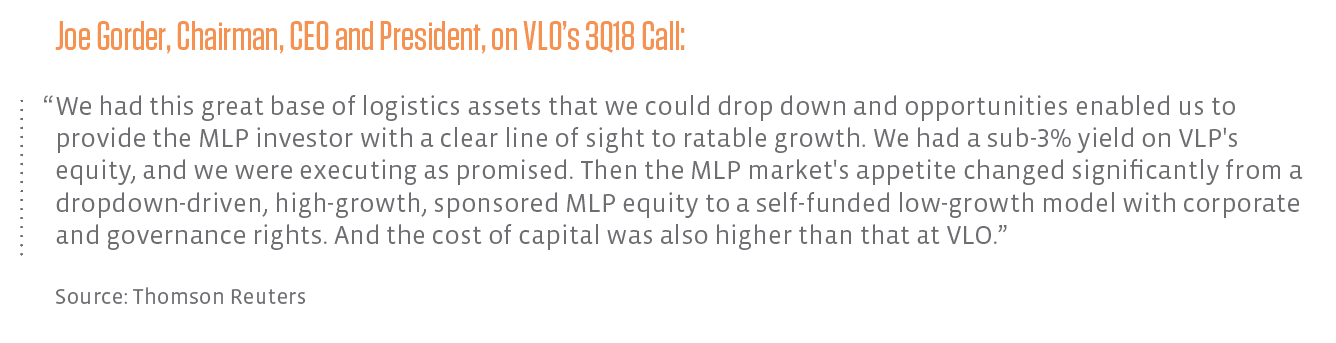

Last month, Valero (VLO) announced that it would acquire its MLP, Valero Energy Partners (VLP). VLP was intended to be a source of capital for VLO, but lackluster equity markets changed those plans. In September, Dominion Energy (D) proposed acquiring Dominion Energy Midstream Partners (DM), citing ongoing weakness in MLP capital markets and the negative impact of the FERC announcement from March on DM’s units. Of course, depressed equity values help make acquisitions easier (less expensive) for the parent, as does large parent ownership. D and VLO owned more than 60% of the common units of DM and VLP, respectively. If equity markets had been more accommodating, parent ownership may have been more modest.

Despite challenging markets, other MLPs have moved forward with dropdown transactions. It helps to have a supportive parent that is willing to take MLP units as payment or is accommodating with the sales price. There are other levers that can be pulled as well, such as IDR waivers. Earlier this month, Oasis Midstream Partners (OMP) was able to raise ~$40 million to help fund a dropdown from its parent, Oasis Petroleum (OAS). The $250 million purchase price represented 6.75x 2019 expected EBITDA. Half the purchase was expected to be funded with borrowings, and the balance was expected to come from capital market transactions (i.e. the equity offering) and issuing OMP units to OAS. Royal Dutch Shell (RDS-A) is expected to waive $50 million in distributions associated with IDR growth for Shell Midstream Partners (SHLX) in 2019. On their call, SHLX management indicated the $50 million could be used for organic growth or an acquisition. In early October, BP Midstream Partners (BPMP) acquired various assets from BP (BP) for $468 million in cash in its first dropdown. Notably, the transaction was financed using a revolving debt facility that BPMP had with an affiliate of BP – not equity. In short, dropdowns are viable and can happen against this market backdrop, but parents will likely need to be accommodating.

Could other dropdown MLPs be consolidation candidates?

Whether other dropdown MLPs will go the way of VLP and DM depends on several factors, including the positioning of the parent and the MLP. In general, we would characterize VLP and DM as one-offs with unique situations. That said, it bears mentioning that TC PipeLines (TCP) also struggled following the FERC announcement on March 15th. TCP has walked back the revenue and cash flow impact of the FERC tax policy change from an estimated $100 million in May to $20-30 million as of October. At its analyst day last week, TCP’s parent TransCanada (TRP) noted that the dropdown market was not available to them, and they weren’t sure if it would come back, which seems to imply some uncertainty around TCP’s future.

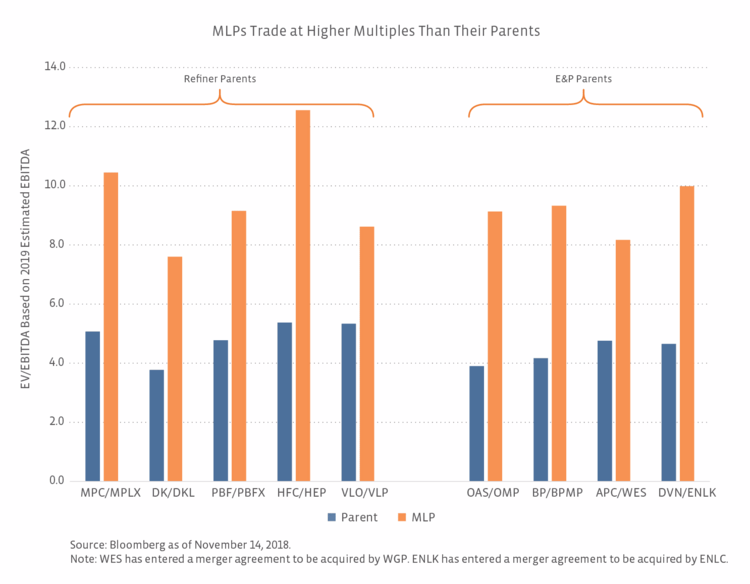

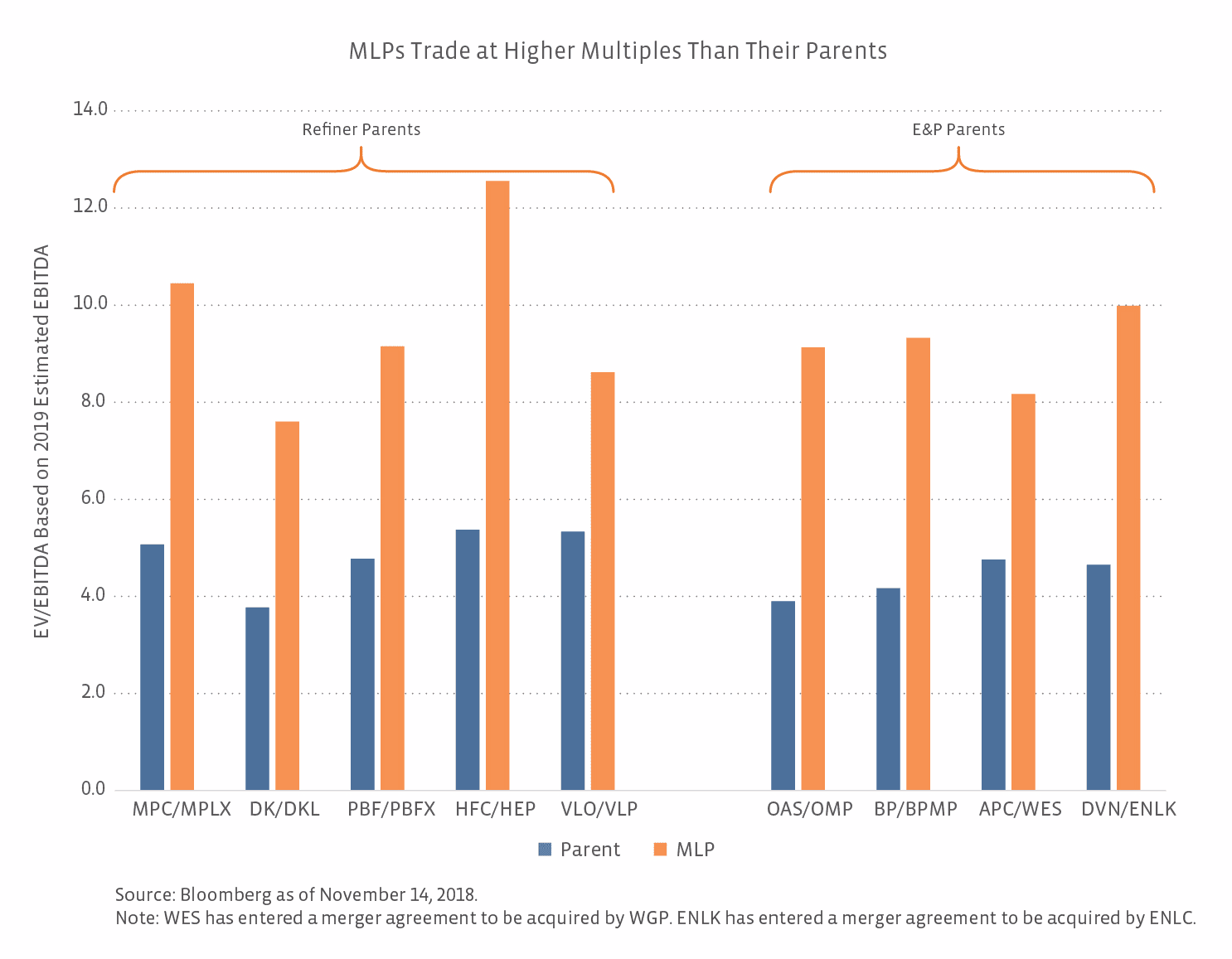

In thinking about additional consolidation of dropdown MLPs, keep in mind that MLPs trade at higher multiples than refiners or E&P companies. As you can see from the chart below, MLPs trade a few turns higher on forward EV/EBITDA than their parents. The refiners shown are trading at 4.9x on average, and the E&Ps (including BP, which is an integrated major) trade at 4.4x on average. The average for the MLPs shown is 9.4×. Midstream assets command a higher premium than refineries or wells, and that value may not be fully appreciated if midstream assets are held with refining or producing assets. Midstream assets in a publicly traded entity help provide transparency to the value of those assets for the parent. It bears noting that the valuation difference for VLO and VLP is the narrowest among the entities shown.

On their recent call, management of PBF Energy (PBF) said they were committed to PBF Logistics (PBFX), but they also indicated that they’ve been looking at everything and would take steps to position the partnership for the future. Many dropdown MLPs still have IDRs, with Holly Energy Partners (HEP) and MPLX (MPLX) notable exceptions. IDRs can be useful for young MLPs, but they are complex and a turn off for investors. Given their progressive nature, IDRs become more of a burden over time as the distribution grows. When it comes to transactions, we see dropdown MLPs as more likely to announce IDR eliminations than to be consolidated by their parents.

Making the change: Shifting from a dropdown story to an organic growth story.

Even MLPs considered to be dropdown stories often have an organic growth element. Some dropdown MLPs are less dependent on dropdowns than others. Phillips 66 Partners (PSXP) started as a dropdown MLP but has taken on organic growth projects, with dropdown assets providing optionality. Parent Phillips 66 (PSX) continues to pursue pipeline projects, which could be future dropdown candidates. Hess Midstream (HESM) stands out as not requiring a dropdown until beyond 2020, though dropdowns are expected to complement organic growth over time.

Other MLPs have largely exhausted their dropdown options to focus on organic growth (or third-party acquisitions) following sizable transactions with their parents. Earlier this year, MPLX completed its massive $8 billion dropdown, and EQM Midstream (EQM) acquired EQT’s (EQT) retained midstream assets. Accompanying its recent simplification announcement in which Western Gas Equity Partners (WGP) will acquire Western Gas Partners (WES), WES will also acquire practically all of Anadarko’s (APC) remaining midstream assets for $4.015 billion or roughly 9.5x 2019 EBITDA. Financing for all these transactions included cash from borrowings and equity issued to the parent. For MPLX and WES/WGP, the dropdowns also accompanied IDR elimination transactions.

Bottom line

Until equity markets improve, parents and dropdown MLPs will likely have to get more creative with their dropdown strategies to the extent dropdowns need to be executed. Parents will likely need to be supportive by taking equity, waiving IDR payments, and/or providing assets at an accommodating price. Certainly, those MLPs with visibility to growth independent of dropdowns are more insulated from the market environment.

{kind=link}

{kind=link}