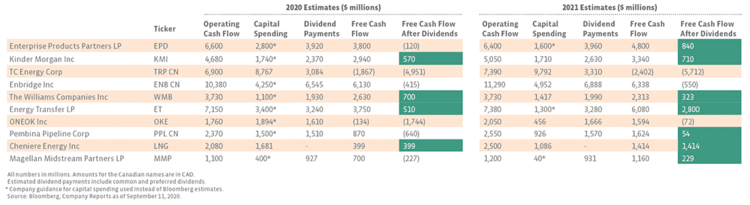

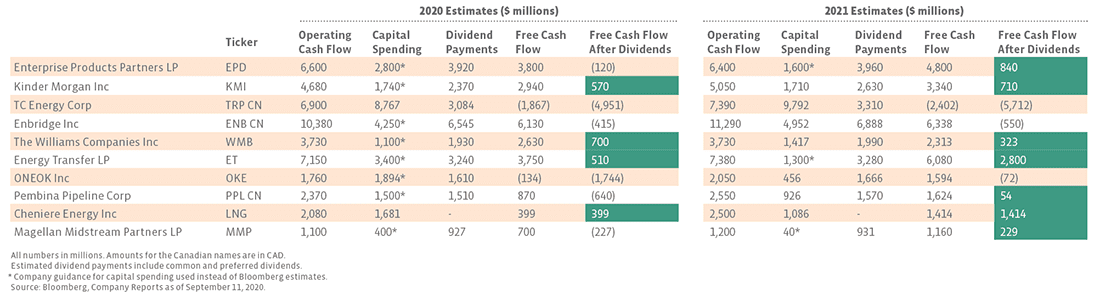

To better appreciate the financial flexibility of free cash flow, it is helpful to evaluate on an after-dividend basis. For midstream, free cash flow after dividends is particularly useful given the generous income provided by these companies. The money left over after dividends is what can be used to reduce debt or even repurchase shares. To illustrate the free cash flow potential of midstream, the table below shows estimated 2020 and 2021 free cash flow for the top constituents of AMNA based on Bloomberg estimates and company guidance for capital spending where available. Keep in mind that none of these companies cut their dividends this year. Cheniere Energy (LNG) does not pay a dividend but does have a share repurchase program.

Of these companies, many are expected to generate free cash flow in 2020 and 2021, with a few forecasted to have positive free cash flow after dividends in 2020 and even more expected to join that number in 2021. Considering EPD and Energy Transfer (ET) are expecting significant reductions to growth capital spending in 2021, both are forecasted to generate meaningful free cash flow after dividends next year. Setting aside TC Energy (TRP) and Enbridge (ENB), which are discussed below, midstream names appear well positioned to generate significant free cash flow next year, with some forecasted to have plenty of cash left over after paying dividends based on these estimates. Importantly, the estimates do not assume any dividend cuts, which would lower the after-dividend hurdle. While this analysis focused on the top constituents of AMNA, these companies exemplify a broader trend across midstream, with many other companies discussing free cash flow generation this year or next (read more).

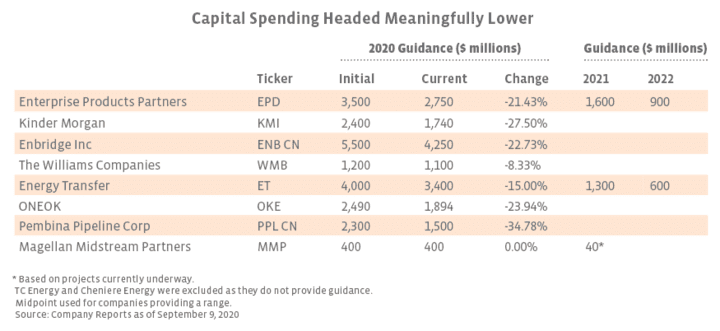

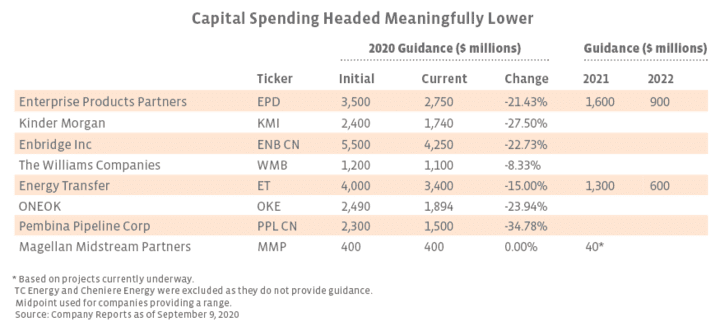

Relative to the others, TRP and ENB stand out for significant and growing capital spending expectations, which support a differentiated growth profile but impair free cash flow generation. While the company does not provide capex guidance, TRP has a capital program exceeding $37 billion (CAD) with $11 billion in projects currently underway. Similarly, ENB has an $11 billion (CAD) capital program through 2022. TRP and ENB remain in growth mode with new projects supporting growing dividends. TRP has guided to dividend growth of 8-10% in 2021 and 5-7% beyond 2021, while ENB grew its dividend by 9.8% in 2020 and discussed 5-7% growth at its December 2019 analyst day with a view to a 65% long-term payout target.

So what?

With a few notable exceptions, the complexion of growth in midstream is changing. Historically, dividend growth was supported by increasing cash flows from investing in new projects (or acquisitions) as is still the case with TRP and ENB. More broadly, dividend growth going forward will still be supported to some extent by growth projects, but it will also be supported by increasing free cash flow as growth spending moderates from the very high levels required to facilitate the shale revolution over the last several years, and companies reap the cash flows of past projects.

Free cash flow is a good thing. It can be used to reduce debt for those with elevated leverage. If balance sheets are well positioned, it can be used for shareholder-friendly actions like buybacks and dividend increases. Given current uncertainty, excess cash flow is likely to be used to enhance the balance sheet, but in a more stable macro environment, buybacks and dividend increases could see greater traction. In addition to Cheniere, EPD, Kinder Morgan (KMI), and Magellan Midstream Partners (MMP) currently have buyback authorizations in place. In terms of dividend hikes, KMI has noted a commitment to increase its dividend to $1.25 per share annualized (from $1.05 now), but its board will weigh many factors when it meets early next year. More broadly, as the space looks ahead to 2021, perhaps increasing free cash flow generation (and potentially more buybacks) will be coupled with an improved macro energy backdrop to the benefit of midstream investors, replacing 2020 headwinds with tailwinds.

{kind=link}

{kind=link}