Demand recovery will take some time.

Countermeasures to stem the spread of COVID-19 had a tremendous impact on global oil demand – the magnitude of which overwhelms past examples of demand declines from the likes of global recessions. In April, when the widespread impact of COVID-19 was better appreciated, the International Energy Agency (IEA) estimated that 2020 oil demand would fall by 9.3 MMBpd in 2020, and April demand would be down 29 MMBpd on a year-over-year basis to 1995 levels, effectively erasing 25 years of demand growth. In the Oil Market Report from June, the IEA forecasted that annual oil demand would be down 8.1 MMBpd in 2020 and increase by 5.7 MMBpd in 2021. In revising its 2020 demand expectation, the IEA cited a swift recovery in China’s oil demand in March and April as well as improving demand in India in May. Notably, the IEA attributed the 2.4 MMBpd difference between actual 2019 demand and the 2021 forecast to weakness in jet fuel, which is expected to weigh on total oil demand through 2022.

While the IEA is the authority for global energy, the US Energy Information Administration (EIA) also provides a global outlook. The EIA is forecasting a slightly steeper global demand decline of 8.3 MMBpd for 2020 and a more pronounced recovery in 2021 of 7.2 MMBpd. While uncertainty around COVID-19 complicates forecasts, it is positive to see that 2021 demand is expected to be at 97.4% or 99.7% of 2019 demand based on IEA and EIA estimates, respectively. With the worst of the demand decline seemingly in the rearview, market observers will continue to watch for signs of further improvement, particularly in the US, which represents approximately one-fifth of total worldwide oil demand.

OPEC+ production cuts provide constructive visibility.

The unprecedented demand impact from the global shutdown following the emergence of COVID-19 required a similarly unprecedented supply response from OPEC and its counterparts. As a reminder, OPEC+ agreed in April to cut production by 9.7 million barrels per day (MMBpd) beginning May 1. The cuts were initially slated to ease in July to 7.7 MMBpd, but on June 6, OPEC+ extended the nearly 10 MMBpd cut through next month. As a condition, countries that had not complied with the initial cuts were obligated to reduce their supply in subsequent months to make up for overproducing. As outlined in April, cuts of 7.7 MMBpd are slated to continue through 2H20, with the volume moderating to 5.8 MMBpd from January 2021 through April 2022. The duration of the planned OPEC+ cuts aligns well with the expectation that demand will recover gradually.

US oil production remains a wildcard.

Assuming countries comply with their quotas and remain committed to cuts, OPEC+ supply is fairly straightforward in contrast to the outlook for US oil production, which is complicated by uncertainty around production curtailments. This is evident in the divergence in June production estimates from the US Energy Information Administration (EIA) and the international energy authority, the IEA. The EIA is forecasting US oil production of 11.2 MMBpd in June in its Short-Term Energy Outlook from June 9. On the other hand, the IEA is forecasting June oil production of 10.5 MMBpd for the US in their report from June 16. The 700,000 barrel per day difference is significant. The IEA’s June estimate is even lower than the production level where the EIA expects US oil output to bottom in March 2021 (10.6 MMBpd).

Why are estimates so different for the two organizations? Presumably, there are varying assumptions around production curtailments. Exploration and production (E&P) companies responded to weak oil prices by temporarily shutting in production in some areas (read more), but with WTI oil prices hovering around $40/bbl, companies are increasingly bringing oil production back online. The pace and magnitude of returning shut-in volumes is more challenging to gauge, particularly among private operators. Multiple public companies have adjusted their plans in response to higher oil prices. In a filing from June 3, WPX Energy (WPX) indicated that its shut-in wells were beginning to be brought back to production. Continental Resources (CLR), which had curtailed 70% of its operated oil production in May, plans to resume some production in July, taking curtailments to 50%. Reuters reported last week that the CEO of Devon Energy (DVN) does not expect any significant production curtailments for the company in 3Q20 or beyond if oil prices stay around $30 per barrel at a minimum.

In short, oil prices have returned to a level that encourages US shale producers to restore shut-in wells to production, but prices today are not high enough to incentivize much in the way of new drilling. Per Baker Hughes (BKR), the US oil rig count stood at 189 as of June 19, which is on par with levels last seen in 2009. If oil prices improve further to $50-$60+ per barrel, US producers are more likely to respond with increased upstream activity, but companies are also emphasizing capital discipline and returns given long-standing investor concerns around capital allocation. Capital discipline may serve as a check on companies’ production growth and help prevent US shale volumes from overshooting in a higher oil price environment, which could be positive for the balance of the global oil market.

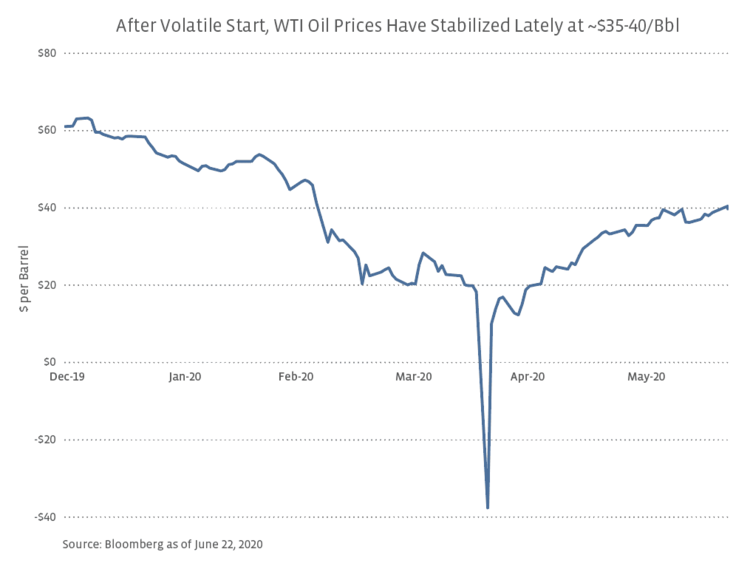

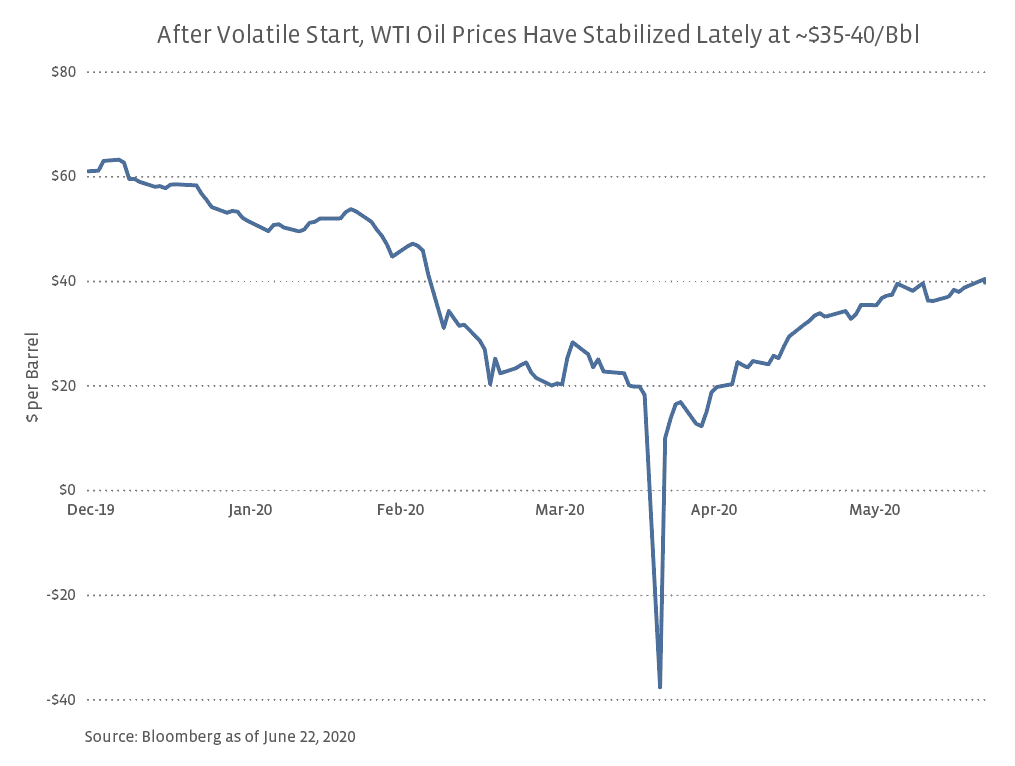

What could be next for oil prices?

Compared to several weeks ago, the oil market is much healthier, as evidenced by the narrowed contango in the WTI oil futures curve with the six-month calendar spread recently around $0.50/bbl. With OPEC+ supply somewhat of a known variable given cut agreements through 2022 (assuming adequate compliance and a continued commitment), the recovery in oil prices will largely depend on the recovery in global oil demand and how US oil producers respond to the price environment. The bottom in oil demand seems to be behind us, but a significant reintroduction of stay-at-home measures to stem the spread of coronavirus could be a setback for improving demand and oil prices. A more accelerated demand recovery would be bullish.

US oil production bears watching given that the US is the world’s largest oil producer, and US producers are simply reacting to oil prices as opposed to being subject to quotas. While some shut-in volumes are returning, other curtailments remain, and existing production is subject to natural decline rates, which are not being offset by significant upstream activity (drilling and completing new wells). If prices improve beyond $50 or $60/bbl, producers may increase their activity but likely with a greater focus on discipline than demonstrated in the past, which could be constructive for a price recovery.

While much has improved in oil markets, prices are likely to remain volatile given uncertainty around demand. For investors, midstream energy infrastructure continues to provide some exposure to an oil recovery given implications for sentiment and US energy production, while also providing relatively defensive energy exposure and attractive yields supported by more stable cash flows. Midstream’s fee-based business model and contract protections help insulate companies from oil price volatility and production declines, making the space a relative safe haven within energy.

{kind=link}