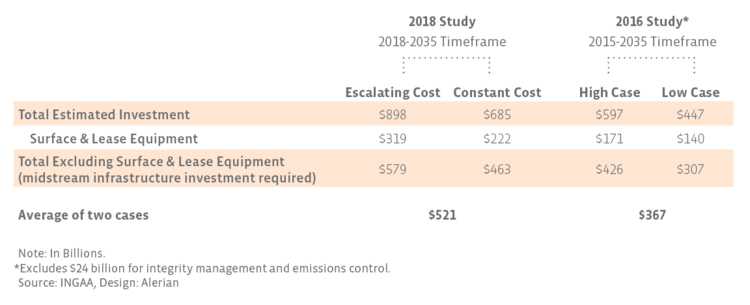

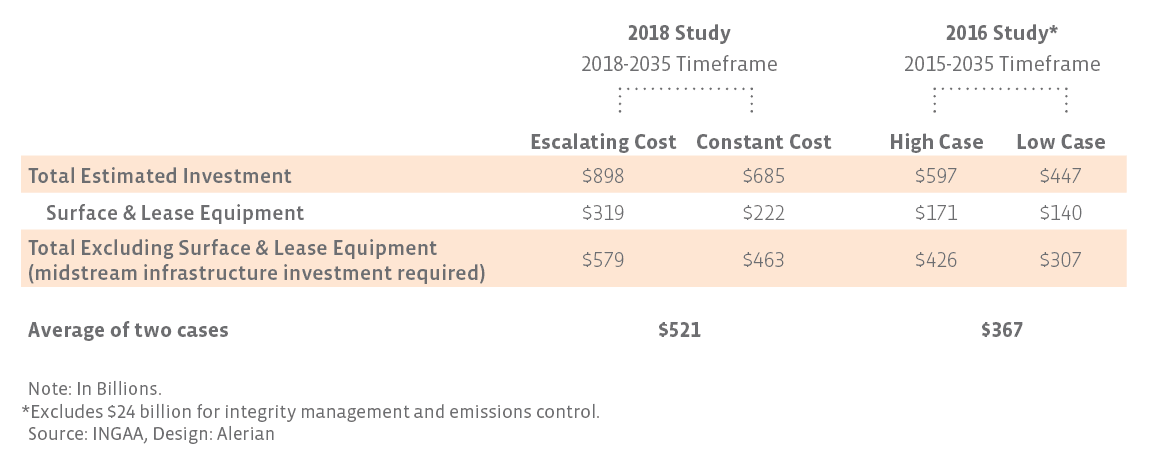

How does the 2018 study compare to the 2016 study? For context, the prior study was released in April 2016, shortly after WTI oil prices had hit a relative bottom at ~$26/Bbl in February. In other words, energy land was looking fairly glum at that time. With the improvement in WTI oil prices to the mid-$60’s/Bbl recently, the estimated investment in oil and gas infrastructure has not surprisingly increased with the 2018 report. The average case for 2018-2035 of $521 billion is greater than even the high case from the 2016 study. Keep in mind the 2016 report covers three additional years. To even the playing field, the updated run rate of $29 billion per year in spending is well above the 2016 high case run rate of $20 billion per year.

Where are all those billions going?

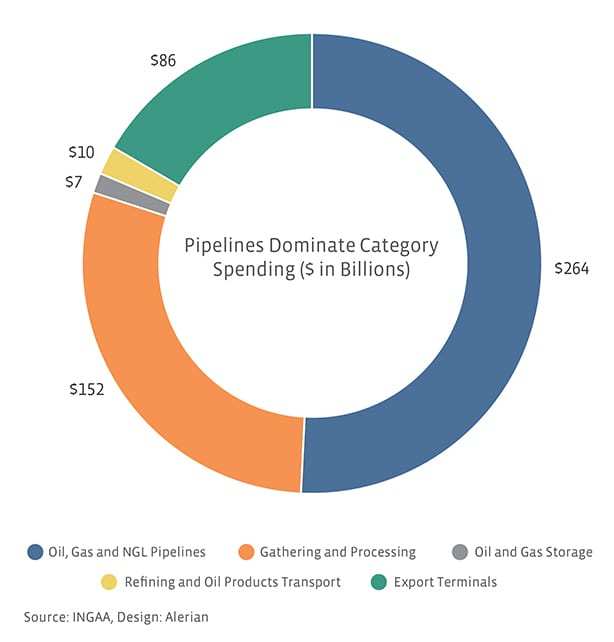

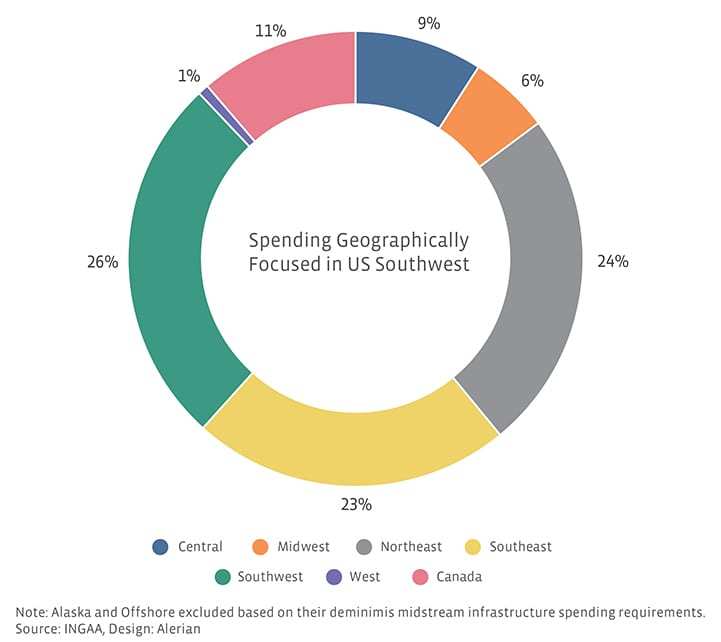

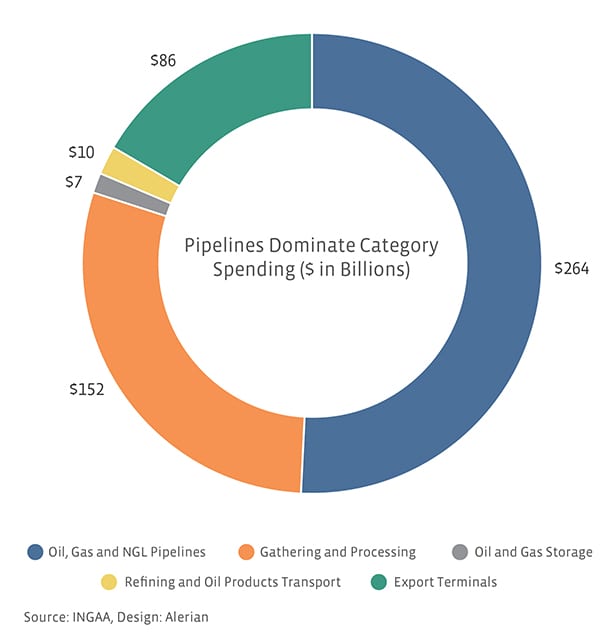

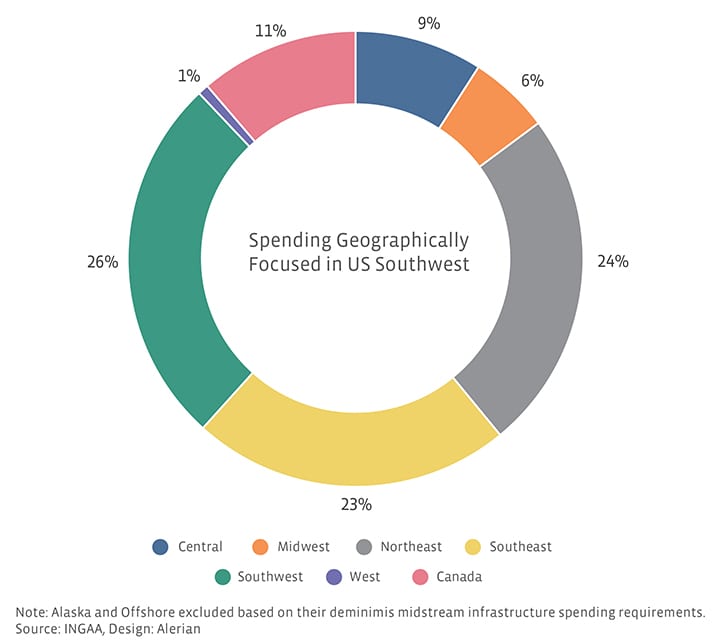

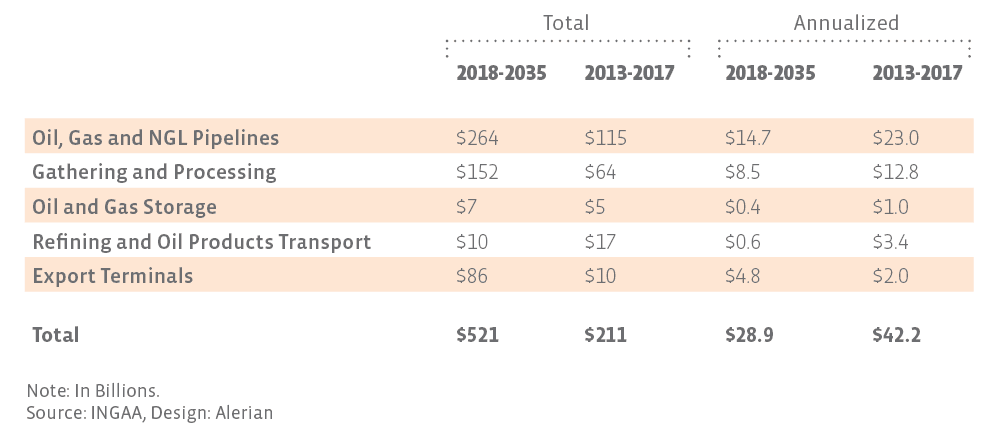

Of the $521 billion expected to be invested in US and Canadian midstream infrastructure through 2035, approximately half is allocated to oil, gas and NGL pipelines at a rate of ~$14.7 billion per year. Almost a third will be related to gathering and processing investments, equating to over $8 billion per year. Export terminals are expected to account for the third largest spending category, representing 17% of the total. Geographically, of the $521 billion, approximately a quarter of the total spending is expected to be concentrated in the Southwest US (TX, OK, LA, AR, NM). Canada represents 11% or $59 billion of the total estimated midstream spend.

What is the spending trend relative to recent years?

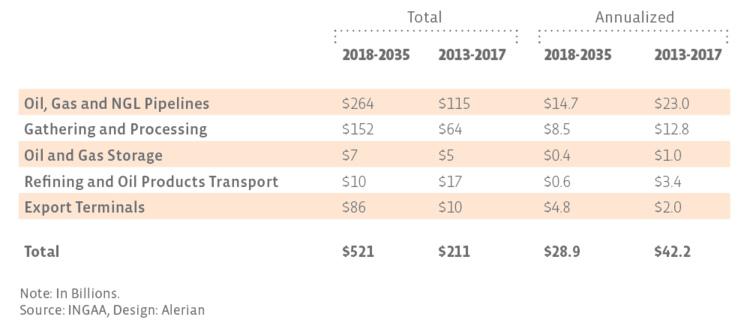

Infrastructure spending has been robust in recent years, as US oil production increased by 2.9 million barrels per day (44.0%) and natural gas production increased by 10 billion cubic feet per day (12.3%) from 2012 to 2017. For the five-year period of 2013-2017, spending (excluding surface and lease equipment) averaged $42 billion per year. Though more moderate, the $29 billion annualized spend for 2018-2035 is still robust. As shown in the table below, export terminals are the only category expected to see a pick-up in annualized spending relative to the prior five years. We’ve discussed in past posts how rising exports will create growth opportunities for MLPs and energy infrastructure companies.

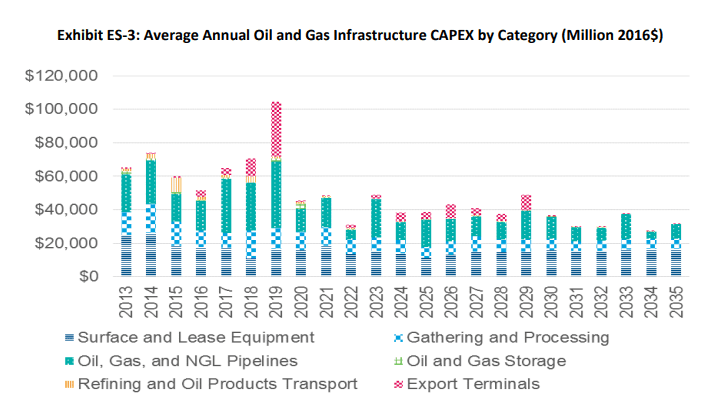

Spending forecasted to peak in 2019, but we’ve seen false peaks before.

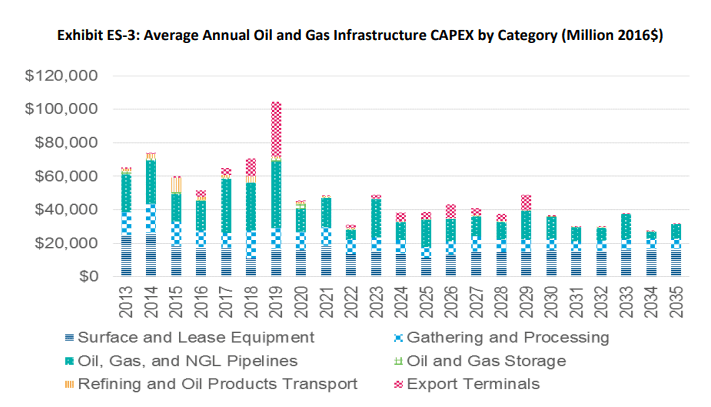

The 2018 study forecasts that infrastructure investment in the US and Canada will peak next year at over $100 billion (including surface and lease equipment) – topping the $74 billion spend from 2014 as shown in the graphic below. Relative to other years, outsized spending on export terminals and pipelines drives the heightened spending in 2019. Examples of additional LNG capacity expected to be completed in 2019 include trains 1 and 2 from Cheniere’s (LNG) Corpus Christi terminal and train 5 from its Sabine Pass terminal, train 1 from Sempra’s (SRE) joint venture Cameron LNG terminal, and units at Kinder Morgan’s (KMI) Elba Island terminal. There should be good visibility for 2019 spending at this point in 2018, meaning the $100+ billion estimate should include less guesswork than outyear forecasts. Only time will tell if 2019 will really represent the peak for infrastructure spending. For reference, the 2016 study expected spending to peak in 2016 under the high case and to have already peaked in 2014 under the low case.

Source: INGAA

Bottom Line

With most oil and gas forecasts, any projection beyond five years should probably be taken with some degree of caution. Predicting the future is difficult as things constantly change — just look at the differences in projections from the 2016 study to the 2018 study. That said, the updated INGAA study is still informative for midstream investors, providing useful information on what categories will see investment and what geographic regions will see investment. The expectation for robust infrastructure investment in 2018-19, relative to the already high spend in the last five years, is particularly noteworthy, as is the expected investment in exports. While the study provides comfort around long-term growth prospects, the expected investments in the near-term may be more exciting to today’s investors.

Alerian is on Twitter! Join the conversation with @AlerianIndices.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}