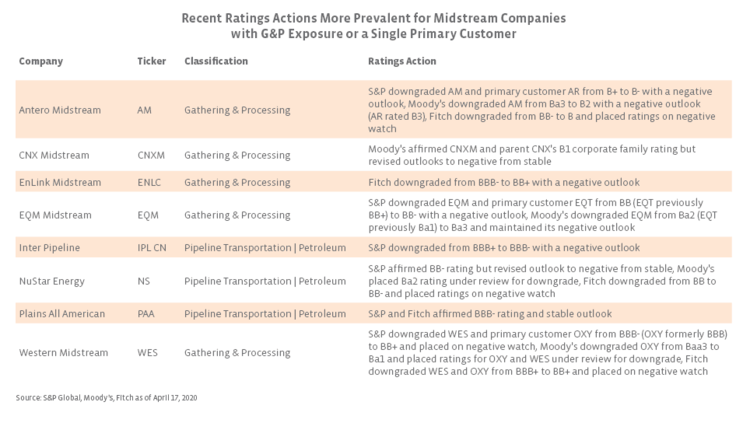

Among midstream companies focused on gathering and processing (G&P) or with single customer exposure, recent ratings actions are the result of several factors, including revised commodity price and volume assumptions, consideration of counterparty risk, and the outlook for primary customers. Ratings agencies noted in their analysis that ratings for midstream companies with significant exposure to a single producer customer, such as Antero Midstream (AM), CNX Midstream (CNXM), EQM Midstream (EQM), and Western Midstream (WES), will remain closely tied to ratings for their producer customers. For most of these midstream operators, the concern is that a high level of dependence on producer businesses with uncertain outlooks could lead to lower volume growth and a weaker cash flow outlook in addition to company-specific concerns. S&P, for instance, noted it is monitoring progress on EQM’s Mountain Valley Pipeline project, which has been delayed due to construction and regulatory issues. In its update on AM, Moody’s cited operations that were relatively concentrated in Appalachia, commodity exposure, and continued capex requirements among the factors that led to the downgrade.

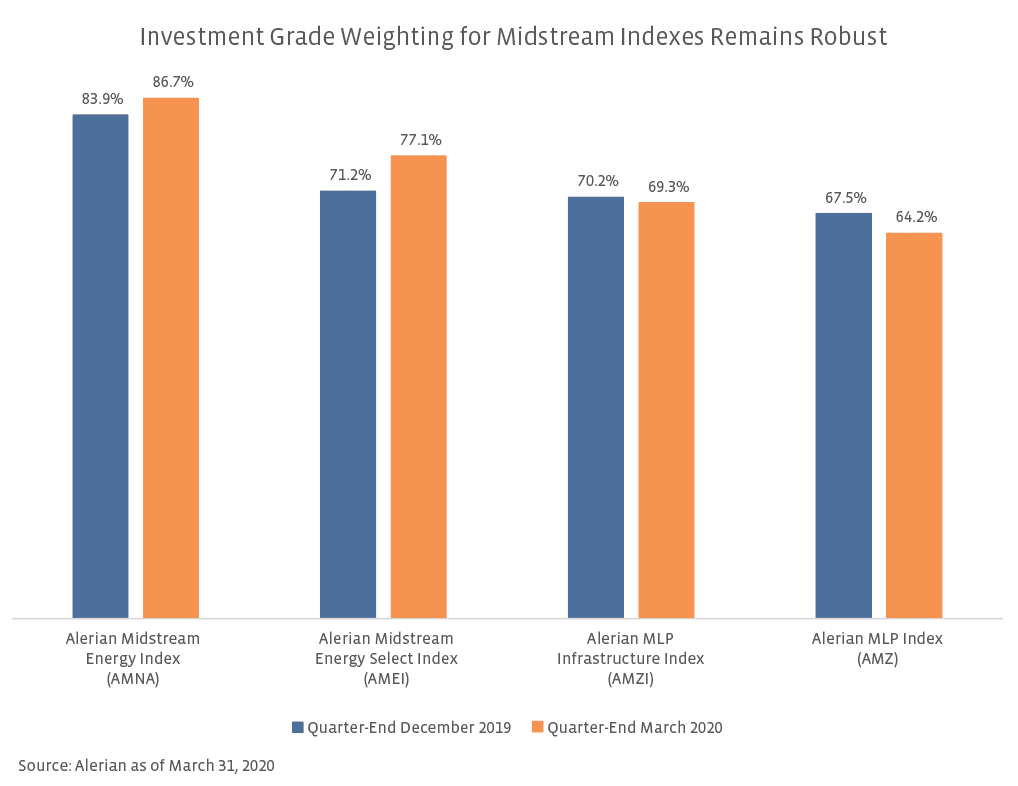

While the number of recent ratings updates is significant, it belies the lack of action for many of the better positioned names in the space. For example, S&P and Fitch affirmed Plains All American’s (PAA) BBB- rating with a stable outlook. Companies that have retained their investment grade status often possess flexibility given recent debt refinancing and credit facility availability (read more), lower leverage, and higher distribution coverage. For more challenged companies, management could decide to cut dividends when necessary as a way of accelerating balance sheet improvements, and many already have over the last month (read more). As shown in the table below, the Alerian Midstream Energy Index (AMNA), a broad composite index containing North American midstream MLPs and C-Corps, had a substantial investment grade weighting of 86.7% at the end of March, while the Alerian MLP Infrastructure Index (AMZI) was slightly lower at 69.3% (see chart below). Among the AMZI and AMEI indexes, Western Midstream (WES) is the only constituent that was downgraded from investment grade to high yield after all three agencies lowered its rating in conjunction with a downgrade for its primary customer, Occidental (OXY), in March. Overall, the weighting of investment grade companies in midstream and MLP indexes remains robust, with a majority of Alerian midstream index constituents by weighting having an investment grade rating. While some midstream companies may have to take short-term action to preserve their investment grade status, these companies are also more likely to have levers to pull to improve their balance sheet. As mentioned above, S&P and Fitch reaffirmed PAA’s investment grade rating after it cut its distribution by 50% in early April. While more ratings updates are likely in the coming weeks, proactive moves to strengthen balance sheets, reduce spending, and increase financial flexibility can help midstream weather current headwinds.

{kind=link}

{kind=link}