In last quarter’s installment, we examined how an MLP in the high splits would pay increasing portions of its cash flow to the general partner (GP). Given this “GP tax,” some investors may choose to sell their investment once it reaches the high splits. Others argue that having a GP very invested in the LP’s performance encourages growth in good times and provides a safety net in bad times. As crude has fallen dramatically over the last 15 months, taking the Alerian MLP Index (AMZ) with it, we’ll examine which side investors have found more plausible (so far).

MLPs in the high splits were examined on a total return basis in comparison to the AMZX, the total return version of the AMZ. In order to be included in the study, an MLP must have reached the 50/50 splits by August 29, 2014 and must have still been trading on September 29, 2015. This led to 14 exclusions: five names in the high splits were acquired during the period, and nine names entered the high splits during the period. (No one seems to believe that MLPs are continuing to raise distributions in this environment, but it’s true!)

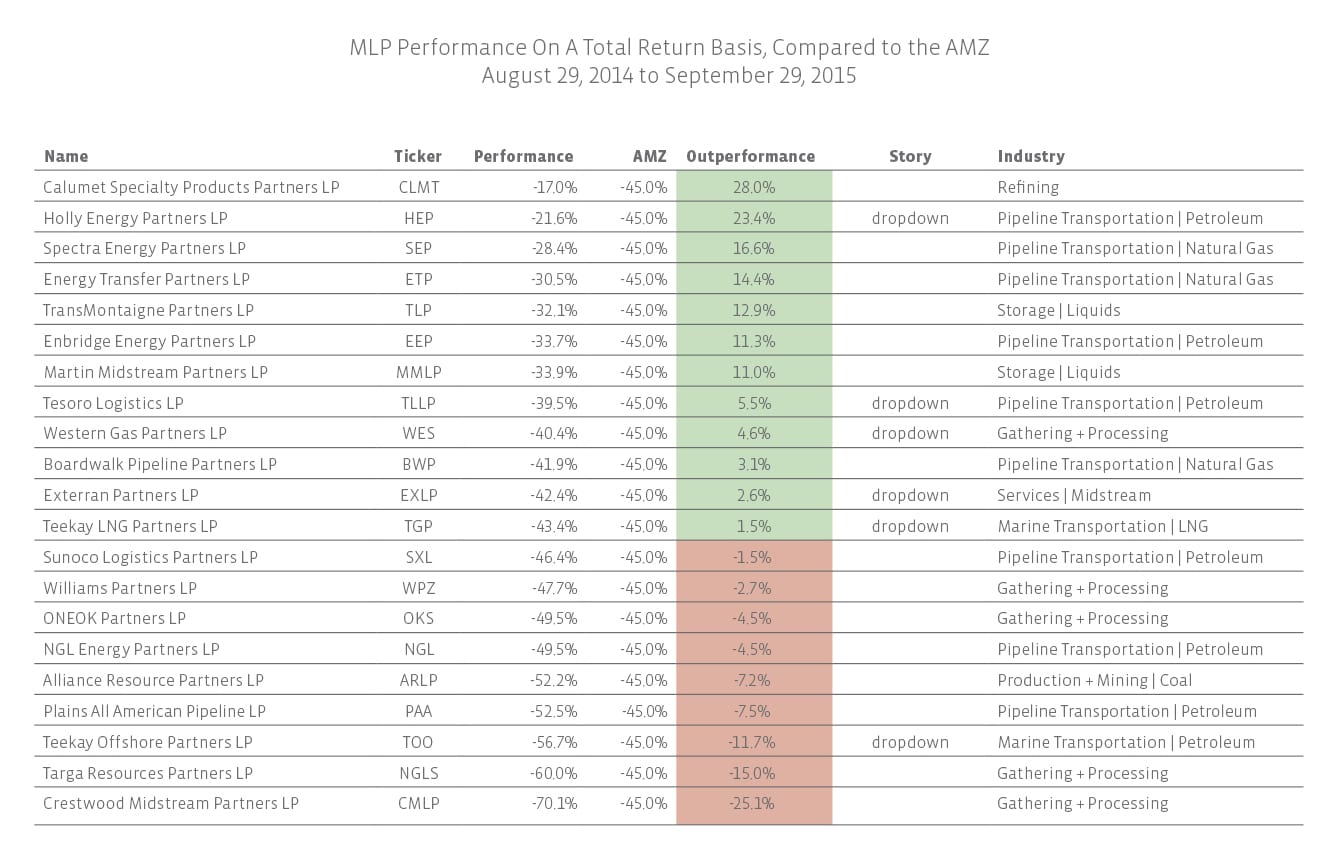

That left 21 MLPs to examine. I know I buried the lede, but these names outperformed the AMZX on average by 2.6%, though the spread of returns was very wide. Unsurprisingly, both extremes are companies with businesses sensitive to crude prices. The biggest outperformer was Calumet Specialty Products Partners (CLMT), a refining MLP that benefited from low feedstock prices. CLMT beat the AMZX by 28.0%. The worst underperformer was a gathering and processing (G&P) company, Crestwood Midstream Partners (former ticker: CMLP), which underperformed the AMZX by 25.1%. The poor performance was due to investor concern about exposure to dry gas plays like the Barnett and Fayetteville, where production is slowing, as well as Bakken crude-by-rail contracts that are up for renewal in 2017. CMLP is no longer trading due to a merger with its GP, Crestwood Equity Partners (CEQP).

Of the five G&P MLPs studied, all but one—Western Gas Partners (WES)—underperformed the AMZ. With the exceptions of the companies named above, subsector did not seem indicative of performance. Some pipeline transportation companies outperformed the AMZX while others underperformed.

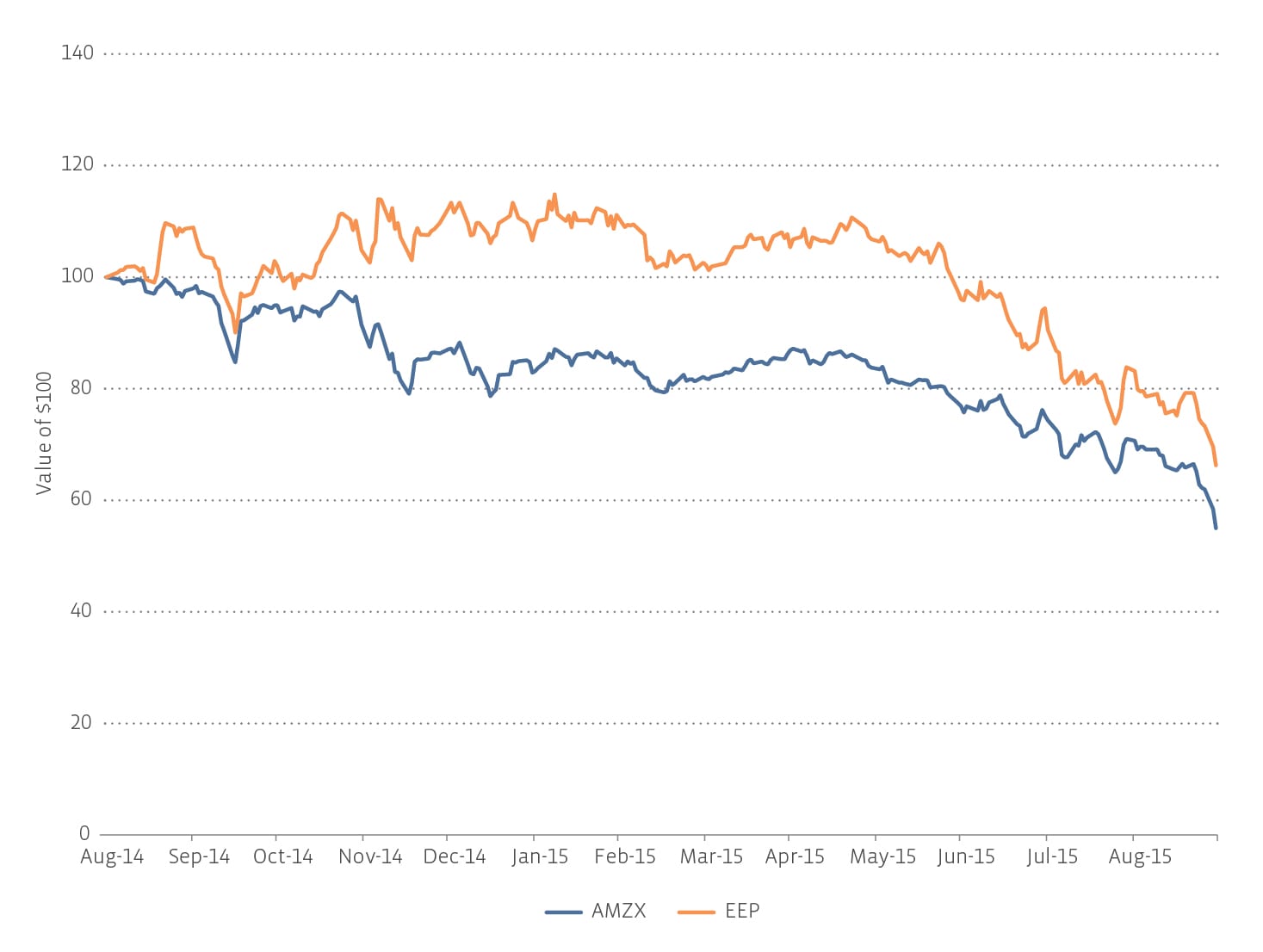

The most predictive factor was whether a partnership could expect dropdowns from the GP. Dropdown stories have visible growth that is independent of commodity prices. Looking at the chart of Enbridge Energy Partners (EEP) compared to the AMZX, the times EEP swung to outperforming the AMZX were when announcements were made that the sponsor, Enbridge Inc (ENB), would drop down assets. EEP outperformed the AMZX accordingly by 11.3% during the period. Of the six dropdown MLPs, five outperformed the AMZ and only one underperformed.

{kind=link}

{kind=link}