Summary //

- US oil production is declining as exploration and production (E&P) companies shut-in wells and pull back capital spending.

- Company-level production curtailments from US E&Ps as a percentage of volumes range from 4% to 70%.

- Commentary from producers so far indicates that the impact of curtailments for midstream may be relatively muted.

In response to the dramatic decline in oil demand stemming from the COVID-19 pandemic and the resulting price weakness, global oil supply is expected to fall significantly this month, as OPEC+ cuts took effect May 1. Some producers began implementing production cuts early, and Saudi Arabia has announced an additional cut of 1 million barrels per day (MMBpd) for June. The International Energy Agency (IEA) is forecasting global oil supply to fall by 12 MMBpd to a nine-year low of 88 MMBpd in May. While the agreement between OPEC and its allies to cut production by 9.7 MMBpd makes up the bulk of the decline, the US and Canada are leading the cuts among countries not party to the OPEC+ agreement. Supply from countries outside the OPEC+ agreement had already fallen 3 MMBpd since the beginning of the year through April, and the IEA estimates that production could fall by another 1 MMBpd in June. Specific to the US, the Energy Information Administration (EIA) estimates that oil production in June will be 1.5 MMBpd (-11.8%) lower than in December 2019. For full-year 2020 and 2021, the EIA is forecasting oil production of 11.7 MMBpd and 10.9 MMBpd, respectively, as US exploration and production (E&P) companies shut-in wells and pull back capital spending. For context, these updated forecasts represent year-over-year declines of 0.6 MMBpd (-4.4%) this year and 0.8 MMBpd (-6.8%) in 2021. Production declines clearly limit near-term growth opportunities for midstream, which has reduced growth capital spending plans in response to the current environment (read more). But what do production declines mean for existing assets? Today, we examine commentary from E&Ps and energy infrastructure companies on production curtailments and discuss how midstream could be impacted by the decline in US oil production.

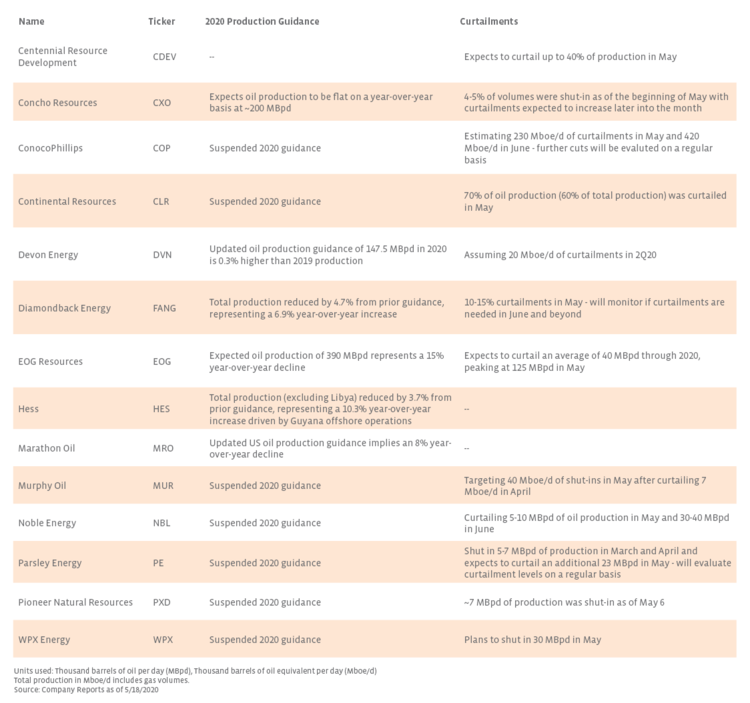

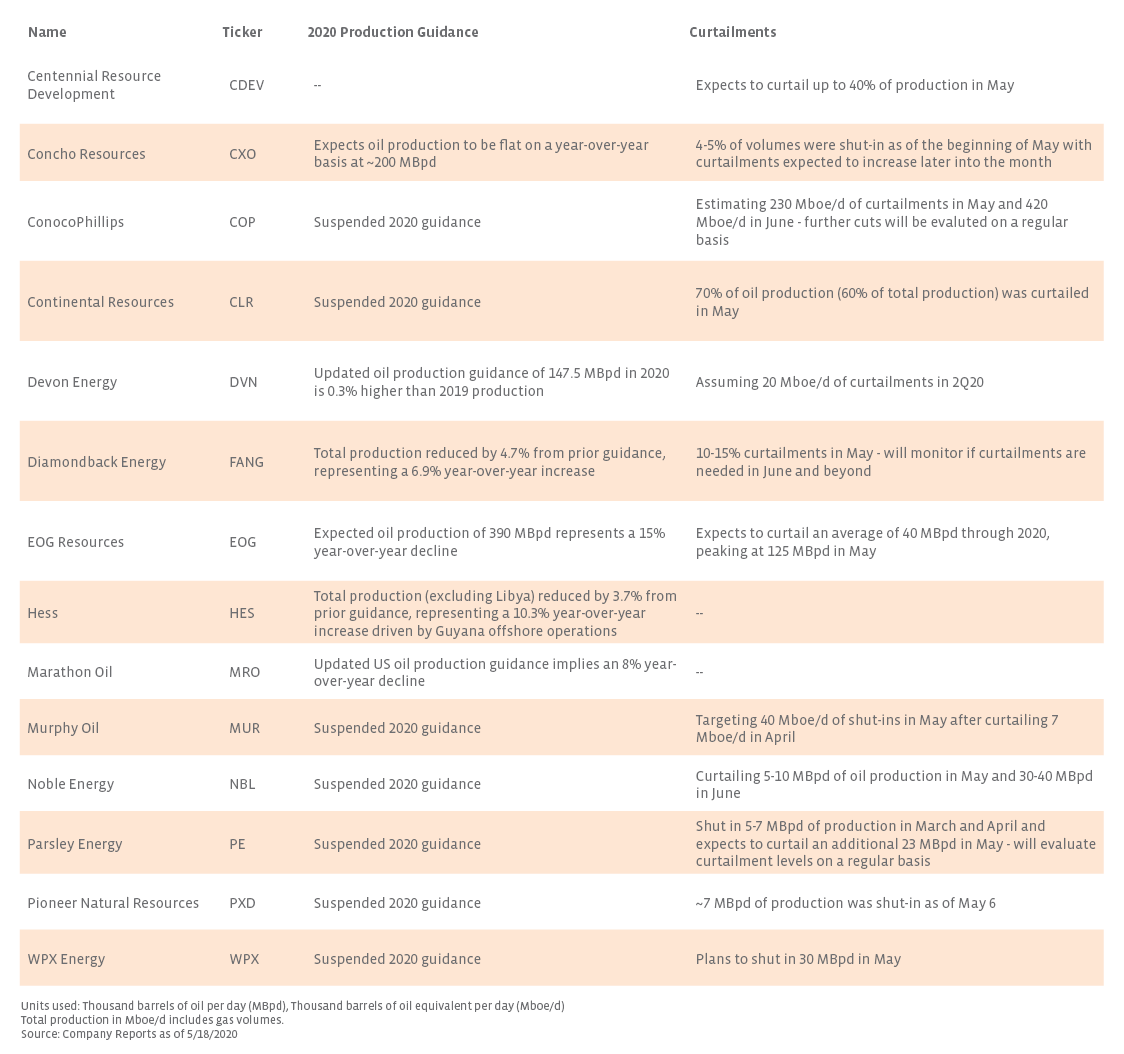

Unsurprisingly, production guidance from E&Ps for 2020 has largely been revised to the downside or suspended due to uncertainties surrounding the macro energy environment. The table below provides production commentary from select E&Ps. As a percentage of volumes, shut-ins have ranged from 4-5% for Concho Resources (CXO) to up to 70% for Continental Resources (CLR). The wide variation in curtailments among producers is dependent on a variety of factors, including geography, production costs, and crude quality. Hess (HES) and Marathon Oil (MRO) are the only names below that have not yet announced shut-ins, but both lowered full-year oil production guidance. For its part, HES secured 6 million barrels (MMBbls) of storage by chartering very large crude carriers, with plans to store barrels in May, June, and July to be sold in 4Q20. Midstream companies have also offered their perspective on oil production going forward. Plains All American (PAA) is projecting that Permian Basin production will decline 15-20% this year on an exit-to-exit basis, the midpoint of which would imply 3.8 MMBpd of production for December 2020 compared to 4.8 MMBpd in February 2020. PAA estimates that Permian production will reach its trough in June and will stay flat in the second half of the year. Targa Resources (TRGP) forecasted that 10% of total oil and gas production in the Permian and Mid-Continent and 20% of oil volumes in the Bakken would be shut-in beginning in May. On its 1Q20 earnings call, Energy Transfer (ET) noted that 8% of volumes on its Midland Basin gathering and processing system had been shut in at the beginning of May. However, as of May 11, roughly 25% of the previously shut-in production had come back online, pointing to a potentially quicker recovery than other midstream and E&P commentary implies.

Although take-or-pay contract provisions help insulate midstream cash flows from shut-ins (read more), declining production still presents a risk to energy infrastructure companies as volume-driven businesses. However, commentary from producers so far indicates that production curtailments may not have a significant negative impact on midstream companies. In an April market update call, COP management noted that it will continue to manage its pipeline commitments despite curtailments. Additionally, management expects robust production from shut-in wells in the Lower 48 once they are brought back online. Parsley Energy (PE), which shut-in 5-7 thousand barrels per day (MBpd) in March and April and guided to another 23 MBpd of curtailments in May, does not expect to incur any deficiency payments related to its transportation commitments, implying that the producer will meet any commitments to its midstream service providers. Additionally, the lack of government-mandated curtailments is an incremental positive for midstream. Earlier in the month, the Railroad Commission of Texas voted against enacting statewide production cuts, and the Oklahoma Corporation Commission took no action after hearing arguments for mandated curtailments. Enterprise Products Partners (EPD) CEO Jim Teague was a notable opponent of these measures, citing the negative impact that they would have on midstream. In addition to potentially shutting-in production in an inefficient manner, mandated cuts may have allowed struggling producers to avoid minimum volume commitments and the related deficiency payments to their midstream counterparties.

While the lower commodity price environment and resulting decline in oil production poses a potential threat to energy infrastructure companies, the impact that shut-in volumes will have on midstream cash flows may be relatively muted. As discussed previously, midstream EBITDA forecast revisions have been modest when compared to other sectors of energy, reflecting the stability of their fee-based businesses and take-or-pay contracts (read more). Certainly, midstream providers were in discussion with their customers when forming their outlooks. Curtailments are also temporary measures, and some E&Ps could be incentivized to bring production back online sooner than anticipated given the recent rally in WTI oil prices to nearly $32 per barrel as of May 18. With production declining, larger, integrated midstream companies will benefit from diversified customer bases and commodity exposure. Overall, midstream continues to remain well positioned to weather the current energy downturn, even in the face of curtailed volumes.

{kind=link}