Summary

- While preference for growth or value investing can depend on factors like the economic cycle or time horizon, uncertainty in the current environment has amplified the growth vs. value debate.

- Although high growth investments may seem more enticing during hot equity markets, value investing has proven durable and has done particularly well in recent months.

- With growing interest in value stocks, it is important to understand how some of the major, broad value indexes are constructed.

-

Investors with a strong value thesis may want to consider a deep value index, rather than a core value index that offers only broad exposure to value stocks.

As equity markets bounced back from pandemic lows, many investors have grown accustomed to high returns, and overall equity investments have become seemingly overvalued. Pre-pandemic, growth stocks had experienced years of strength, much of which was triggered by the growing popularity of tech-related stocks and the rise of the retail investor. And now with earnings results largely “beat and raise” across multiple sectors, it’s tempting to keep jumping into high growth investments. But there is still a case for value investing, particularly in our current environment. Higher inflation expectations are beginning to weigh on growth stocks as we approach what many think is an extended “reopening trade.” Since late 2020, many believed that the COVID-19 vaccine would allow economies to reopen and global trade and travel to resume, which would trigger a rotation into value stocks. And while value has certainly picked up steam, the re-emergence of the Delta variant and overall economic uncertainty has created significant debate in the value vs. growth arena. But, whether investors prefer a value, growth, or blended style, it is essential to first understand how broad style indexes are constructed in comparison to pure style indexes and which one is more appropriate for the investor’s objective.

Growth vs. Value: A Brief Review

Investors often choose value investments because they believe these are misvalued and are available at a relatively cheaper price than their peers. Because we assume that markets are mostly efficient, investments are only mispriced temporarily—the goal is to buy an investment at a low price, then benefit from its price appreciation when the price returns to a more reasonable level. Relative “cheapness” is typically measured by valuation multiples, which could be price-to-earnings (P/E), price-to-book (P/B), price-to-sales (P/S), and enterprise value-to-EBITDA (EV/EBITDA), among others. Value stocks may perform better during the end of recessionary periods or during early parts of economic expansion. Many of these investments could also be older, more established companies in industries like utilities or financials, which may exhibit stable yet modest growth—but don’t necessarily trend on social media.

On the other hand, growth stocks are typically in fast-growing industries like technology, which may receive more media coverage and analyst attention. Examples include some of the internet tech giants or biotech companies which have exhibited high returns in a relatively short period. These investments are often projected to have higher earnings growth forecasts but will likely trade in line or at more expensive valuation multiples relative to their peers.

Value as an index strategy—broad or pure exposure?

It is important for investors to differentiate a broad value exposure from a pure value exposure. Many of the popular value and growth indexes are more beneficial for investors who wish to have a broad growth/value exposure of a core equity index. For example, consider the starting universe of the S-Network US Equity Large/Mid-Cap 1000 Index (SN1000), which is a core index of the 1,000 largest U.S. stocks. The S-Network US Large/Mid-Cap Value Index (SN1000V) reduces the number of constituents to 700 by netting growth and value scores and selecting the constituents with the highest net value score. This produces a broad value index—essentially the core index less those constituents with the highest growth characteristics—which may not be as pure as the investor desires. Likewise, the S-Network US Large/Mid-Cap Growth Index (SN1000G) also contains 700 stocks from the core universe of 1,000 which have the highest net growth score. This leads to over half of the constituents (396 out of 700) overlapping within the value and growth indexes. A similar sort of methodology is also used in other large indexes such as the S&P 500 Value Index (SVX), S&P 500 Growth Index (SGX), Russell 1000 Value Index, and Russell 1000 Growth Index, resulting in broad style indexes with many overlapping constituents.

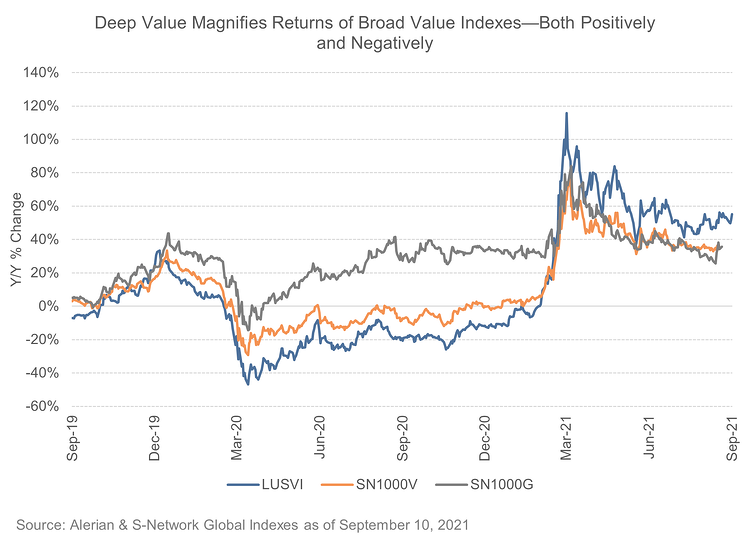

But if the investor’s objective is to find a pure exposure to value, they may prefer to use a deep value index rather than a broad value index. Deep value indexes include a selection of the most value-oriented stocks—these typically will not have any crossover constituents with aggressive growth indexes. Investors who may want a pure value approach can look at an index like the Lyrical U.S. Value Index (LUSVI). This index selects the cheapest quintile (200 out of 1,000) stocks based on one-year-forward P/E ratios. This produces an index with magnified returns—both positively and negatively—relative to a broad value index. In the chart below, LUSVI underperformed SN1000V when value was out of favor during early 2020; however, LUSVI has achieved higher returns than SN1000V now that value has been improving.

Bottom Line:

While growth stocks have dominated headlines in the recent past, value stocks have started to become more favorable through the global reopening trade. As more investors consider value investing, it is important to understand how broad value indexes are constructed in comparison to pure deep value indexes and which one better suits the investor’s objective.

LUSVI is the underlying index for the Lyrical Asset Management U.S. Value ETF (USVT).