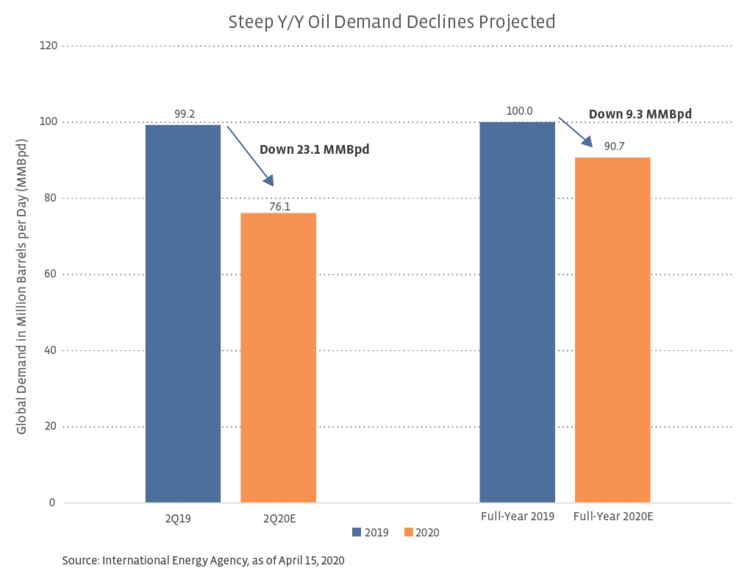

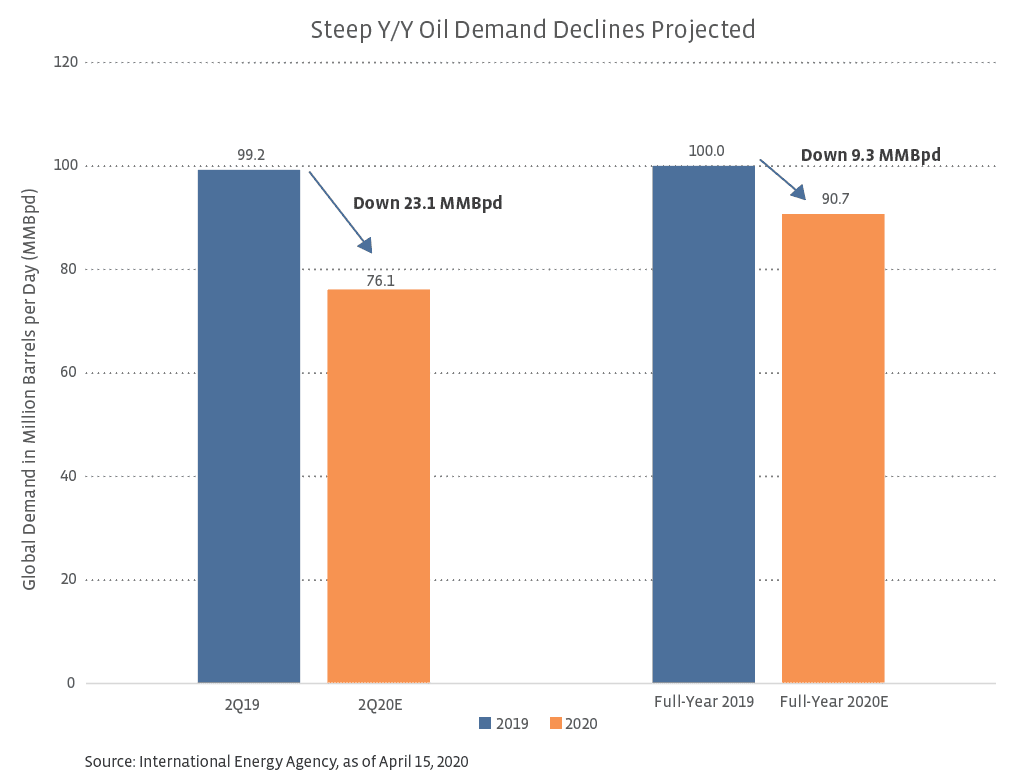

While the IEA provides a global forecast, it can also be informative to examine what energy companies are seeing on the ground. With energy earnings season underway, companies have provided more real-time demand insights stemming from their businesses and the geographies where they operate. In the midstream space, Kinder Morgan (KMI) discussed a 40-45% reduction in refined product volumes on their April 22 earnings call. KMI’s refined product pipelines serve California, Arizona, the Southeast, and Mid-Atlantic. In their revised 2020 EBITDA guidance, KMI assumed a 40-45% reduction in 2Q20 refined product volumes versus their prior assumptions, with the reductions moderating to 10-12% in 3Q20 and 5-6% in 4Q20. On a year-over-year basis for the month of April, Magellan Midstream Partners (MMP) saw their gasoline loadings fall 33%, distillate (diesel) loadings fall 9%, and jet fuel loadings (a smaller portion of their business) fall 72%. However, the last seven days of the month had seen some improvements – a 24% decline in gasoline, a 4% decline in distillate, and a 76% decline in jet fuel compared to last year. In MMP’s sensitivity analysis for 2020 distributable cash flow, the low end assumes 2Q20 demand declines of 25% for gasoline, 5% for distillate, and 70% for jet fuel.

Refiners process oil into the products that are ultimately consumed by end users (gasoline, diesel, jet fuel, etc.), which gives them a front seat to demand. When asked about gasoline demand on their earnings call Wednesday, bellwether refiner Valero (VLO) indicated that they were seeing improved demand, particularly in the Mid-Continent and Gulf Coast. For the last two weeks of March and first few weeks of April, they described demand as 55% of normal. However, the seven-day average at the time of their call on April 29 saw demand at 64% of normal – a noticeable rebound. Phillips 66 (PSX), which markets fuel in Western Europe and the US, noted that demand in Western Europe was down 70% at its worst and was currently down 50%. In the US, PSX initially saw demand down around 50% but had seen it improve recently to only being down 35%. For added international perspective, Chevron (CVX) cited demand declines of 75% for jet fuel, 50% for gasoline, and 25% for diesel, while noting that petrochemical demand has held flat. Chevron’s refining capacity is concentrated in North America and Asia-Pacific.

While demand globally and in the US seems set to improve into May building on momentum from the end of April, the outlook for the rest of the year is clouded by uncertainty around how life will continue to adapt in a world with COVID-19. Setting aside the resilience in petrochemicals, demand for distillate/diesel has held up relatively well compared to other fuels. Jet fuel has seen the largest demand decline, but jet and kerosene accounted for just under 10% of the total oil demand for developed countries in 2019. While the pace of a demand recovery will likely vary by geography and refined product, most stakeholders seem to expect a gradual recovery through the rest of this year, which will complement production cuts to help restore balance to the oil market.

{kind=link}