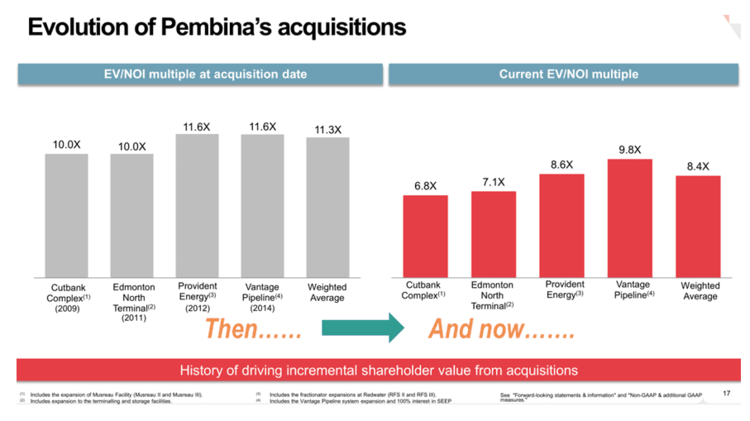

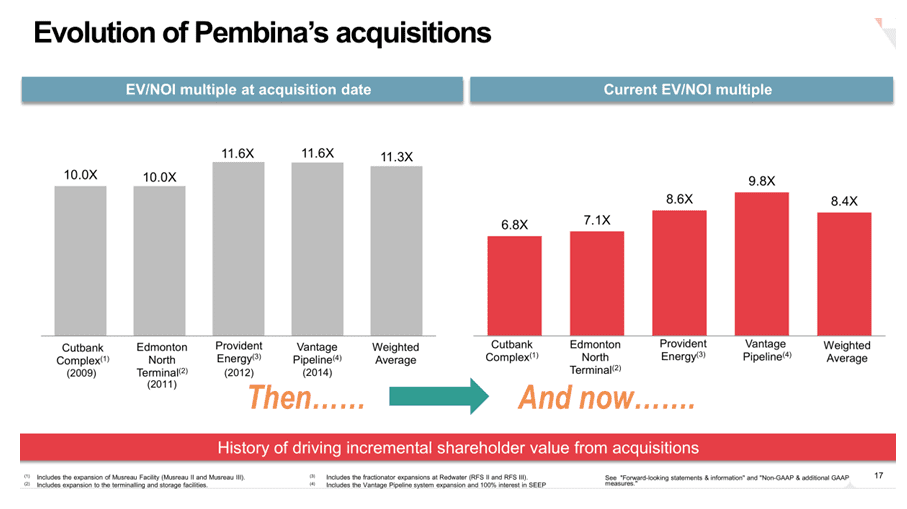

Where Pembina’s message was unique was management’s presentation of how the company’s acquisition multiples have changed after the fact. As we’ve mentioned before, the main reason large North American energy infrastructure players believe M&A has not happened despite the challenging market environment is that the bid-ask spread for desirable assets remains wide. The deals that are getting done aren’t home runs from a multiple perspective. Many are neutral in the near term, and some are even mildly dilutive. Over the long term, efficiencies and synergies do bring down multiples. This is the thinking behind deals like Energy Transfer Equity (ETE) offering to buy Williams Companies (WMB)—the focus is on 2019 and beyond. Lots of words are written about where multiples will move to, but it’s nice to be able to see the before and after, rather than just the projections.

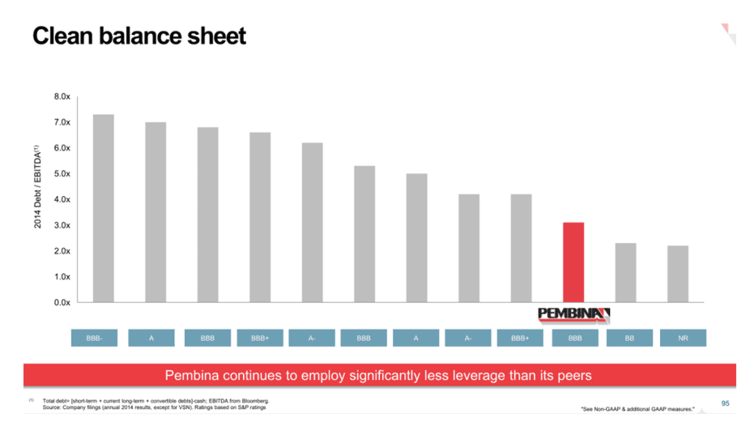

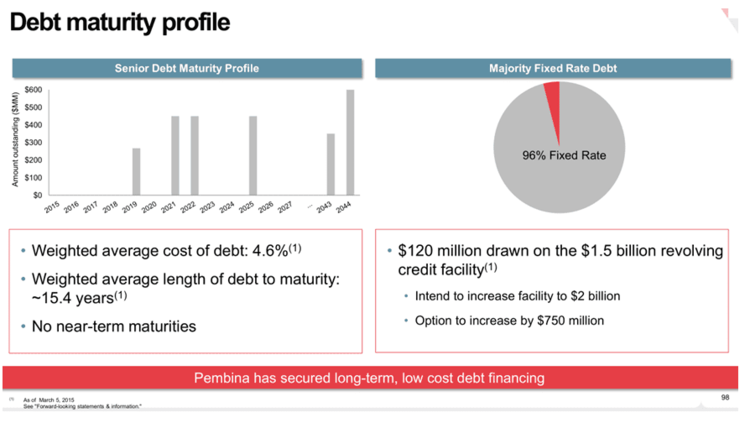

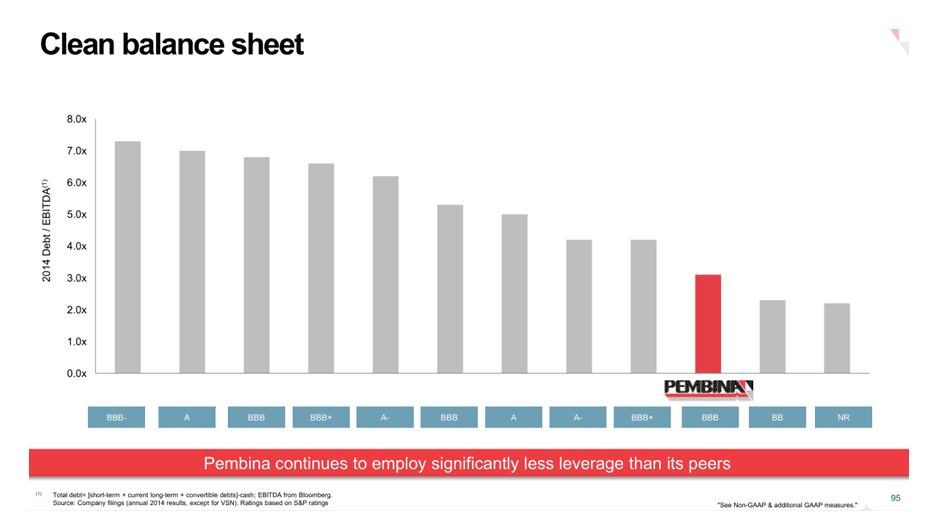

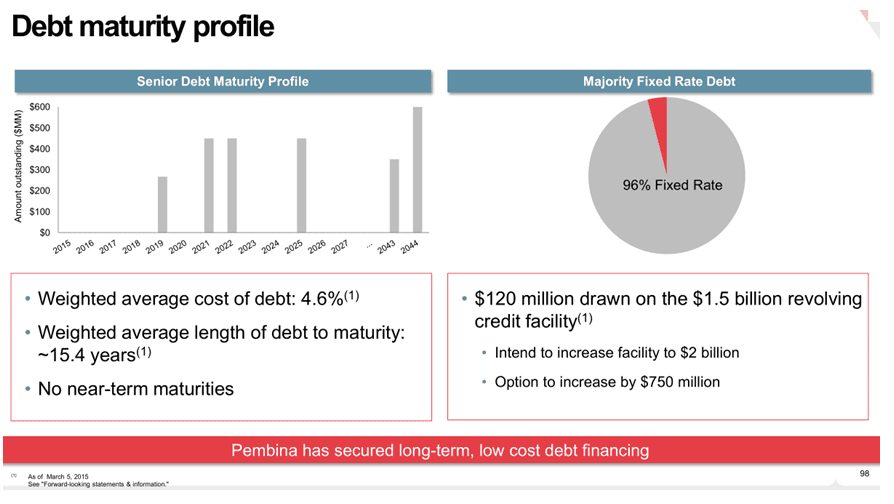

The first questions to ask around interest rate sensitivity are fairly similar to the first questions about cash flow. How much debtdo you have, and how much of that is fixed rate versus floating? (Just like, how much cash are you earning, and how much of that is fee-based versus commodity price sensitive?) Raw debt is rarely useful, so measures like leverage ratios (Debt/EBITDA) are frequently used. In this way, comparisons can be made not only over time, but also between companies.

Looking at a snapshot in time of leverage ratios is helpful, but does not consider the whole story in the same way that a $500 payday loan is not the same as a $250,000 30-year fixed-rate mortgage, is not the same as $40 borrowed from your buddy, is not the same as a $100,000 10-year floating-rate mortgage. Both time frame for repayment and the cost of the debt matter. Given that nearly everyone expects interest rates to increase, locking in low rates now for long-term debt can be a very smart move.

{kind=link}

{kind=link}

{kind=link}

{kind=link}