Summary //

- The impact of the March 2018 policy revision from the FERC has largely played out, except for the impact on oil pipelines. FERC indicated in 2018 that it would incorporate its policy revision into the 2020 five-year review of the oil pipeline index, which is underway.

- Most interstate liquids pipelines use the FERC’s oil pipeline index to adjust their rates each year. FERC will use 2019 cost information to determine the index level for the five-year period beginning July 1, 2021.

- While the finalized index will likely vary from what was proposed last week, it is important to keep in mind that FERC is ultimately tasked with ensuring that interstate pipeline rates are just and reasonable.

In case there was not enough material to make 2020 an eventful year, this year also marks the five-year review of the oil pipeline index by the Federal Energy Regulatory Commission (FERC), which has implications for US liquids pipeline rates. Midstream investors likely remember the turmoil of March 15, 2018, when FERC announced a policy revision regarding pipeline rates that sent the midstream space spiraling. At the time, FERC indicated that it would incorporate its policy revision into the 2020 five-year review of the oil pipeline index. Last week, FERC proposed a new pipeline index level and invited comments on its proposal. Today’s piece explains the oil pipeline index and what investors should know about the index review. For more on FERC, please see this piece from last fall.

Editor’s Note: FERC’s website is currently being upgraded, which may cause some links in this piece to not work properly.

What was the policy revision from March 2018?

The determination of pipeline rates and nuances from the March 2018 FERC announcement are a bit in the weeds for the typical investor, but these details provide context to understanding why the oil pipeline index review is likely to be under additional scrutiny this year. On March 15, 2018, the FERC sent shockwaves through the midstream space in announcing that MLPs would no longer be allowed to receive an income tax allowance in cost-of-service pipeline rates. What does that mean? Some pipeline rates are based on the costs of operating the pipeline plus a reasonable return, and taxes had been included as a cost. Since MLPs do not pay taxes (read more), the policy change removed the “double” tax benefit for the pipeline rates of MLPs. To summarize, MLPs do not pay taxes, so they should not get to count taxes when adding up the costs of operating a pipeline to determine the rates charged to customers. While the March 2018 announcement led to a significant sell-off in midstream (read more), the finalized rule issued in July 2018 helped alleviate fears and uncertainty from the initial announcement (read more). Today, the impact of the policy change has largely played out, except for the impact on oil pipelines.

What is the oil pipeline index?

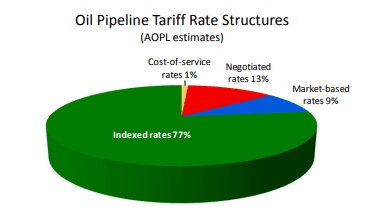

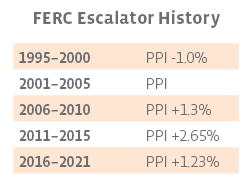

Most interstate liquids pipelines (those carrying oil, natural gas liquids, and refined products like gasoline) use indexing to adjust their rates each year based on FERC’s Oil Pipeline Index, which sets a maximum for annual rate increases. Specifically, the FERC uses an index based on the Producer Price Index for Finished Goods (PPI-FG) with some adjustment to reflect industry cost changes. For July 1, 2016, through mid-2021, the index is based on PPI-FG + 1.23%, with a multiplier provided each year based on the annual percent change in the PPI-FG. The table below includes past index levels. The methodology for the index is reviewed every five years, with the review for 2021-2026 currently underway. In its 2020 review, FERC is expected to evaluate the index based on how costs changed from 2014 through 2019. FERC will use cost information from Form 6 filings submitted by pipelines this spring to determine the index. While dated, the pie chart from the Association of Oil Pipe Lines (AOPL) below gives an indication of the prevalence of indexing.

Source: Association of Oil Pipe Lines from Magellan Midstream Partners’ |

Content continues below advertisement

Source: FERC |

For additional context, FERC issued an Advance Notice of Proposed Rulemaking in October 2016, calling for comments on potential changes to its approach in regulating oil pipeline rates. In February of this year, a vote by the FERC ended the proposed rulemaking – a decision that was welcomed by the industry. In short, FERC is not changing the process for regulating oil pipeline rates. However, the FERC is incorporating two key developments in recent years – the removal of the income tax allowance for MLPs and its May 2020 revision to the method used to calculate the return on equity (ROE) for interstate pipelines. As discussed in Targa Resources’ (TRGP) most recent 10-K, many components go into determining the oil pipeline index, and the FERC’s tax policy change impacts two items – income tax allowance and accumulated deferred income taxes.

What is proposed for 2020, and when is a final index level anticipated?

Last week, FERC proposed a new pipeline index level of PPI-FG + 0.09% for the five-year period beginning July 2021. While the proposed adjustment factor is a step down from 1.23% for 2016-2021, it is reassuring to see a positive adder put forth for comments. The proposed level is probably better than some had feared given FERC’s policy revision on the income tax allowance for MLPs. The final index level, which we would expect to be announced by the end of this year, will likely deviate from what was proposed as FERC takes into account feedback from various stakeholders as seen in the past.

The last five-year review in 2015 provides additional context. On June 30, 2015, the FERC issued a Notice of Inquiry, kicking off its index review and seeking comments regarding a proposed level of PPI-FG + 2-2.4% or any other methods for calculating that index level. On December 17, 2015, the FERC finalized the new index level for July 1, 2016, through June 30, 2021, at PPI-FG + 1.23%. The lower adjustment factor was attributed to using Page 700 data from Form 6 that better measures the changes in pipeline costs as well as updated filings and data corrections. If FERC followed the same timeline, the final index level for the five-year period beginning July 1, 2021, would be announced in December 2020. In its 2020 Analyst Day supplement from late March, Magellan Midstream Partners (MMP) expected a finalized index methodology at the end of 2020.

What’s next?

While the finalized index will likely vary from what was proposed, it is important to keep in mind that FERC is ultimately tasked with ensuring that interstate pipeline rates are just and reasonable. With the comment period underway, midstream companies are undoubtedly engaging with the FERC directly and through AOPL to lobby for a higher adder. On their 4Q19 earnings call, Plains All American (PAA) management indicated that they would work with FERC alongside the industry to try to ensure a logical implementation of revised income tax policy. Simultaneously, pipeline customers will be advocating for a lower rate. The deadline for comments is September 11, 2020.

Despite uncertainty surrounding the final index level, investors should be encouraged by the positive adjustment factor in the initial proposal and muted response in midstream equities since the announcement compared to the volatility of March 2018. The Alerian MLP Index (AMZ), which consisted of 53.1% petroleum pipeline transportation companies by weighting as of June 19, was down 2.2% Thursday and Friday, compared to a 0.5% decline for the S&P 500. If a pipeline ultimately determines that the new index level is not providing a reasonable return, it could file a rate case with the FERC to petition for a higher rate. Additionally, it bears mentioning that some liquids pipelines have market-based or negotiated rates that would not be impacted. For example, MMP uses the FERC’s indexing methodology for only 40% of the markets for its refined product pipelines.

Bottom line

By most indications, the update to FERC’s oil pipeline index should be much less eventful than the March 2018 policy revision that sent shockwaves through the space. Given that FERC is tasked with ensuring just and reasonable returns and the income tax change is one of many components evaluated, we do not expect a material negative impact to the industry from FERC’s 2020 oil pipeline index review.

{kind=link}

{kind=link}