Summary //

- With ESG gaining traction broadly among the investment community, discussions around ESG have also become more prevalent in the midstream space.

- The growing investor interest in ESG is an opportunity for midstream companies to highlight some of the risk management and safety practices that have long been a priority in the space.

- This piece and corresponding white paper introduce ESG concepts and how they apply to the midstream space, examine metrics currently disclosed by companies, and recommend additional metrics that would provide greater transparency for investors.

Environment, social, and governance factors, or ESG, comprise the criteria used by investors in a holistic approach to analyze an investment. Formerly a niche concept, ESG has moved toward the mainstream of finance in recent years as a result of investor demand, regulatory influence, and demographics. With ESG gaining traction broadly among the investment community, discussions around ESG have also become more prevalent in the midstream space. This piece discusses the current state of ESG within midstream, examining metrics currently disclosed by companies and recommending additional metrics that would provide greater transparency for investors.

Today’s piece is an abbreviated version of our recently published white paper of the same title. Please see the white paper for more detail and a complete appendix containing company level data.

ESG is moving from a niche concept to the mainstream.

Formerly a niche concept, consideration of ESG and its inclusion in financial analysis has become more pervasive in recent years. In addition to higher AUM dedicated to ESG, demographics and increased regulations have played a part in growing the ESG space. Although not typically considered an ESG investment, the oil and gas industry is not immune to the shift toward ESG. The interest in ESG issues among investors and the industry was evident at the MLP and Energy Infrastructure Conference in May, which included a well-attended ESG panel. ESG came up as a topic in most of the company presentations, which is acknowledgement by the management teams present that ESG is becoming increasingly relevant to investors. Finally, the general increase in data disclosures by companies on ESG issues has made more in-depth analysis possible.

Midstream participation in ESG has been bifurcated.

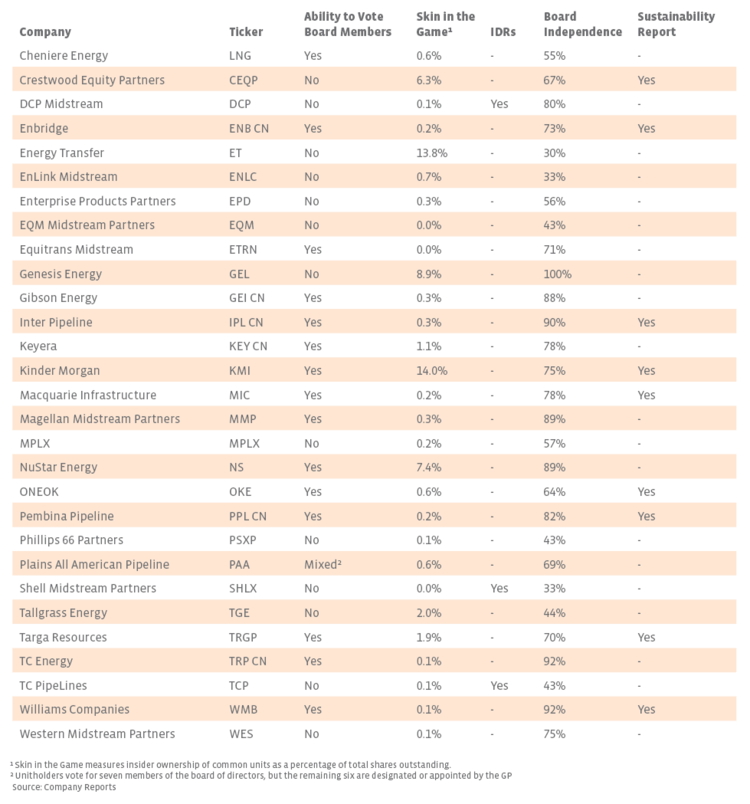

In general, the amount of disclosure on ESG issues by midstream companies is bifurcated between companies that have provided detailed reports on the topic and companies that have hardly acknowledged ESG concerns. The varied degree of transparency with disclosures and the relative lack of uniformity in the disclosures make comparison difficult among companies in the sector. However, several companies have taken steps to release an annual sustainability report containing information on how companies monitor and integrate ESG issues into their operations as well as long-term initiatives and goals. These reports also contain detailed data that was previously only tracked internally and not commonly disclosed. In 2019 alone, Crestwood Equity Partners (CEQP), Targa Resources (TRGP), and Williams (WMB) released their inaugural sustainability reports. Other companies have not released full sustainability reports but have engaged with investors on ESG topics during investor days and have increased the amount of disclosures on their websites.

For the more granular ESG disclosures, the data presented by midstream companies varies significantly. Some companies, especially those that have published sustainability reports, offer details including emissions data that are difficult or impossible to track without company disclosure. The degree of transparency with ESG metrics is one area for improvement among midstream companies, especially in the MLP space. Currently, CEQP is the only MLP to release a sustainability report, and while some other large MLPs have taken steps to disclose ESG data, further participation is necessary.

Environment: Operating effectively and managing environmental impact

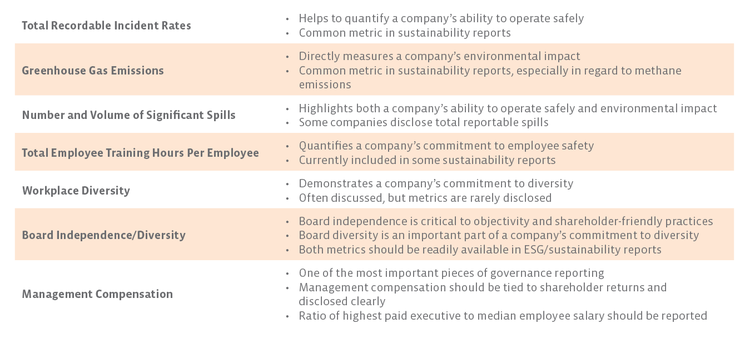

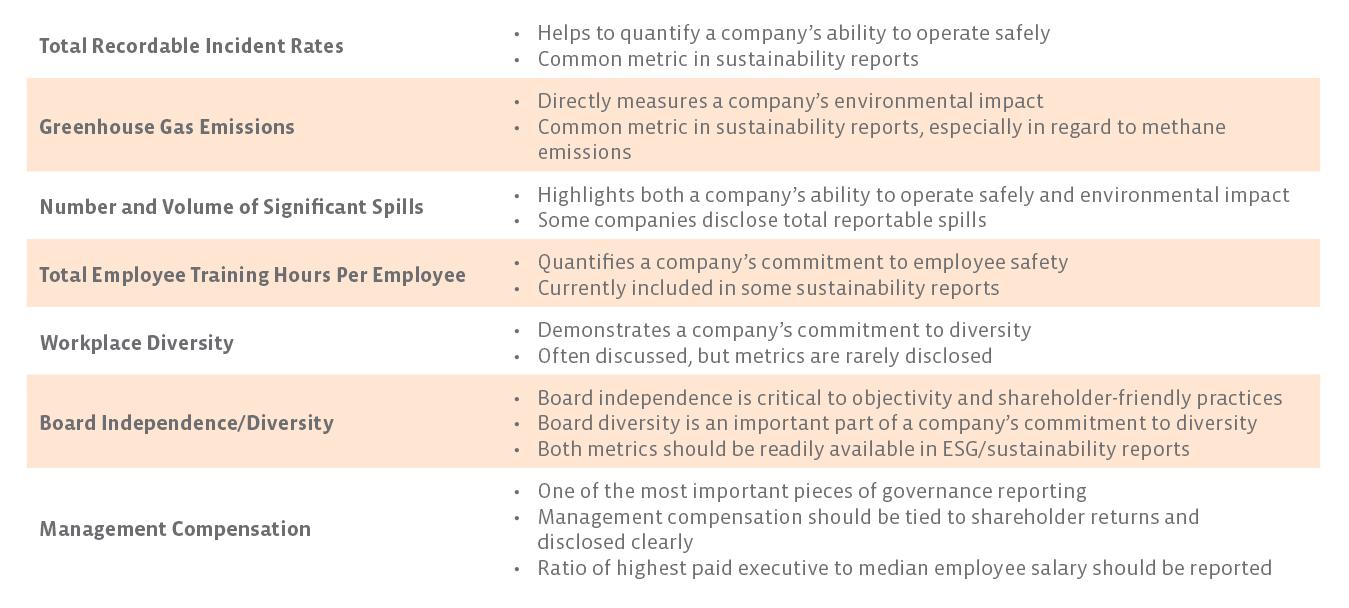

Environment includes operating effectively and encouraging best practices to minimize the impact on the environment. Specifically, midstream companies are focused on preventing spills and addressing pipeline routing and land usage. Pipeline spills are expensive from a cleanup and regulatory standpoint and can cause significant damage to a company’s reputation. As a result, companies have incentive to mitigate any spills through active monitoring of their assets and investment in technology that reduces risk. Pipelines have been criticized by opposition groups as unsafe and hazardous to the environment, but extensive research has found the opposite to be true – pipelines are the safest mode of transportation for oil and natural gas. Midstream operations teams plan pipeline routes to mitigate risks to conservation projects or endangered species, working with government agencies and local communities to meet or exceed regulatory expectations. Looking at metrics, there is not a set industry benchmark for EPA violations or PHMSA enforcement actions, but these should be as close to zero as possible given the paramount importance of safety and environmental stewardship.

Social: Managing relationships with employees and the community

The Social category of ESG refers to how a company manages its relationships with its employees and the community. Social includes issues such as diversity, workplace safety, community engagement and the pay gap within a company. Across energy, safety has been and will remain a priority for every company. Companies are also constantly reviewing safety training and drills for the sake of their employees and to ensure compliance with regulations. Companies disclosed varying metrics for safety, including safety training hours and the number of safety courses, exercises, and drills undertaken by employees during a given year.

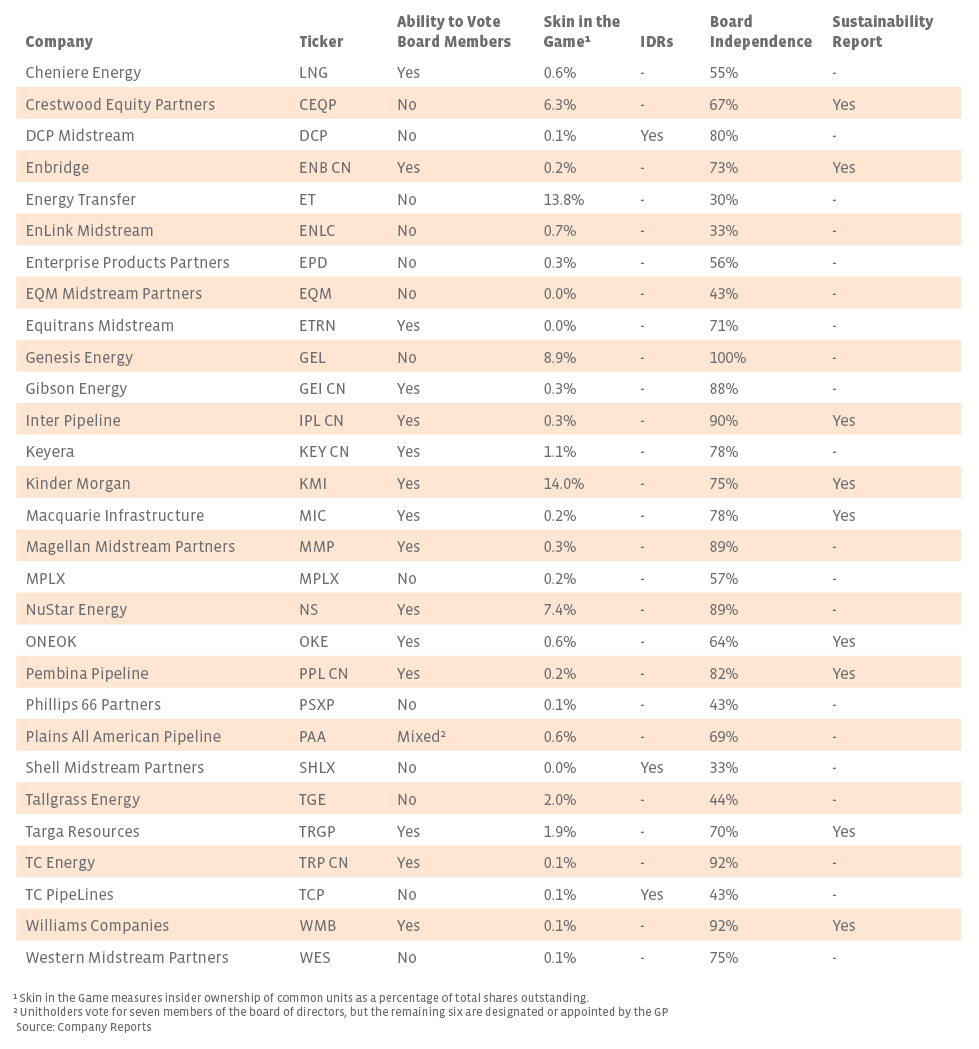

In addition to safety, the Social category also encompasses metrics like board diversity and the intra-corporate pay gap. Among the companies analyzed that reported their pay ratio, the median salary of the median employee was $111,341. At a glance, pay ratios for the midstream space compare favorably on a relative basis to other industries. Per a 2018 report, midstream would rank among the industries with the lowest pay gaps with a median of approximately 67 to 1 and slightly below broader energy at 72 to 1. For context, sectors such as health care and financial services typically have ratios of 150 to 1, given the high number of low-paid employees. Board diversity and independence is another Social issue that has been in focus. For the purposes of this paper, board diversity refers to the composition of the board by gender (although other factors can be considered), and independent board members are defined as those that do not have a position within the company. Midstream boards of directors are mostly composed of male members, with 81.8% of midstream boards represented by the AMNA top 30 being male.

Governance: Company oversight and aligning interests

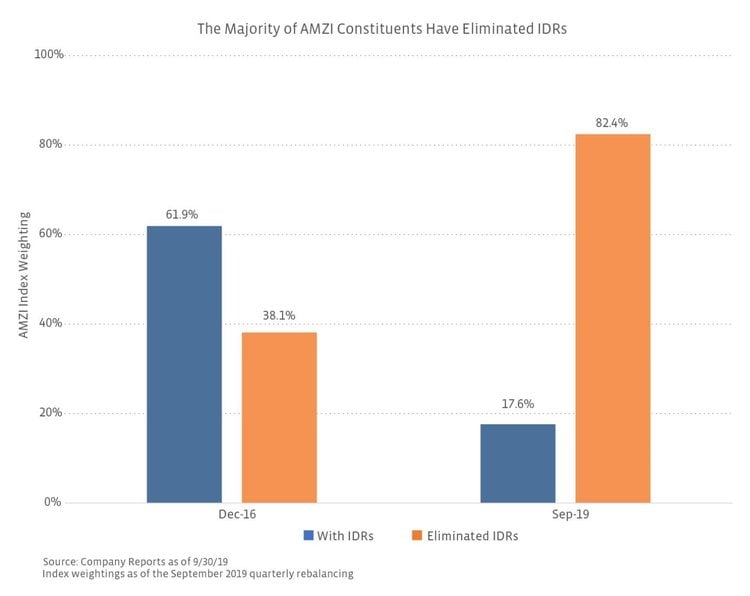

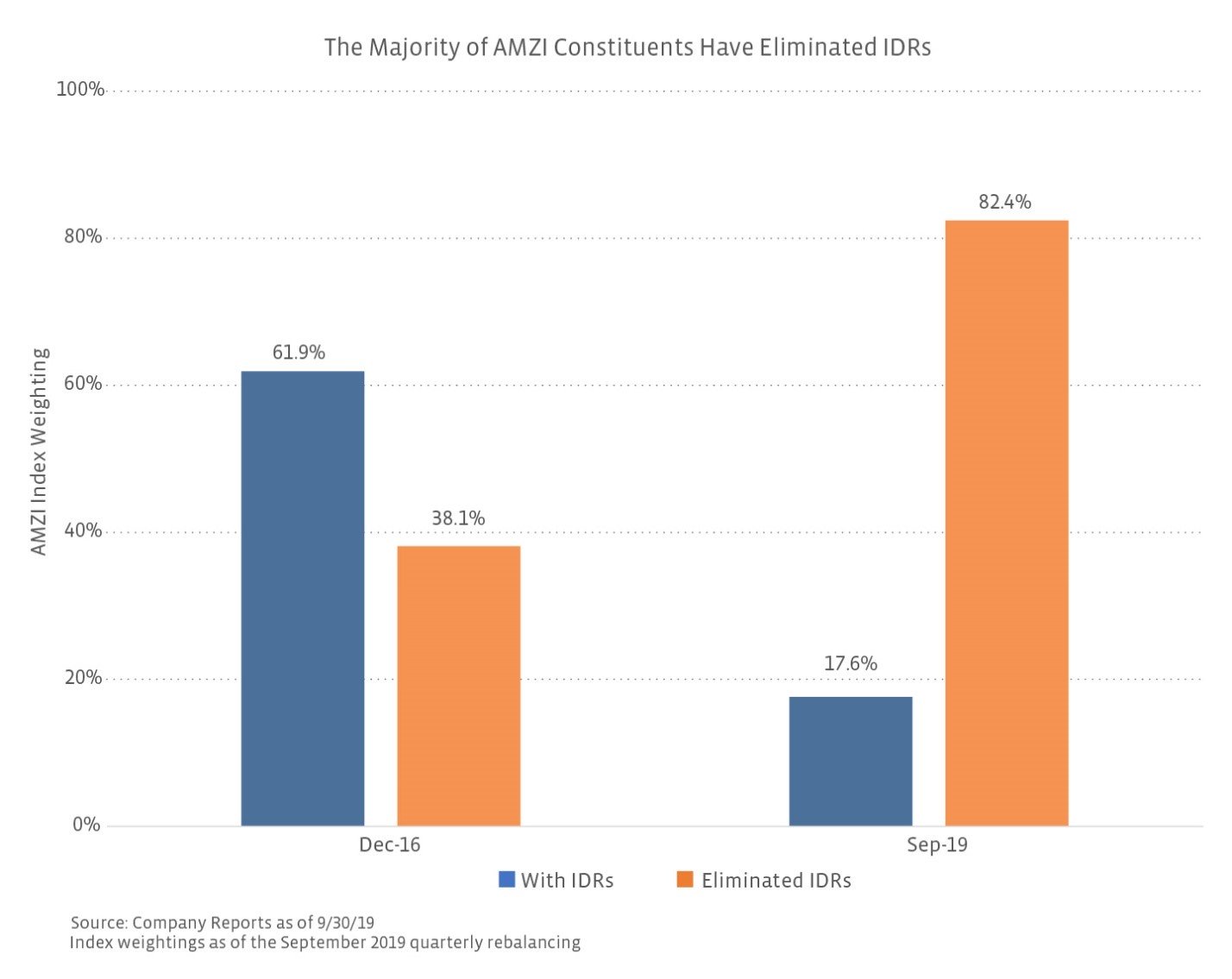

Governance is defined as the actions taken by management and the board of directors to ensure accountability, fairness, and transparency in a company’s relationship with its stakeholders. Rather than simply meeting regulatory or stock exchange requirements, effective corporate governance involves taking active steps to align executive and shareholder interests through consideration of economic interests, board independence, and shareholder voting rights. Historically, for MLPs, incentive distribution rights (IDRs) have been detrimental to governance and therefore a concern for investors. Although the initial goal of IDRs was to align the interests of the MLP and its general partner (GP) early in the life of the partnership, the structure is not sustainable as the MLP matures and IDRs become a burden on cost of equity. Looking at just MLPs, 82% of the constituents of the Alerian MLP Infrastructure Index (AMZI) by weight as of the September 2019 quarterly rebalancing have eliminated their IDRs compared to 38% at the end of 2016. The widespread elimination of IDRs is the best example of improving corporate governance in the MLP space.

{kind=link}

{kind=link}

{kind=link}