Summary //

- The impact of the pandemic varied by midstream business line, geography, company size, customer base, and other factors, but financial guidance for 2020 generally seemed to hold up reasonably well.

- EBITDA outlooks for 2021 are somewhat mixed relative to 2020 with some forecasting modest (or even robust) growth, and others expecting sequential declines, but outlooks appear stable overall.

- While buybacks have been in focus for midstream, there are still companies providing dividend growth.

As highlighted in the past (read more), midstream is unique within the energy sector in its ability to provide annual financial guidance, which is underwritten by the fee-based nature of midstream cash flows. Other energy subsectors, such as exploration and production companies or refiners, have more variable cash flows due to direct commodity price exposure, which prevents these companies from providing earnings projections or requires guidance to be based on commodity price assumptions that are difficult to get right. Today’s note briefly looks back at how 2020 guidance held up for midstream and looks ahead to financial and dividend guidance for 2021 from select companies.

2020 midstream guidance was mixed but held up reasonably well.

To better appreciate midstream guidance, it is helpful to look back on how forecasts held up in the unprecedented environment of 2020. Undoubtedly, the impact of the pandemic varied by midstream business line, geography, company size, customer base, and other factors. For example, a demand-pull natural gas pipeline serving a power plant likely saw less impact to volumes than a demand-pull refined product pipeline. Companies with extra crude storage may have been able to capitalize when the oil market went into super contango, but many midstream names would not have had that opportunity. Contract protections, such as minimum volume commitments, also vary by asset and company.

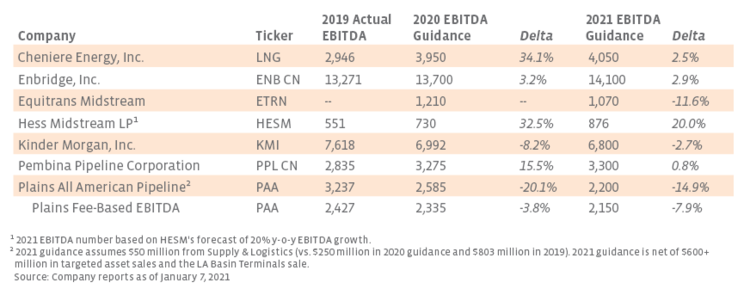

Acknowledging these unique circumstances for each entity, financial guidance for 2020 generally seemed to hold up reasonably well. While some midstream names had to permanently lower 2020 guidance given the unforeseen impacts of the pandemic, some maintained their financial projections throughout the year, including Williams (WMB), Enbridge (ENB), and Cheniere Energy (LNG). Others reverted to initial guidance later in the year after operational results proved better than feared. For example, Plains All American (PAA) guided to 2020 adjusted EBITDA of +/- $2.575 billion in February, then lowered guidance by $150 million in May, but raised guidance to +/- $2.585 billion in November – slightly above the initial guidance issued before the pandemic took hold. Hess Midstream (HESM) similarly lowered guidance in March, but 2020 EBITDA guidance from November was within the initial range provided in January. To be clear, some midstream companies did permanently lower guidance, but all things considered, guidance seemed to hold up fairly well. Management teams often err on the side of conservatism when providing forecasts, which may have proved particularly helpful in 2020. Of course, upcoming fourth quarter results will provide greater clarity on how midstream performed relative to company forecasts for the year, but outlooks from third quarter earnings season were largely encouraging.

What could be in store for 2021?

Though more updates are likely in conjunction with 4Q20 results, some companies have already provided initial financial guidance for 2021 or unveiled dividend plans. As shown below, EBITDA outlooks for 2021 are somewhat mixed relative to 2020 with some forecasting modest (or even robust) growth, and others expecting sequential declines. Overall, outlooks are generally stable all things considered. For PAA, the contributions from Supply & Logistics lead to greater variability in total earnings, but the fee-based EBITDA expectations shown in the table reflect more stability. PAA’s guidance for 2021 is net of planned asset sales of $600+ million, and management has guided to approximately $300 million in free cash flow after distributions in 2021 or $900 million or more if including asset sales.

When it comes to returning capital to shareholders in midstream, buybacks have certainly been more in focus lately (read more) given rising free cash flow and elevated yields across the space. That said, there are midstream companies still providing growing dividends. The table below includes companies that have guided to or already declared growing dividends for 2021. Enterprise Products Partners (EPD) announced a 1.1% distribution increase last week. Others have provided 2021 guidance or already declared an increased dividend for their next payout. Two of the companies below – EPD and Kinder Morgan (KMI) – also have buyback programs in place. Altus Midstream (ALTM) recently announced its first quarterly dividend of $1.50 per share consistent with prior guidance, and Macquarie Infrastructure Corporation (MIC) paid a special dividend of $11 per share last week. While some names are growing, other companies have plans to at least maintain current distributions in 2021, such as Magellan Midstream Partners (MMP) and Western Midstream Partners (WES).

Bottom Line

Midstream company guidance is useful for framing expectations for the year ahead. While more updates are expected with 4Q20 results, the outlooks for 2021 so far tend to be fairly steady. Though buybacks are in the limelight, income remains front and center for midstream with a few names poised to provide dividend growth this year.