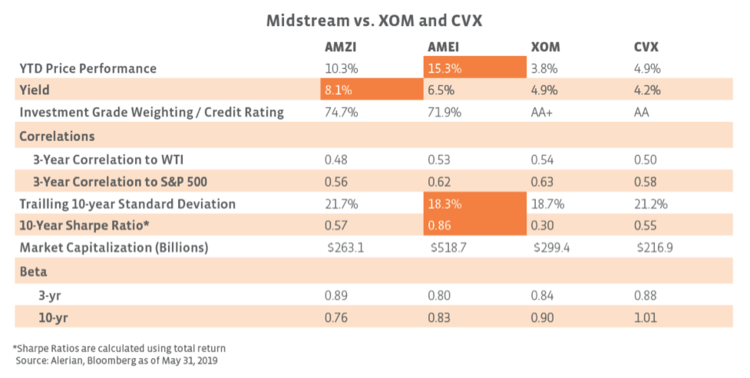

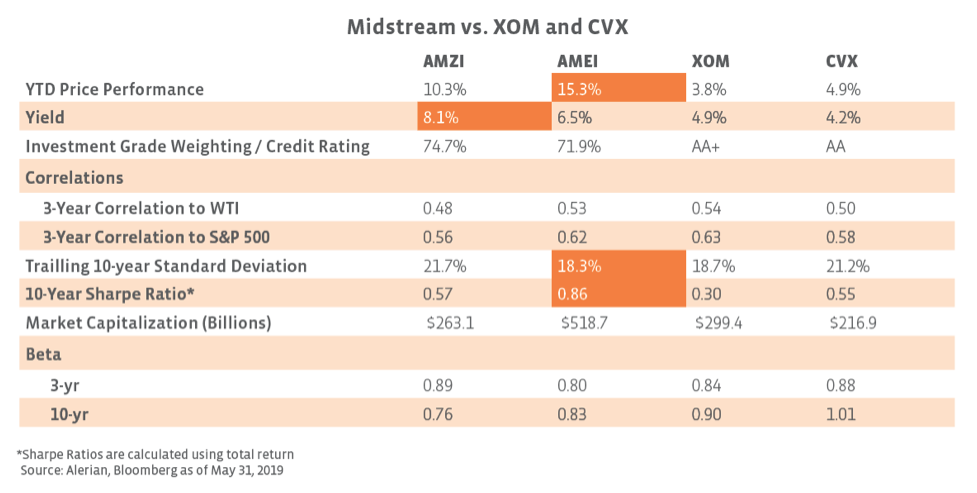

Sorting through the data above, midstream stands out for its stronger year-to-date performance and higher yields. The impressive credit ratings for XOM and CVX eclipse even the highest credit ratings among midstream companies (read more). Notably, midstream, XOM, and CVX are similarly matched in terms of their correlations with West Texas Intermediate (WTI) crude and the S&P 500. The AMEI stands out for its favorable Sharpe ratio relative to the others.

How does midstream compare to broader energy?

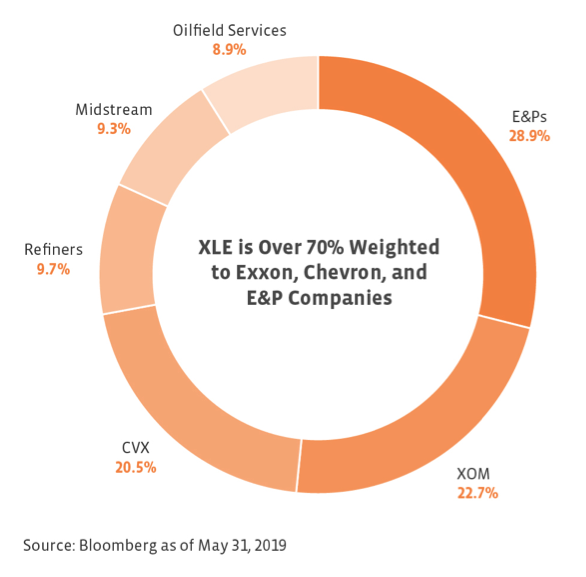

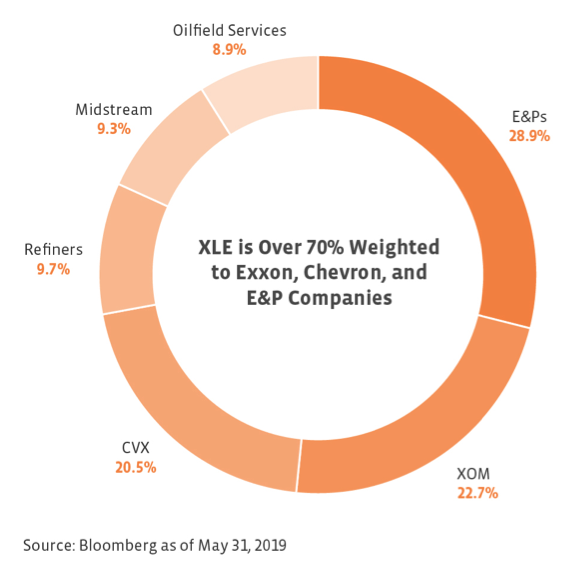

The comparison of midstream and the majors can be instructive for comparing midstream with broader energy given the prominence of XOM and CVX in energy indices. To represent broader energy, we use the S&P Energy Select Sector Index (IXE), which consists of the energy companies in the S&P 500 and is tracked by the Energy Select Sector SPDR Fund (XLE). The index weightings are based on float-adjusted market capitalization with a cap. As you can see from the pie chart of sector weightings, the XLE is heavily weighted towards XOM, CVX, and exploration and production companies (E&Ps). The midstream names included in the S&P 500 are Kinder Morgan (KMI), ONEOK (OKE), and the Williams Companies (WMB), which account for the 9.3% weighting in the XLE shown below.

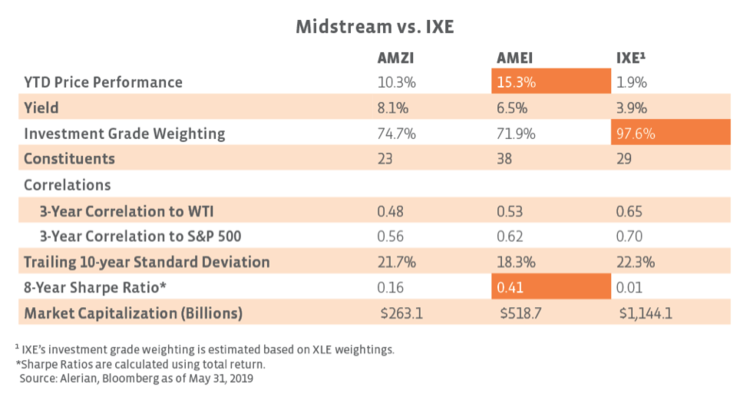

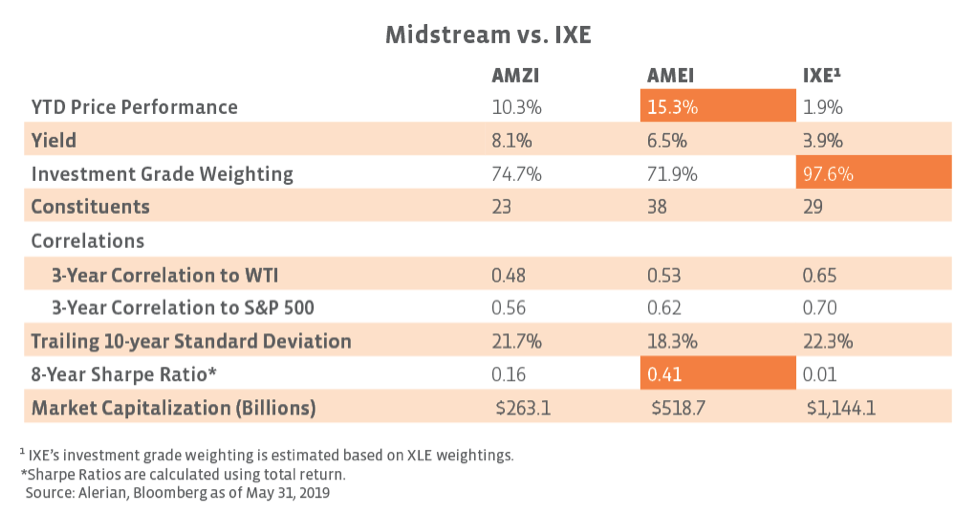

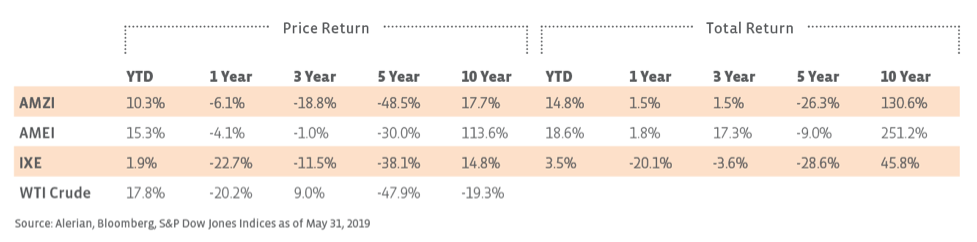

Comparing against the IXE, midstream again stands out for better performance this year and its generous yields. However, the IXE boasts better credit quality based on the weighting of investment grade companies. The IXE has a higher correlation with WTI crude, which one would expect given the weighting towards E&Ps, as well as a higher correlation with the broader market. Midstream screens more favorably based on the Sharpe ratio, which is calculated using total return and goes back eight years based on the availability of IXE total return data.

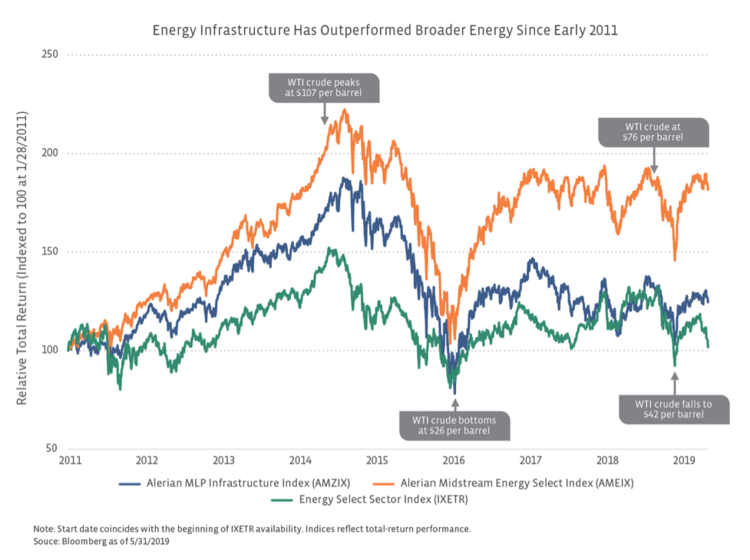

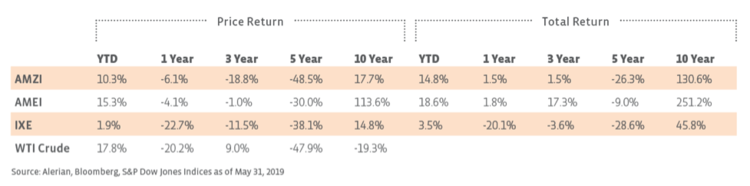

As shown in the chart below, when looking at total-return performance since early 2011, midstream has outperformed the IXE, with the AMEI performing particularly well on a relative basis. All three indices suffered in the period from oil’s relative peak in June 2014 to its bottom in February 2016, though AMEI has regained much of the lost ground. The start date for the chart coincides with the availability of IXE total return data on Bloomberg. The table below compares performance over different time periods for additional context. Of course, past performance does not guarantee future results.

Why has midstream outperformed so far this year?

Midstream has been the relative bright spot in energy despite commodity price volatility. While oil tends to command more attention, Henry Hub natural gas prices were trading at three-year lows in early June. Through June 12, WTI crude had fallen 22.9% from its peak of $66 per barrel on April 23. The IXE fell more than 12% during that timeframe, while the AMZI and AMEI were down 3.0% and 4.5% respectively. Midstream’s more defensive, fee-based business model has helped insulate it from the volatility in crude and natural gas prices. Additionally, recent private equity transactions, including the announced buyout of Buckeye Partners (BPL), have helped serve as a catalyst, while highlighting midstream’s value proposition (read more). Midstream may also be holding up better given company-level improvements, including reduced leverage, the shift to self-funding equity, and healthier distribution coverage.

What’s the bottom line for investors seeking energy exposure?

When comparing midstream products with an investment in the majors or a broader energy product, there are tradeoffs to consider based on investor preferences or outlooks.

Yield– Advantage midstream.An MLP or midstream product will typically provide a greater yield than the majors or a broad energy sector product while still providing energy exposure. Investment in an MLP or MLP-focused product may provide the added benefit of tax-deferred income if a portion of the distribution is considered a return of capital (read more).

Concerned about oil prices (prefer defensive investments) – Advantage midstream or majors. Midstream companies are defensive by nature of their business model, but the majors are defensive due to their size, credit quality, and consistent dividends.

Bullish Oil – Advantage energy sector product. Typically, a broad energy index with a heavy weighting towards E&Ps would be expected to outperform midstream in an environment of rising oil prices, though that hasn’t been the case this year. Rising oil prices are likely to be constructive for midstream but more so from a sentiment standpoint than in terms of impacting actual bottom lines. For E&Ps, rising oil prices should more directly benefit revenues and profitability.

Diversification across energy sectors – Advantage majors or energy sector product.An investment in the majors or an energy sector product will provide greater diversification across the energy value chain.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}